Good inights, Rahul.

Thanks for taking the time to prepare this. I think HFCs deserve a separate thread of their own.

Let me chip in my couple of thoughts.

- The “A Players”, i.e. the ones which have good asset quality (GNPA ~1.5%), high ROE (~14-15%+) and low leverage (<4 times Debt/Equity) are mostly owned by PE firms, who entered in early stages and have navigated the companies to their IPOs.

For example, Aptus and India Shelter is heavily held by Westbridge, Aavas by Kedaara, Home first by Warburg Pincus (Orange Clove) etc.

These PE players are basically funds which have end of life. Until these PE funds are on the cap table, expect these companies to face constant bouts of stock supply and therefore, prices may remain compressed despite 25-30% AUM growth and pristine asset quality. At least that is how these A-player stocks are playing out for now.

- “B players” like PNB housing, LIC housing, Can Fin, etc. (I would also call Can fin a B player, because of its leverage and modest 15% growth, although it has strong parentage of Canara bank and very good asset quality) are fighting against inertia and their growth rates have never really appealed, Moreover, their leverage positions may give them lesser headroom for aggressive growth compared to A-players. All this shows up in their mid-teens AUM growth and moderate asset quality.

PNB housing might foray into microfinance under new leadership, Can fin homes might foray into digital transformation and risk management after Ambala incident, but give or take, these are 10-15% growers. Dont expect the moon from them.

- Now come the underdogs, Hudco, Repco, etc. These are actually the “C Players” behaving like “A players” temporarily. when credit cycle turns, they have proven to disappoint a lot. Hudco for example, is known to trade at <1 PB and is now trading at 3.12 PB.

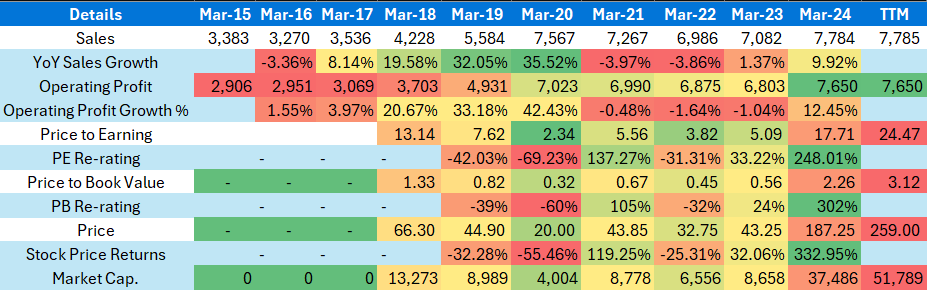

Here’s a look at Hudco at a high level:

In FY24, Hudco’s topline has grown by 9%, operating profits have grown by 12%, however its PB is re-rated from 0.56 PB to 3.12 PB, a whopping 6x PB update. Naturally the price has gained 6x not much because of fundamental growth but because of re-rerating.

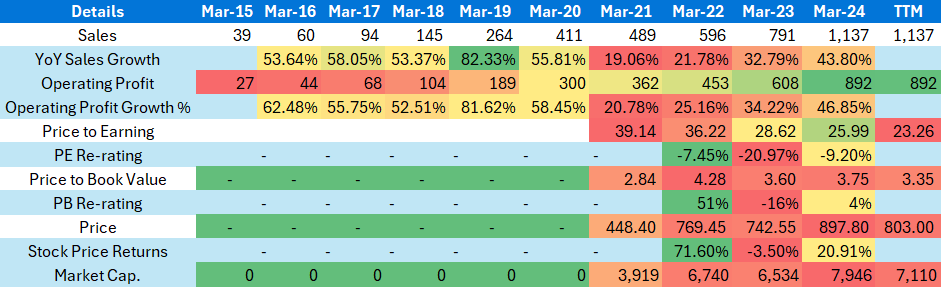

Take a look at an A Player, in comparison:

Home First:

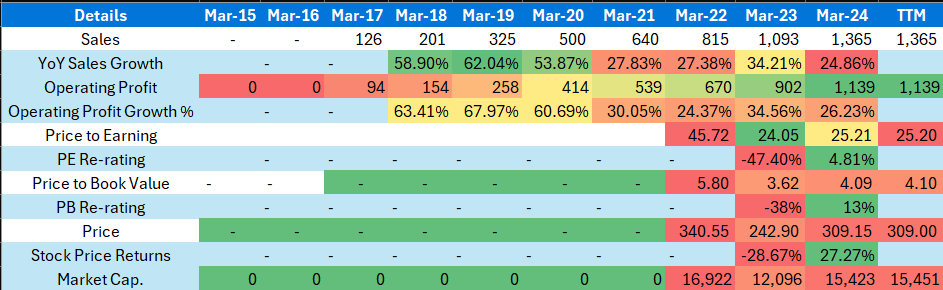

Aptus:

AUM and Book Value Growth wise, Hudco stands nowhere close to the A players:

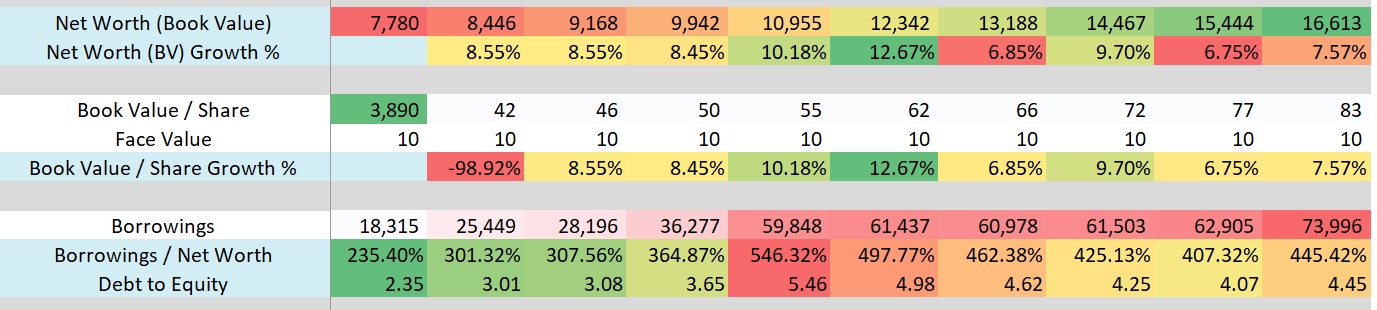

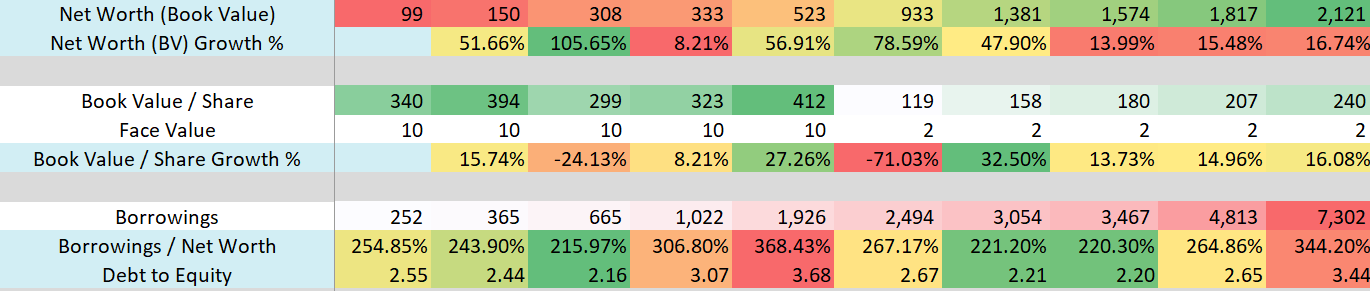

Hudco’s Balance Sheet metrics:

Hudco’s AUM growth (Derived):

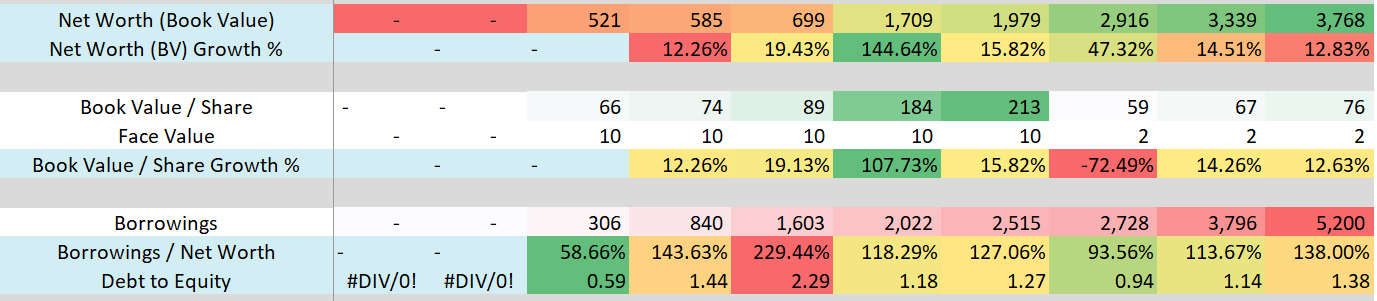

Home First’s Balance Sheet metrics:

Home First’s AUM growth (YoY):

Aptus’s Balance Sheet metrics:

Aptus’s AUM growth (YoY):

Clearly, the A players have better balance sheet, less leverage, higher AUM growth, less delinquencies and credit cost.

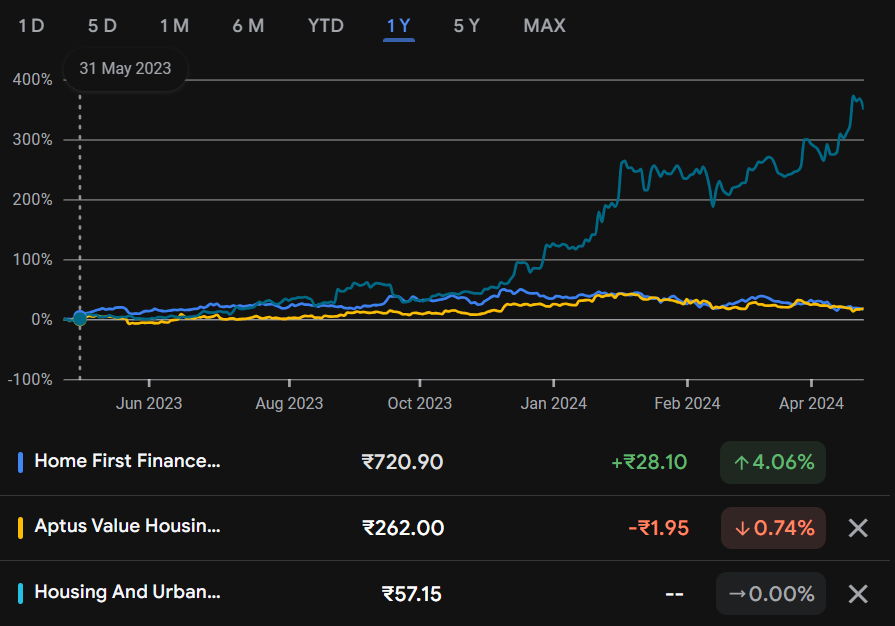

Now look at the price chart of Home first, Aptus and Hudco for last 1 year.

| Subscribe To Our Free Newsletter |