Few info based on CEO’s 2024 YT video during Expo in Delhi:

- Exports share ~75%

- OEM and After market are focus segments – doesn’t seem to be doing contract manufacturing for likes of Timken, SKF etc.

- CV esp. heavy vehicles come up as prominent segments

Additional info from Timken concall – exports had one of the worst quarters with 15% share vs ~30% share during good times. Heavy vehicle segments really struggling with exceptions being rail road and South America market. Even India market had railways and industrial segment driving growth.

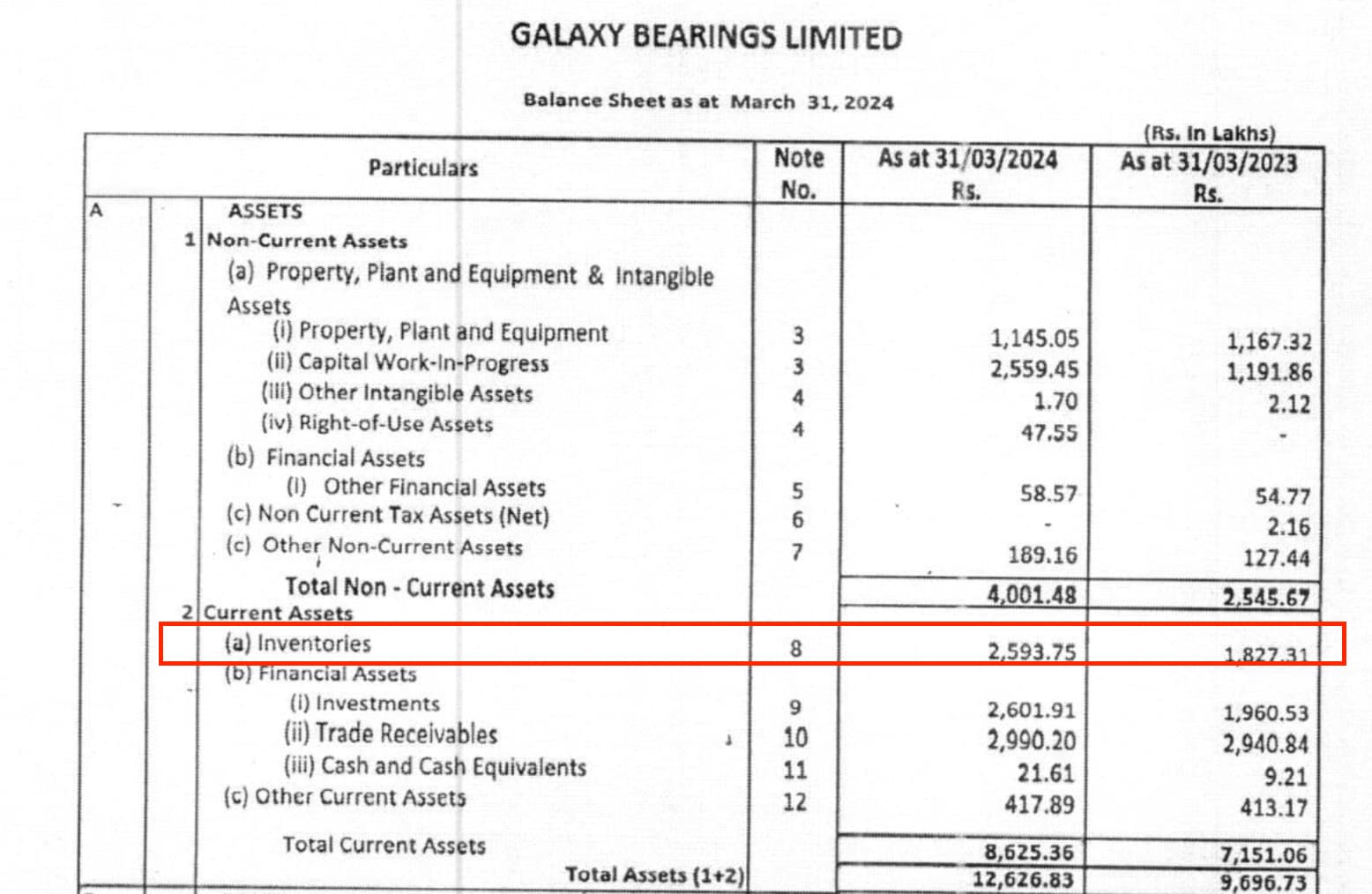

While MNCs like SKF, Timken along with Rolex had very health Q4 with topline and margin expansion leading to serious re-rating – Galaxy’s flattish Q1 results (YoY basis) DO NOT seem that bad in light of exports and heavy vehicle headwinds. Sharp QoQ uptick, high inventory levels (might be attributable to Red Sea in case they have exposure to related geographies) and upcoming capex (phase 1 potential commissioning in Jun / Jul) suggests that upcoming quarters may be worth watching out for.

Disc: Have exposure with recent purchases within last 30 days

| Subscribe To Our Free Newsletter |