Hi,

I have been studying Krishca for sometime now. Here are 3 major questions and some data in order to try and understand the business better. Please feel free to chime in with your inputs and feedback. Also, any other example of a small ancillary in an oligopolistic setup dependent on a big commodity industry will help

Q1. How will the business perform in a cyclical downturn?

Quick Answer → Signode India (biggest competitor) has shown consistent growth (9% CAGR) and more or less steady margins (16-19% PBILDT) over last 10 years. Thus, the business or industry seems only mildly cyclical based on this limited dataset

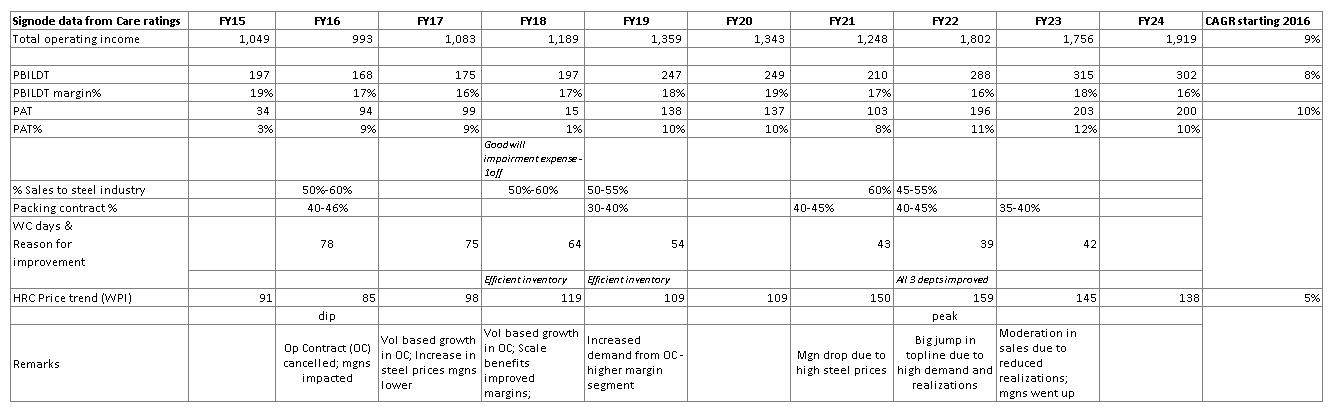

Details → I collated Signode India financials from care ratings report – available publicly – you can go to screener premium and find them under Tools → “credit rating reports”

Key observations:

-

FY16 was a cyclical dip for steel industry based on bottoming out of steel prices. Even that year, Signode did 17% PBILDT margins. Topline suffered a bit due to OC (operations contract) getting cancelled but impact was a mere 5% over FY15

-

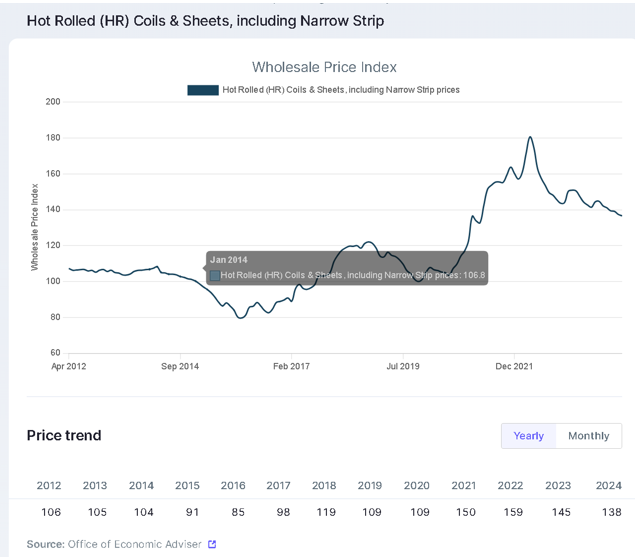

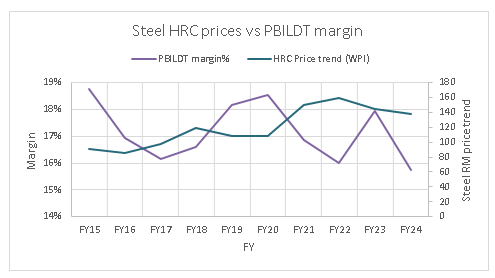

Over the course of last 10 years, Signode’s operating margins have been in 16-19% range. There is weak negative correlation of (-0.35) between steel prices and their PBILDT margins

-

Topline growth CAGR has been around 9% in last 10 years

-

Roughly 50-60% of sales is to steel industry and Packing contract (or OC) contribution to revenue has been roughly 35-45%

-

Working capital days have come down from 78 to 42 over last 10 years due to efficient inventory management

Q2. Does the business have any bargaining/pricing power?

Here is a snippet from one of the Signode India’s care ratings report:

Over the past few decades, industry structure has changed from a monopoly to an oligopolistic setup. Krishca promoter has mentioned in past that big steel players such as Tata, JSW, SAIL were desperately looking for new vendors to de-risk the supply.

Will the bargaining power hold? → looking for inputs

Going by theory of “Kinked demand curve under oligopolies”, prices are quite sticky since you want to deter a price war on one hand but also not increase price unilaterally since competitors will not follow. Comes down to relationship, product differentiation etc…

Q3. Is the opportunity size big enough?

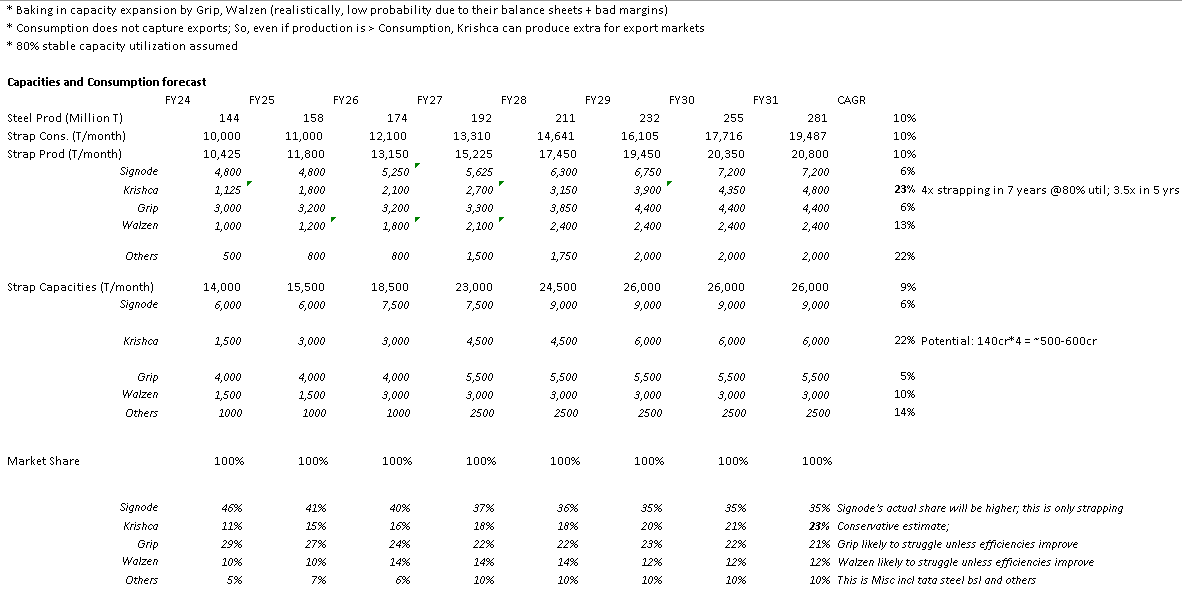

Quick answer → they can grow their domestic capacities and production by ~22% for next 6-7 years provided steel capacities meet their target growth & given, we don’t see import of cheap steel straps

This has been the most troubling question since the promoter mentioned in concall that Indian strapping market is only ~3000cr including packing contracts. Dubai market is another 300-400cr directly (without adding the potential to supply to Americas and Europe).

He has also mentioned that the company will organically grow into primary packaging. With no estimates and details on the size of this primary packaging market, competition intensity, margins etc., I tried to only focus on domestic strapping market and project the capacities and consumption based on steel industry growth assumptions. This could be an incorrect approach since steel industry projections are unreliable and should be taken with a pinch of iodized salt ![]()

Key Observations:

-

Base assumption – Steel production reaches ~250-300MTPA by 2030; Strap consumption mimics steel production that assumes no imports of strapping

-

Even if Signode grows its capacity by 1.5x in next 7 years & Grip, Walzen also put up 1 additional 1500T/month plant → Krishca will have space to 2x its current capacity base from 3000T/month (2 plants) to 6000T/month. This is conservative and not counting in the space for middle east expansion. A 4x capacity (since 2nd plant got commissioned recently in May; capacity till FY24 was 1500T/month that can expand 4x to 6000T/month) for steel strapping in 7 years would mean roughly 140cr*4 = 500-600cr of revenue potential just from steel strapping (22-23% CAGR)

-

Signode India has been paying heavy dividends back to its parent MNC. Not sure if this means they are not interested in heavy reinvestments in India and treating this subsidiary more like a cash cow for now; This presents an opportunity for Krishca to steal more market share through capacity expansions & getting to 20-25% market share in ~7 years

-

Grip seem to have a stretched balance sheet based on ratings report by acuity dated july 5, 2023 → this makes them unlikely to expand aggressively in future (assumption)

This is more of an excel spreadsheet based analysis. I will request fellow members who are tracking the industry closely or understand such dynamics to feel free and provide their views. Thanks a lot

@Rakesh_Arora @DEBASHISH @jitenp

Disc – for educational purposes. Invested but re-considering position sizing

| Subscribe To Our Free Newsletter |