Q4FY24:

• Long-term borrowings reduced from ₹36 Cr to ₹14 Cr

• With Uganda contributing to 60%, India 16%, Nigeria 12%, UAE 10%, and Tanzania 2%, Unihealth’s total revenue stood at ₹50 crores.

• Incorporation of its subsidiary company, ‘UMC Hospitals Pvt Ltd’, on May 22, 2024. This expansion marks a strategic move for Unihealth Consultancy Limited into the healthcare sector within India and providing healthcare services to the Indian populace.

• The Company will be commissioning specialized services like IVF, ophthalmology, and cardiology at its existing hospitals in Uganda and Nigeria and expanding its operations in Tanzania and India.

• The Company has incorporated subsidiaries in India (UMC Hospitals Private Limited) and Mauritius (Unihealth Holdings Limited) in furtherance of the same and plans to increase its commissioned bed capacity by 150-250 beds by setting up UMC Hospital facilities in Tanzania and India before the end of FY 2024-25 – To be commissioned by Q3-Q4 FY25.

• The manufacturing unit planned by the Company in Mwanza (Tanzania) is also set to be commissioned for commercial production during this financial year

•

• Target countries for expansion include Ethiopia and Kenya, showcasing a broader vision for geographical growth.

CONCALL NOTES:

• UniHealth presently has projects with a combined bed capacity of 1,250 beds under various stages of execution, spread across India and multiple countries in Asia and Africa under its consultancy division.

• EBITDA MARGINS: We’re sure of maintaining these EBITDA margins with a slight upside in the coming years with addition of specialty and superspecialty services because these services are going to be utilizing the same infrastructure. A lot of the manpower costs are going to get negated because we won’t need additional manpower at the management level for these services and the top line, the addition to the revenue is going to be significant. So, on an individual basis the addition of these services will allow us to operate them at a much higher EBITDA margin allowing us to improvise the overall EBITDA margins.

But definitely as we expand and as we grow and as we add newer facilities and additional hospital beds in India and elsewhere, these new facilities for the first 12 to 24 months are going to witness lower EBITDA margins because they are going to be in the initial phase of their operation. So, they are going to have margins which are going to be significantly lower compared to what we are achieving today.

But on a consolidated basis as UniHealth, an upside in the existing business and the lower EBITDA margins in the new business while they mature. So, on a consolidated basis, we still are confident enough that we will be able to maintain a 30% to 33% EBITDA margin on the overall business.

The second benefit of the EBITDA margin that we expect to come in the coming years is also from our consultancy business. The consultancy services operate at a much higher EBITDA margin. So, with a growth in that particular vertical of the business as we grow forward is likely to offset any reduction in the EBITDA margin because of new facilities being added and their nascent period being countered. So, on a consolidated basis, yes, going forward, we will be expecting the company to maintain a similar EBITDA margin if the upstate is not significant in the coming 24 to 36 months when we are going to be in a high growth modality.

• LOCAL PARTNERS: As a standard principle for all of our overseas venture, we do not go solo. We have always ensured that we have a very strong local partner who is able to help us navigate the initial bureaucratic challenges and is able to offset a lot of local challenges at various stages that the project is likely to encounter. But these local partners also come in with their investment on a proportionate basis. So, definitely they are also investing, allowing us to reduce our capital outlay for a project. They also come in with significant bandwidth to help us leverage and explore the possibility of taking local debt, both for CapEx and for OpEx if required. So, that is another advantage that our local partners get. Going forward for our expansion also, we will be taking up local partners.

As a policy, we do not go for a stake which is less than 50% or in fact, now we have re-modified that and we will be looking at a stake of 51% or upwards for UniHealth and the proportionate stake, 49% or lower for the local partner.

They definitely sit on the Board, some as Non-Executive Directors and maybe some as Executive Directors as well. But there are two critical important principles that we have and we have had always ever since we started our expansion. One, as the brand UMC is the ownership of UniHealth Consultancy Limited, we extend this brand. There is an operation and management contract and agreement in favor of UniHealth Consultancy and operationally, the rights reside with UniHealth Consultancy. So, we have complete operational control of our existing facilities and also of all the new facilities that we are looking at.

Also, the selection of our partners is such that none of our existing partners or partners in the foreseeable future come from a healthcare background. So, they are having very good local businesses which are from a non-healthcare industry. So, their interest is two ways. One, definitely to take the benefit of venturing into a high growth, high supply-demand gap present in the healthcare industry and second is also from a social perspective where they are presently enjoying a very good position within the industry on an overall basis and want to capitalize upon the social status that a healthcare facility offers in these geographies.

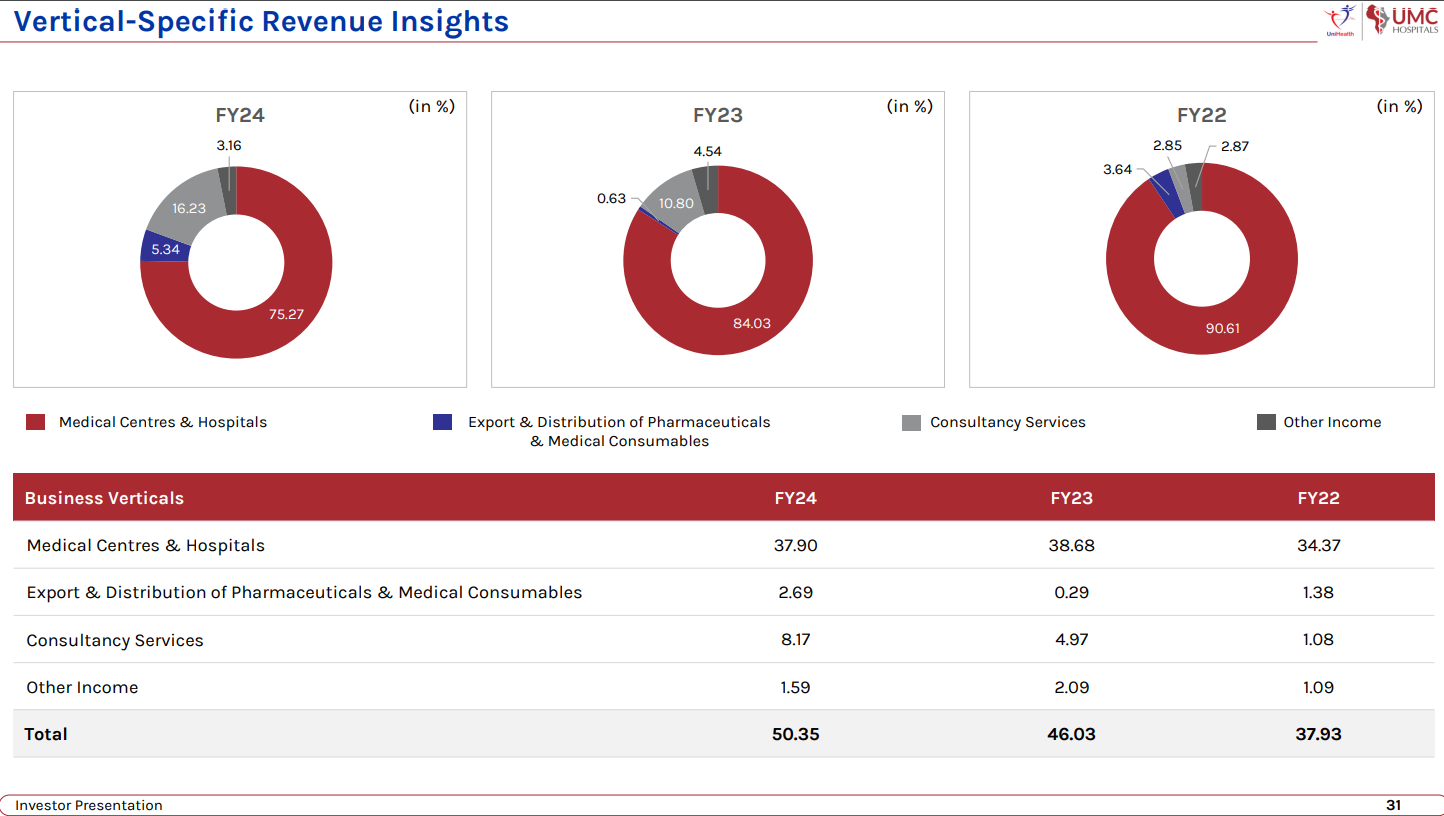

• CONSULTANCY BUSINESS: The consultancy business has contributed to 8.17 crores out of the total top line of 50.35 crores for Fiscal Year 2024. So, that is a good 16% plus that it has contributed. This is in comparison to just about 11.5%, 12%, which it contributed last year.

Going forward we do expect to gain considerably in the consultancy segment, both in terms of top line and bottom line. However, the innate nature, the inherent nature of consultancy business is such that we cannot have a straight-line prediction for it. It keeps varying. You may be pursuing a project for six months of a particular fiscal year, but the revenue will be realized only in the next fiscal year.

So, EBITDA margin, now typically what happens for consultancy services is that we have a very good strong professional team. Now with addition of new projects, addition at the team level, the major cost in a consultancy services vertical is the manpower. So, at the manpower level, we are not required, or we don’t need to add on the senior managers and senior professionals on a per project basis. What addition happens is happens at the ground level. So, that the OpEx for that is not considerable compared to the revenue generation from a new project. So, till the time we are adding on another two or three projects, our existing team with minor additions is able to cater to it. That is why the overall EBITDA margins and profit margins for this vertical are significantly higher, almost twice that of the margins that we have from the medical centers and hospitals vertical.

Right now, we are doing projects in India, we are doing projects across Africa, we have a project ongoing in Myanmar. So, this again, you know, though the entire execution, to a large extent, happens from the corporate office itself, from India, we don’t require to put people locally on ground. They manage via video calls, and they manage via sporadic travel to these project sites. But we are able to cater to the requirements of a clientele which is spread across Asia and Africa.

• ASSET LIGHT MODEL: Going forward, from an expansion perspective, the company is wanting to focus on a capital or asset light model where we do not plan to invest into the land and building in terms of ownership. We will be looking at two modalities, one wherein we lease out the infrastructure, maybe invest in the required equipment and operate it under the UMC Hospitals brand. Second will definitely also be an acquisition of the operations and management of certain existing facilities, whether they are in India or in Africa, because for a variety of reasons, there are people who want to outsource the operation. So, we will be keenly looking at that segment of the industry as well, where we take up the management. So, we will be looking at that segment also where we take up the operations and management of existing hospitals, maybe invest to upgrade the infrastructure in terms of the facilities, services, equipment and operate them under the UMC Hospitals brand. Now whether they happen on a lease model or a revenue share or a combination will depend on a case-to-case basis vis-a-vis the project that we are looking at.

• WORKING CAPITAL CYCLE: From a working capital perspective, different countries are having a different healthcare model.

NIGERIA: in Nigeria, the cash patient base, the patients who pay upfront or immediately on delivery of the treatment services, that forms almost 65% to 75% of the patient base because insurance or credit market is not a big portion of the healthcare services model in Nigeria.

UGANDA: In Uganda, though the insurance market is not as big, there are a lot of corporate companies with whom we have got accreditations and we are empaneled with them and have been providing our services where the payment cycles can range from two months to about six and a half, seven months depending upon the client that we have.

TANZANIA: Out there, the national health insurance is very well established and their payment cycle is roughly around 90 to 100 days.

INDIA: In India, there may be facilities where we are catering to the requirements of a lot of government schemes where again the payment cycles from the government departments can vary between four months to roughly around eight, eight-and-a-half, nine months as well. And there may be certain projects where we may not be catering to government schemes where the proportion of cash patients is going to be significantly higher. Patients from cash and the traditional insurance, I mean the TPA-based patients, their payment cycles are way better.

So, going from country to country, that model keeps varying and accordingly, our working capital requirement keeps changing where in Nigeria working capital requirement is significantly lower. It is just about I think 55 to 60 days. In Uganda, that goes up to almost four, four-and-a-half months. So, it keeps changing.

• Going forward, we will be expanding in different markets where though Uganda will continue to grow, the contribution to the top line and bottom line from that particular geography is likely to come down. The target for us is that by fiscal year ’25-’26, the contribution from a single geography does not exceed 25% to 30% to the consolidated financials of the company. So, with that particular target in mind, the expansion strategy of the company is being structured and formulated.

• GROWTH GUIDANCE:

FY25: The existing business is likely to grow on the same model that it has been growing over the last three years. On an overall basis the target will be to grow between 15% to 25% in the top line for FY ’25.

FY26: By FY26, the addition of 200 to 250 beds that we are likely to commission in FY25 is going to take complete shape and the revenue generation from those beds is going to get added on to the consolidated books of the company. So, that addition is going to be significant. Right now, we are working with an operational capacity of 200 beds and we are generating the revenues that are reflected on the books. By Fiscal Year 2026, we would have added on at least 200 more beds, if not more. So, we do expect the revenues to double up by that fiscal year.

• NIGERIA CURRENCY DEPRECIATION: If we look at a consolidated basis, this year though the revenue upstream has just been around 9% to 10%, in a local currency format, the growth has been much higher. This was a year where in Nigeria we witnessed a 40% depreciation of the currency compared to the previous financial year. So, though the revenue growth for Nigeria was 40%, because of the depreciation in the currency, we were not able to actually reflect that picture on the consolidated books in India. Going forward we expect the currency to stabilize as well in this year and that is likely to then translate into a better growth percentage compared to this 9.5%, 10% from the existing business.

Had the currency been stable, the overall consolidated growth would have been somewhere between 15% to 20% on the top line and even the profit after tax would have been higher than what we have been able to achieve at this stage.

• DISTRIBUTION VERTICAL: The second modality for our growth would be to focus upon the export and distribution vertical where we are able to add on more products, more companies and complete the registration processes so that we are able to distribute their products in a much larger volume than we are currently achieving.

From that perspective, we have been continuously engaging leading manufacturers in India. We are in discussion to add a few more companies with a fairly distributed range of products but which fit very well in our long-term perspective, and we have also initiated the registration of the manufacturing plants with the respective authorities in these countries. For example, Reliance Life Sciences with whom we have a distribution arrangement, we have initiated the registration process in Uganda and the site inspection for the facility has also been concluded earlier in April this year. So, we are on track.

• SUPERSPECIALITY SERVICES WILL AUGMENT CASH FLOWS: A majority of these specialized services, for example, if I talk about IVF to begin with, we are looking at an average revenue per patient in the range of $4,500 to $6,000. And these kinds of treatments are usually paid for in cash by the patient. There is no credit. There are no insurance coverages. There are no corporates which are actually paying for these.

So, the generation, if I am looking at a reasonable target of doing about 100 to 150 cycles at each of these locations in the first year, first 12 months of the commissioning of services, in that case, I am looking at about a million dollars plus, which is going to be a direct cash payment from the patient.

Same goes for a lot of cardiology and ophthalmology services where there is a significant patient flow coming from foundations, funders, sponsors. Very typical to what we have in India where small children are requiring cardiac procedures for the hole in the heart, what we commonly call, are funded by some of the other organizations. Same goes for cataract surgeries. So, these kinds of procedures are usually not offered on a credit basis. So, that will significantly augment the cash flow for the company

• CONSULTANCY SERVICES WILL ALSO AUGMENT CASH FLOWS: Consultancy services work on a very standardized cash flow modality where part of the service delivery is based on a signing fee or an upfront advance payment and the remaining is structured in either monthly payments or if it’s a shorter cycle in terms of the service delivery, then immediately on execution of the said service, which is usually between two to four months. So, that particular vertical is also likely to support the cash flow significantly as we embark upon expansion and addition of new hospital beds, which is likely to offset this benefit in some form where we may have credit cycles of about 90 odd days when we talk about countries like Tanzania where National Health Insurance is a significant funder for the treatments.

• In the short-to-medium term of our growth, we do not intend to be associated directly with government hospitals wherein we are taking up the operations or management or investing in any form in the government hospitals.

• Now we expect the currency to be significantly stable. I mean, this depreciation of the Nigerian Naira was enacted by the Nigerian government to align with a lot of international funds and international pressure for the recovery of its overall economy. And now we expect stabilization of that currency. So, in this fiscal year and going forward, there will be a significant addition to the top line and bottom line from Nigeria in view of the continued growth that we are experiencing out there.

• De-risking or managing the depreciation of the currency:

What we do is all the frontline base category services, for example, the room charges or the consultation charges are kept as per the market standards.

But for all specialty services procedures, surgical conditions, ICU charges, which are the major revenue generation points for the company, we continuously revisit them, and we compare them with the existing exchange rates and we continue to change or alter our, amend our service charges based on that.

Unfortunately, for this year, the nature of depreciation was so sudden that it was not practical for us to align all our service charges in one go. So, over the last six or seven months, we have been in that process where to a large extent today we have aligned our cost charges for a lot of procedures in line with the depreciated currency rate so that we are able to offset this particular risk to a large extent going forward as well. So, this is a practice that we have been following considering the nature of currency depreciation risk that we have in Africa.

Also to offset that particular risk, we are expanding our footprint both in India and in certain other African countries like Tanzania and Kenya, which are geopolitically fairly stable, with a historical currency risk also on a much lower level compared to Nigeria and ensure that the contribution to top line bottom line does not cross 25%. So, the company’s dependency is not there on one particular country or currency going forward

• For example, in Nigeria, we have upgraded and created orthopedics and spine as centers of excellence for our facility. Our Indian doctors started visiting there, conducting a lot of surgeries and seeing a lot of patients from January onwards. So, we had the first visit of their planned in January. Then they visited again in April. Now that benefit in terms of the growth of numbers is likely to happen from now onwards, because January being the first visit, you know, there were a lot of challenges in terms of getting the patients to get the funds in place for their treatment. But by the time the patients, I mean, the doctors visited again in April, a lot of those patients came forward with the funding required for undergoing these specialized services like spine surgeries, joint replacements, knee, hip, everything. So, in that case, now going forward when the doctors revisit in June, the surgical numbers, the total revenue from that particular department is going to witness a further uptick. So, this nature of healthcare service model also is reflecting on the overall growth in terms of the numbers, where going forward, now that we have been able to deploy some funds and we will be deploying our other funds as well in terms of expansion of facilities, services and bed capacity, in this particular fiscal and in the fiscal next, after this, we do expect a significant rise in the top line and bottom line compared to what we have achieved between FY ’23 and FY ’24.

• PRESENCE IN AFRICA AND COMPETITON: First point where our presence in Africa, we consider it the opposite. We don’t consider it as a weakness. In fact, it is a strength because we have been able to penetrate and create our position in countries where the healthcare supply-demand gap is massive. There is a growing need and demand for quality healthcare services where the EBITDA margins are significantly higher than we have in India.

So, that, in fact, for a company of our size is a very big up-stick because business like Apollo or a Max or a Medanta find it extremely difficult to penetrate into these geographies and establish themselves. Apollo for its own tried. It went into Mauritius. That got called off after a few years. That unit was not very profitable for them. Medanta tried in some East African countries. Same was with Shalby. But none of them were able to actually make a lot of profit from these units. Their entire focus eventually was aimed and remained at getting patients from those countries to India, which now the local establishment is not really keen to look at in a positive manner. They want their own healthcare infrastructure to be developed.

That is why there is a lot of support that we get from the local governments out there. For example, in Uganda, we are the only facility which is approved and empanelled by United Nations to cater to their requirements for nearly seven or eight different countries in the neighborhood. And they pay a significant premium to us just because of our available infrastructure and the service delivery. But the potential for growth out there is immense.

We don’t see challenges or threats in terms of competition coming that easily because the entry barriers both on ground and from a perception basis are significantly high. So, it is not so easy for a company to consider that let us make an investment in Africa today. There have been announcements. There have been scenarios where Apollo was awarded land parcels in Dar es Salaam in Tanzania to put up a hospital. There were announcements in the public domain, but that facility never came up, and now this is almost more than 10-12 years old.

So, we have that benefit where we have the opportunity to enter into and consolidate our position in about 3 to 5 countries in Africa and grow that particular business vertical of the company to a sizable level where tomorrow there are lot of strategic collaborations that can be looked into with Indian hospital groups which are big in nature or even with a lot of hospital groups out of Singapore or Malaysia because everyone is viewing at Africa in a very positive manner.

It is just that it is too tedious for the big players to go in and get the work done on ground. Their costs are much higher because a CEO from an Apollo or a Max or a Medanta will have to be paid at least 3 to 4 times what I will be able to do. So, I am able to contain a lot of my costs in that manner because of the pure size that we have.

Again, Apollo, Max, Medanta, Shalby, they all focus upon 150 and above bed strength because of the scale that they have already achieved out here. It is not economically viable for them to look at a 60, 70 or 100 bed facility, which is not the case for us, and which we over a period of years in terms of experience have understood do very well in Africa. Anything, in fact, above 150 beds is like a white elephant out there. It is not very easy to manage. But a 75 to 125 bed is something that breaks even within 12 months, is significantly profitable and easier to manage. So, that is the African part of the business.

• INDIA: Now coming into India, definitely we are looking at an asset light model. We are not looking to invest heavily into the land and building. Out here also the company is looking at a bed strength ranging from 50 beds to about 125 beds, again a segment which is very, very fragmented.

So, today, all the established big players are present in the 200-bed capacity and above majorly. They do have smaller facilities of about 160, 175 beds in tier 2, tier 3. But majorly their focus is on bed strength which is above 200 beds.

Second comes the specialty centers, which are focusing only on mother and childcare or a single specialty like HCG, which is focusing on cancer care, or some of them focusing only on IVF.

But a tertiary care multi-specialty facility between 50 to 125 beds is very, very fragmented where whether it is in Mumbai or in tier 2, tier 1 or tier 2 cities, you have got a lot of these individual doctors who’ve put up facilities, who’ve grown. They own a single facility, and now they are looking at a professional setup to come in and help them capitalize upon all the hard work that they have done. So, that is the kind of model under O&M that we are targeting. We are looking at.

Over the last 12 months, our market assessment interactions have been very fruitful in giving us a deep insight into this particular segment of the industry. So, there are a lot of available opportunities. It is only a matter of time whether UniHealth or someone else puts its foot in to this particular gap and creates a brand out of this 50 to 125-bed strength hospital capacity on a regional or a pan India basis.

So, Apollo had bought out, you know, there was a chain called Nova, which today is Apollo Spectra, which is a daycare cum 10-15 bed facility. So, it did try to dabble into that particular segment, though today it does not really form a major part of Apollo. It has continued its focus only on the bigger centers.

| Subscribe To Our Free Newsletter |