Sharing some of the notes that i had compilied some time back.

What is Lab Grown Diamonds (LGD):

-

There are two distinct methods to create Lab Grown Diamonds.

- The high-pressure, high-temperature (HPHT) method: Gem-quality lab-grown diamonds are created in two primary ways. The high-pressure, high-temperature (HPHT) method simulates the conditions of a natural diamond’s growth. With this method, a diamond seed is placed into a chamber along with carbon and a metal catalyst. The assembly is then compressed with anvils and heated up, creating temperatures of 1300–1600°C and pressures of 5–6 GPa

- Chemical Vapor Disposition (CVD): This method enables scientists to grow synthetic diamonds using moderate temperatures (700°C to 1300°C) and lower pressures. Carbon-containing gas is pumped into a vacuum chamber, depositing onto a diamond seed and crystallizing as synthetic diamond. The eventual size of the diamond depends on the time allowed for growth. The growth process typically takes 4-6 weeks.

Most of the HPHT rough used for jewellery manufacturing is imported from China. CVD equipment cost is lower than HPHT equipment. India exports mainly CVD diamonds and diamond studded diamond-set jewellery using both HPHT and CVD diamonds.

LGD Technology landscape:

WD Lab Grown Diamonds (alias M7D Corporation) is the exclusive licensee of a portfolio of patents covering single crystal CVD diamond growth technology developed by The Carnegie Institution of Washington.

- Patent No. 6,858,078 (February 2005) – covers CVD diamond growth using microwave-plasma

- Carnegie patent RE41,189 (April 2010) – reflects a high-pressure, high-temperature annealing process that improves a diamond’s visual qualities

Seki Diamonds (Cornes Tech) is possibly the biggest/advanced manufacturer of microwave plasma CVD systems. LCD reactor typically costs $175,000.

Also, Seki has expertise in diamond seeds which is one critical component for output quality.

Lab grown diamonds: Supplementary or substitute:

Industries tryst with synthetic diamond is not new. In late 80s, industry experimented with Cubic Zirconia and Moissanite. However, those were far behind on physical, chemical properties. A cubic zirconia does not contain carbon, so does not qualify as a diamond. Cubic zirconia is less hard and does not look quite the same to the naked eye, unlike a lab diamond, which has the same look and physical properties as a natural diamond. Diamonds score a perfect 10 on the Mohs scale of hardness, while moissanite is between 9-9.5, and cubic zirconia 8. The refractive index of cubic zirconia is lower than a diamond, 2.2 vs. 2.42. Moissanite actually has a higher refractive index (2.65 – 2.69)

However, Lab Grown Diamonds are ticking most of the boxes both on properties and 4C attributes of diamonds.

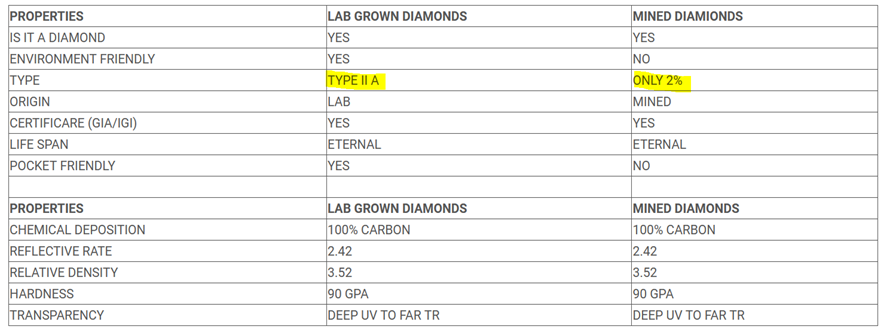

Diamond Purity grading:

- IA diamonds contain Nitrogen (N) atoms in clusters. Approximately 95% of natural diamonds are type Ia diamonds.

- IB diamonds contain Nitrogen (N)atoms as isolated atoms instead of clusters.

- IIA diamonds have no measurable Nitrogen (N) or Boron (B) impurities, just pure Carbon (C). Less than 2% of mined diamonds are type IIa diamonds (Kohinoor and Hope Diamond). All lab grown diamonds are type IIa diamonds.

- IIB diamonds have Boron (B) as their trace element.

Key reasons adding shine/legitimacy to Lab Grown Diamonds (specifically the CVD based LGD):

- Most importantly, A CVD produced diamond is mostly Type IIa (2a), considered to be the purest category of diamond. (no nitrogen and/or Boron impurities). Whereas only 2% of the natural diamonds fall into type IIa (2a).

- The Federal Trade Commission (FTC) has amended the guidelines to classify both natural and Lab grown as ‘diamonds. They have decided to drop the word “natural” from the definition of diamonds thereby putting both LGD and earth extracted diamonds at same footing.

- Premium industry body like GIA are employing the same terminology to grade lab grown diamonds.

- Industrial diamond initself is a BIG enough category. According to the US Geological Survey, 90% of diamonds used in US industries come from labs. Simultaneously, most geological diamonds used in industrial processes come as a by-product of producing mining gems for jewellery. The customisability of lab-grown diamonds makes them ideal for the needs of industry.

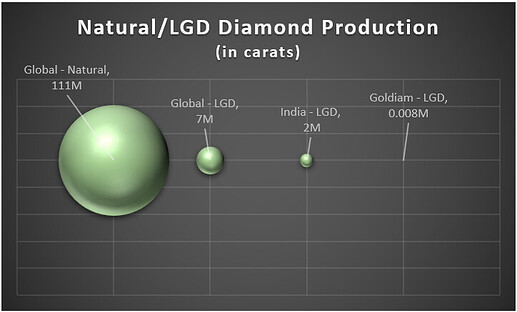

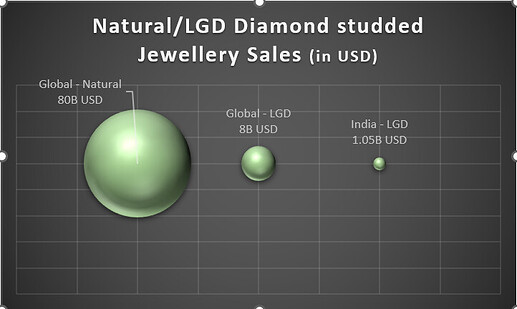

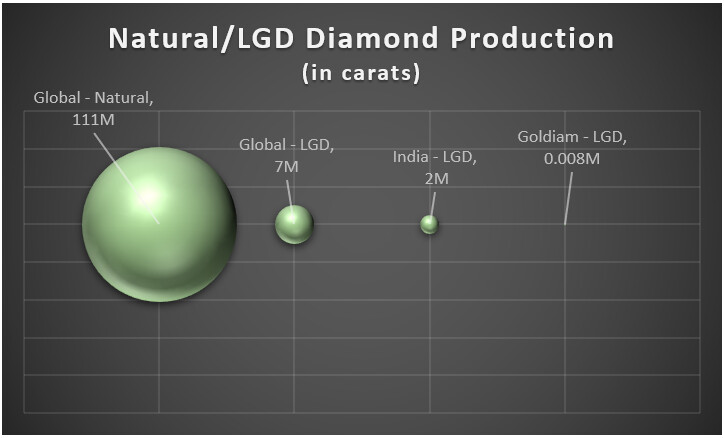

Market size in USD/carats and Growth projections:

-

In Carat Terms: Seven million carats of lab-grown diamonds were produced in 2020 worldwide. Out of that, 1.5 million carats were made in India. Approx 7800 carats by Goldiam. All these numbers seem tiny compared to the 111 million carats of Natural diamonds.

-

In value (USD) terms: Global lab-grown diamond jewellery sales could top $8 billion in 2022 and near the $10 billion mark by 2023. In contrast, polished natural diamond is pegged at $27B and polished diamond jeweller segment is pegged at ~$80B.

India LGD key players: size and scale:

Industry sources estimate that there are currently < 20 growers in India with a combined capacity of 3,000 CVD reactors with each reactor carrying a capacity of churning out 175 carats per month, which is minuscule compared to the demand. As expected, Indian CVD manufacturing is concentrated to Surat, Jaipur and few in Mumbai.

According to the Gem & Jewellery Export Promotion Council, India exported $1.05 billion worth of polished lab-grown diamonds from April 2021 to January 2022, registering growth of nearly 113 percent. Further, polished lab-grown diamonds witnessed a growth of 105.58 per cent to Rs 2,499.95 crore ($325.45 million) in April and May 2022, as against Rs 1,216.06 crore ($164.52 million) in April and May 2021.

India based LGD players who has access to WD Lab grown patented technology by way of sub-licencing agreement with WD Lab:

- Ethereal Green Diamonds LLP (“EGDL”) and its affiliate The Diamond Library.

- ALTR (India) Private Limited and ALTR Inc

- Evolution Diamond

- Goldiam is indicating that it has perpetual sub-licencing agreement for the patents (may be reference to WD Lab patent).

Other key players (may be without WD Lab patent agreement) are:

- GreenLab Diamon LLP whose Revenue is estimated to have increased to around Rs 229 crores in fiscal 2022, from Rs 65 crores in fiscal 2021 and Rs 20.6 crores in fiscal 2020

- Bhanderi LabGrown

- Cupid Diamonds

Trade channels across the globe are embracing LGD with serious effort and investment:

-

Signet Jewellers, the world’s largest retailer of diamond jewellery with more than 2900 stores in the U.S. alone (plus another 650+ in Canada and the U.K.) under well-known names such as Kay Jewellers, Jared and Zales. They have 6% market share in US jewellery and watch market. Signet so far has been selling Lightbox LGD collection from De Beer’s. They piloted the program with e-commerce business, James Allen. Have expanded market reach by selling loose lab-grown diamonds at its upper-mid-market Jared and Kay brands.

Signet CEO Gina Drosos had previously indicated the company’s appetite for a move into the

lab-grown market. During a conference call with analysts last year, she said the company would ensure it was “well positioned to participate in that space”. -

Based on Tenoris data, less than 19% of US independent jewellers sold lab-grown diamonds in January 2020. Currently, about 50% of specialty retailers sell jewellery set with these stones

-

De Beers subsidiary company Lightbox Jewellery exclusively sells synthetic stones made by another De Beers company, Element Six. Element Six is investing $94m in a new synthetic diamond manufacturing line in Oregon, US. De Beers seriousness for LGD can be gauged by its predatory pricing (dated article)

-

In May 2021, jewellery company Pandora announced it would use only synthetic diamonds.

-

LUSIX, a leading producer of lab-grown diamonds (LGD), announced that high-profile investors, including LVMH Luxury Ventures, Ragnar Crossover Fund and More Investments, have completed an investment round of $90 million. The new facility will enable LUSIX to better serve the increasing demand for LGD, from its clients worldwide and from the overall industry.

-

Just a year back, a trade show organized by Lab-Grown Diamond and Jewellery Promotion Council (LGDJPC) in India generated business of Rs. 5000 Crores within 4 days of exhibition.

Goldiam Edge:

-

SCS 007 certification: The SCS-007 Standard, developed under an international multi-stakeholder process, establishes a uniform basis for independently assessing and certifying the environmentally and socially responsible production and handling of all diamonds, whether mined or laboratory grown. Key Jewellery retailer like Signet/De Beers has a comprehensive responsive sourcing protocol covering aspects like ‘no blood diamond’ and environment neutrality. So far, following four LGD players have got the SCS 007 certification: Green Rocks, Goldiam USA, Lusix, and WD Lab Grown. Also, two retailers have initiated the certification process: Helzberg Diamonds and Swarovski. Interestingly Goldiam is a longstanding supplier to Helzberg.

-

Vertically integrated: Goldiam is perhaps only listed player covering entire value chain. They grow, cut, polish diamonds, design and manufacture jewellery in-house that is distributed through their U.S. office. Vertical integration adds ~20 percent to our bottom line.

-

Deep connect within LGD eco-system and retail distribution channels. During one of the past concalls, Goldiam management had indicated about getting empanelled with world’s largest Jewellery retailer (was that referencing to Signet??). This is beyond the current 5 large retailers that Golidam is working with. Management feels that each of them are big enough to procure LGDs between USD 5M to USD 50M.

-

Capex Glide path: Management has been indicating about taking LGD segment to ~50% of revenue in next 3-5 years. Towards that, capex announced of Rs 100M which will extend the existing capacity by 35% – 40%. As per management commentary, this entire expanded capacity is based on confirmed order commitments. Additionally, management is guiding for an additional INR 300M – 400M capex within 1 year to double the existing LGD capacity.

-

Guidance for ~40% standalone profit distribution by way of buy-back and dividends. Have been walking the talk so far. As a result, promoter shareholding has increased marginally over period of time.

Key Negatives:

-

Legacy Income Tax issue (most of the info is available in public domain).

-

Eco-friendly LLP is the primary vehicle for them to carry on the Lab Grown Diamond cultivation business. Looking at the related party transaction, looks like value-add work is happening between Goldiam Intl to Golidam USA. However, for that to be true, there must be some entries to record purchase of LGD from Eco-friendly to Golidam Intl. There is no purchase from Eco-Friendly LLP under related party transactions. Only related party transaction with Eco-Friendly LLP is by way of rent receipt of ~6Lac per annum. Therefore, little unclarity on the flow of good and material from accounting perspective.

Another possibility, transactions are happening directly between Eco-friendly and Goldiam USA

circumventing standalone Goldiam intl books. This looks little unlikely as share of profit from

Eco-Friendly Diamond LLP is just 5.91 Crs only. (under other income). -

First trench of 50% shares of Eco-Friendly LLP were acquired in Q3’FY21 however, investor presentation represents this during 2015-18. Why this misrepresentation?

-

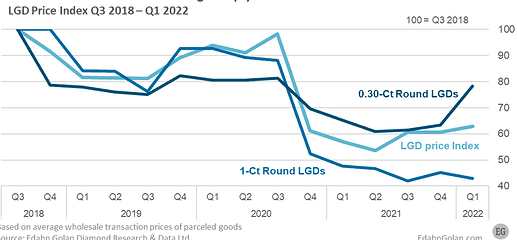

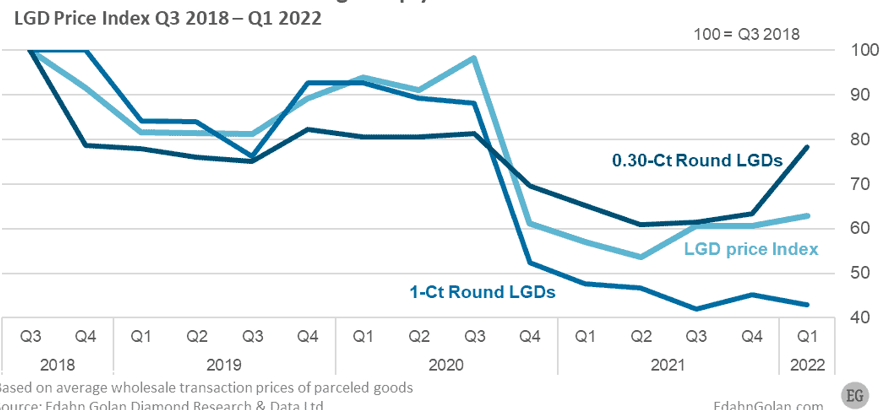

Loss of value: One of the study suggests that LGD price has come down to 60 points when indexed to Q3’18 price. In fact 1 Carat plus segment is worst hit where prices has crashed to 40 index points. Goldiam is predominantly into 1+ carat size LGD. This price erosion is expected to further accelerate with tech improvement and competition heating up. Will the LGD industry be able to offset the price erosion by expanding market further. Even then, what is the impact on margins?

Concluding Thought:

Lab grown Diamonds space is looking fascinating. Keeping perception and emotional aspects aside, LGD are turning out to be technically very close to real natural diamonds. As one of the key investment considerations, total addressable market is HUGE – covering complimentary fashion category first and eventually eating into bigger Natural diamonds territory as substitute play. Goldiam on its part can do great considering the early mover advantage and capturing full value chain by way of vertical integration. On the flip slide, considering the sharp price deteriorating cliff, it will take a lot of market expansion, volume growth just to maintain top line numbers.

Disc: No investment.

Some of the data points may be bit dated since did this self-documentation ~1 Year+ back.

Thanks,

Tarun

| Subscribe To Our Free Newsletter |