Amrutanjan produces and sells ayurvedic OTC healthcare products. The company’s 100% subsidiary AHCL makes the chemicals for the products. The CMD of the company is Mr. Sambhu Prasad who took over 9 year back. The company is more than 100 yrs old and was set up in 1893. Earlier the company used sell only the yellow pain balm. Everyone in South India knows this company and must have used the pain balm. A few years back the company undertook a re-branding exercise and launched a white pain balm. It also acquired Siva Soft Drink which owns the Fruitnik brand.

From the FY14 Annual Report

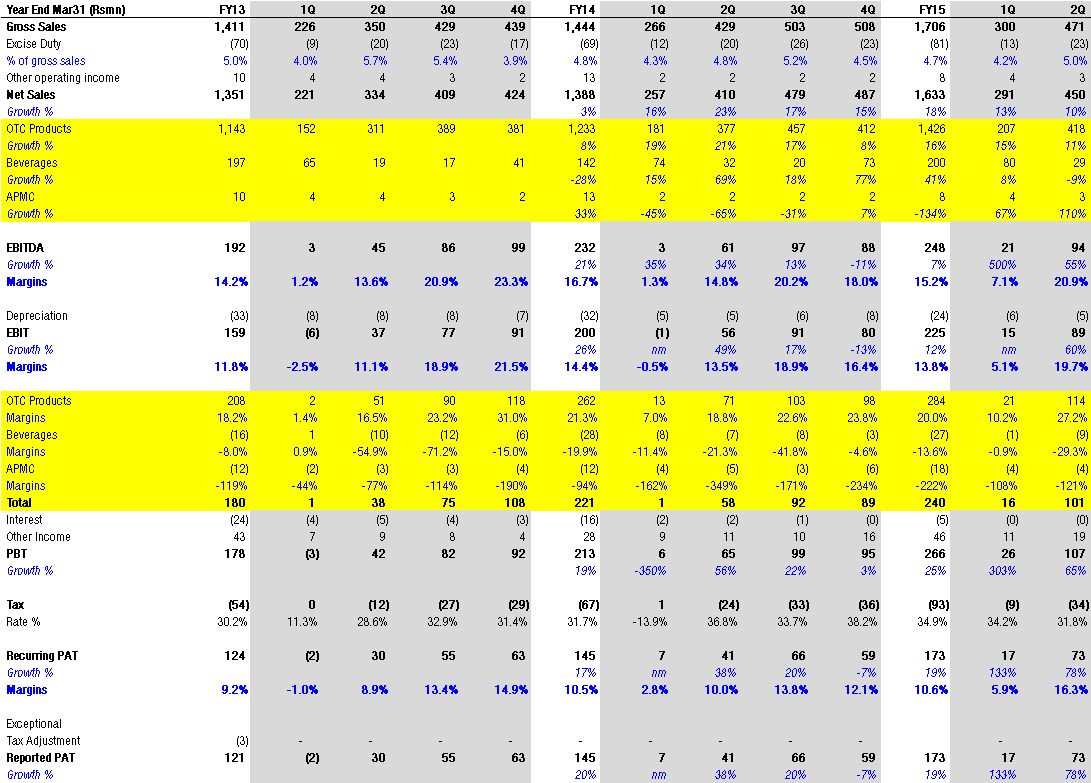

We wish to grow the next 3-5 years at a CAGR of 33%. This is bold. But looking at the past, one can argue we are trending in the right direction. 2000-2005: 0% 2005-2009: 5% 2010-2013: 10%

Focus on Head , Body and Congestion areas for our core business and offer/build portfolios in each vertical. We wish to also expand on our smaller portfolio of other products like Sanitary napkins and foot care products(corn caps) that can grow by entering the distribution chain and reaching consumers. Once they individually reach a level of sales that is self sustaining brand investments can happen. We have other unique OTC products that will be entering the market space this year.

The challenges for a company our size is to match the investments in media attempted by our much larger competitors. We have to recognize that our nearest competitor is 10 times our size and two of the smaller brands have sold out to larger competitors in the last 5 years. This was a very dormant category till 2009! Inspite of these head winds we executed to sustain in this business. This industry is driven by investments in the brand and this is a fact. Share of Voice and Share of Market are correlated strongly. We wish to steadily increase our share of voice to a level that will help us build new brands, and sustain existing ones.

Key Investment Arguments

Even if company can sustain 15-20% sales growth (and not 33% like they are targetting) margins will expand meaningfully because of operating leverage which could lead to much faster PAT growth. You can already see the growth pick up in FY15 and 1HFY16 already.

684crs market cap company. Zero debt company and has net cash of Rs38crs. Pays 30-40% of profits out as dividends.

Has plant in Mylapore, Chennai which has been shifted to the outskirts of Chennai. The land available of 2.5 acres is worth upwards of Rs150crs. Dont know when it will be monetized though. In FY09 company sold land for Rs84crs and paid a special dividend and also did a buyback.

Key risks as I see it

Small company with a topline of just Rs171crs. Advertising is critical for sales growth. Dont know if it can spend and compete with the likes of Zandu. Chinese balms like Tiger is another area competition. Subsidiary which makes the chemicals for the balms is loss making. Consolidated profits are Rs2crs lower than standalone profits.

Big investors in the stock already

—-Vijay Kedia of Atul Auto fame

—-Sundaram Mutual Fund.

Company website

https://www.amrutanjan.com/index.html

Disclaimer:

—-Have only done research based on publically available data and not met management.

—- Am invested in the company so my views might be biased.

| Subscribe To Our Free Newsletter |