Judging from the discussion so far, the following points seem to be the consensus view:

-

Investors find the subscription business unexciting.

-

The valuation vertical seems promising, but no one seems to have more insights to share.

-

The cash on the balance sheet is a common concern.

I have done a significant amount of work on the industry in the last year with @nirvana_laha. I have met with management a few times since listing, spoken to several of Prop Equity’s clients as well as competitors in the valuation vertical. In the interest of raising the quality of the discussion on the company, here’s my view on how one should look at the company.

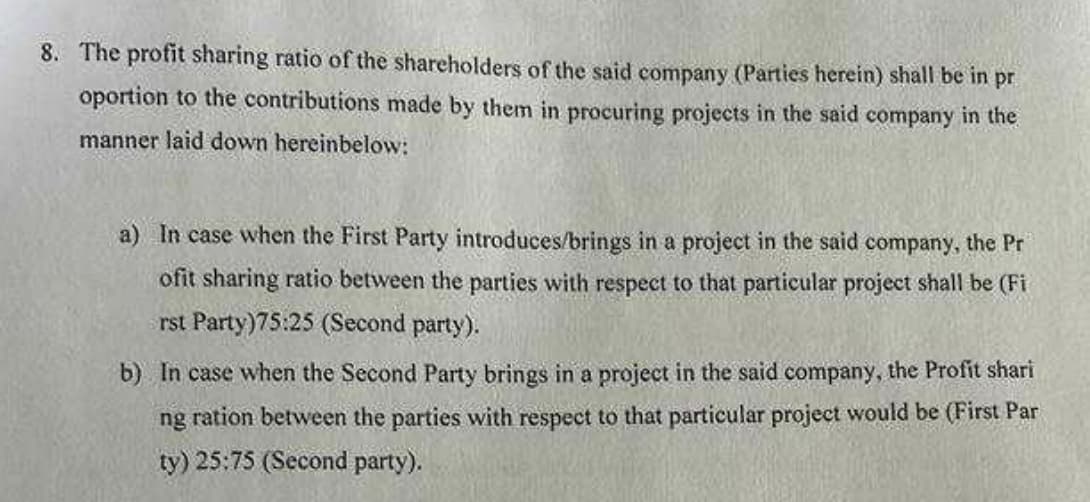

1. The valuation vertical has the highest probability of scaling successfully

I spoke to senior management at one of the largest PSUs, as well as a private bank, both are Prop Equity’s clients. Here are the key points:

-

Banks get valuation reports made for loans against property as well as new developments. For almost all private banks and PSUs, this is outsourced to companies like Prop Equity.

-

Depending on the ticket size, they need either two or three reports per property, and use the consensus to determine the loan eligibility / amount.

-

A vast majority of these reports are done by small brokers that operate out of a few districts in a city. (Example: Patwardhan Consultants that cover Mumbai / Pune / Nashik) There are only two or three companies that offer valuation services pan-India. Prop Edge and Adroit are in this list.

-

Banks have their own issues working with smaller regional brokers:

-

Lack of a uniform reporting format – A valuer in Bangalore may provide a different kind of property report from a valuer in Kolkata. This quickly becomes a headache with scale.

-

Small brokers don’t have bandwidth – The last week of a month is extremely busy, as banks try to clear pending loan cases. During this period, smaller valuers who run a 5-6 person office get overloaded, and they can’t cater to everyone at the same time. During this period, the turn around time for a report gets stretched to several days, while every bank wants them asap.

-

-

Larger organisations like Prop Equity or Adroit don’t run offices as lean (40-50 employees in major cities), and therefore have more people. This allows them to meet TAT targets during these busy periods. They also have standardised reports from across the country.

In cities where Prop Equity and Adroit have scaled successfully, they have taken 30% wallet share each from a large bank, displacing smaller unorganised brokers.

The thesis here is a shift from the unorganised to organised given a lack of serious pan-India players. There is room for 3-4 pan India companies to empanel with a bank, as banks have limits on how much wallet share a single valuer can take.

I leave it up to the reader to determine the market size for this vertical in India, but I have high confidence in Prop Equity scaling this vertical to 100 Cr. topline, with 40% EBITDA margins in the next few years.

2. The subscription business does not deserve bandwidth

It’s very difficult to raise prices for the subscription vertical as it stands right now. They have onboarded almost every large developer and bank. The TAM for this subscription business is at its infancy in India, and it’s far more profitable to build and sell value add services on the data they have collected.

This business will continue to bring in 40-50% margins as the costs are fixed, and this is why management calls this a cash cow. Any incremental effort spent on this vertical wont be as rewarding as the other new verticals that management has incubated, so it’s completely reasonable for management to focus efforts elsewhere.

The proof of this is in the valuation vertical: in 3 years, they have built this business from scratch and scaled to the size of the subscription business already, with over 400 employees and a topline of 20 Cr.

3. The cash on the balance sheet will be used on new verticals

Management’s model here is to incubate a new vertical, provide equity to the partner running the vertical, see how it fares with clients, and only after seeing success, spend on scaling the business.

There are three new verticals being scaled at the moment: developer management, project monitoring, and the vehicle valuation. Management mentioned that if project monitoring sees good traction in the next year or two, they’ll increase the spending on sales & marketing to increase visibility and win clients.

4. There are several dormant optionalities

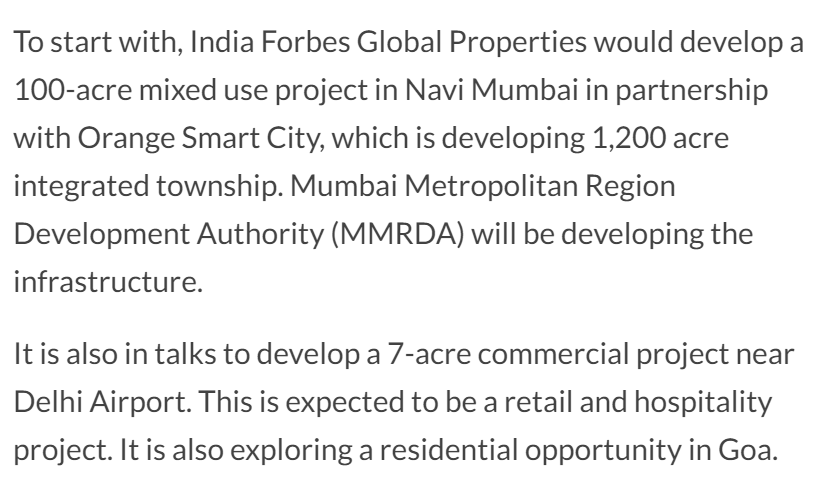

- Developer management is a vertical with Forbes Global that could have a large leap for Prop Equity given the profit sharing agreement. The JV will earn 10% of the sales value of any property developed and sold by the JV, and distributed to the partner that brought in the deal. They also have an agreement to develop one such property within five years.

-

Project Monitoring is the B2C vertical that management has been working on for the last 3 years. His claim is that this market is larger than the valuation vertical, and there is no competition in this space in India right now.

-

YouTube can be a very powerful platform with scale. There are numerous success stories of people who have started with producing videos, gaining a following, and then starting a business / selling a product to subscribers. If management can scale this to 100k followers and beyond, this could be a great platform for lead generation for all the other verticals.

In my opinion, I think investors should focus more on the valuation vertical scaling, and treat project monitoring, developer management and the automobile valuations as an optionalities without pricing them in.

D: invested in family accounts, no transactions in the last 30 days.

I’m amazed by how confidently people can write such things about others they’ve never met. Especially on a first name basis. I feel it’s undeserving of this forum.

| Subscribe To Our Free Newsletter |