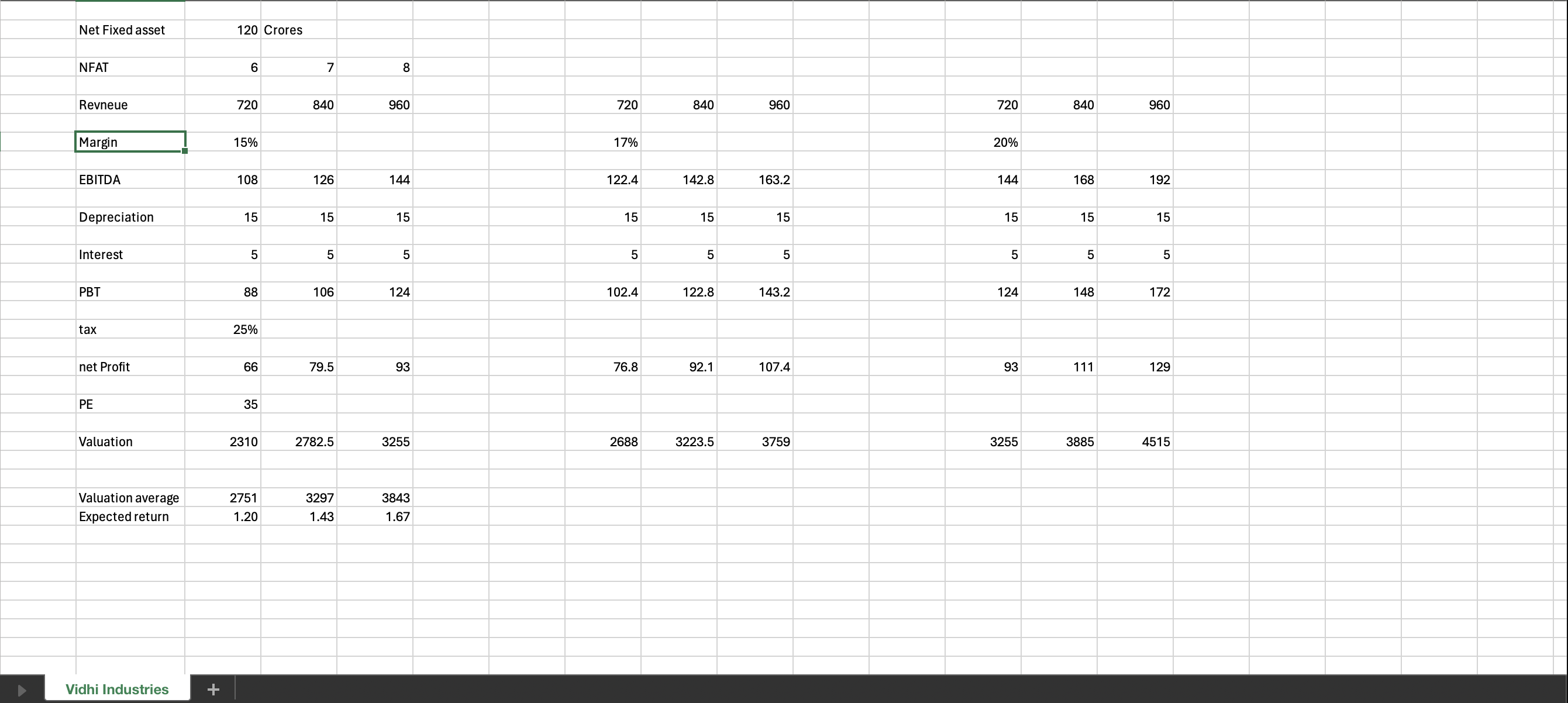

The current valuation seem to have factored in the base case of 6x NFAT turnover and 12% margin (from manufacturing revenue) at 35x PE (historical 5 year average) at an EBITDA margin of 15% (a bit conservative while management is guiding higher margin)

Key valuation drivers are higher NFAT (7x or above) and margin expansion (17 – 20%)

Please note, I have excluded the trading revenues while arriving at NFAT turnover.

| Subscribe To Our Free Newsletter |