This was indeed the reason. For a company like this, we shouldn’t be comparing quarters but years since they aren’t selling soaps or shampoos but executing large lumpy orders with different revenue recognition modalities by project.

The company came out with first investor presentation yesterday which is quite detailed unlike its ARs. There’s a definite intent here to grow the business and the market cap, with the hiring of high-caliber professional CEO and MDs and giving them hefty options and also hiring Valorem to help investor communications. Disclosures should only get better from here hopefully.

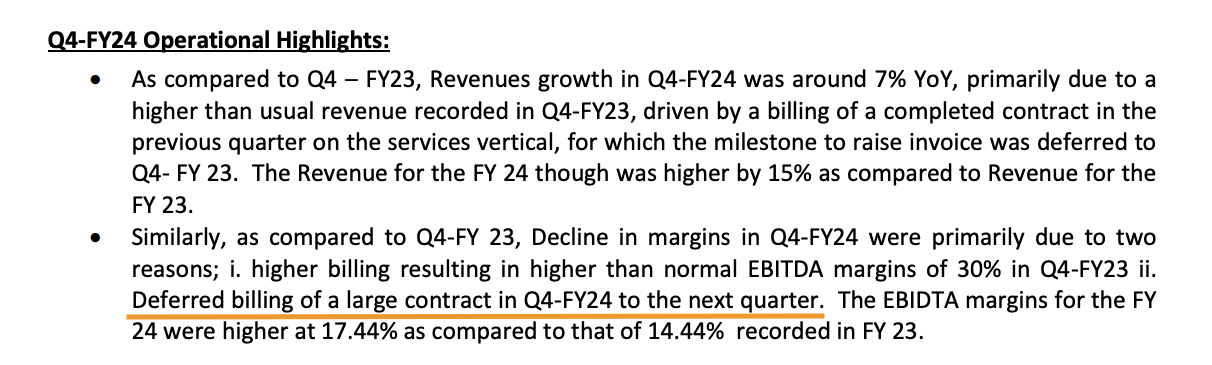

There’s also some very useful information in the PPT like the geospatial segment growth, margins and also segment-wise split-up. The margins in geospatial have gone up substantially in FY24.

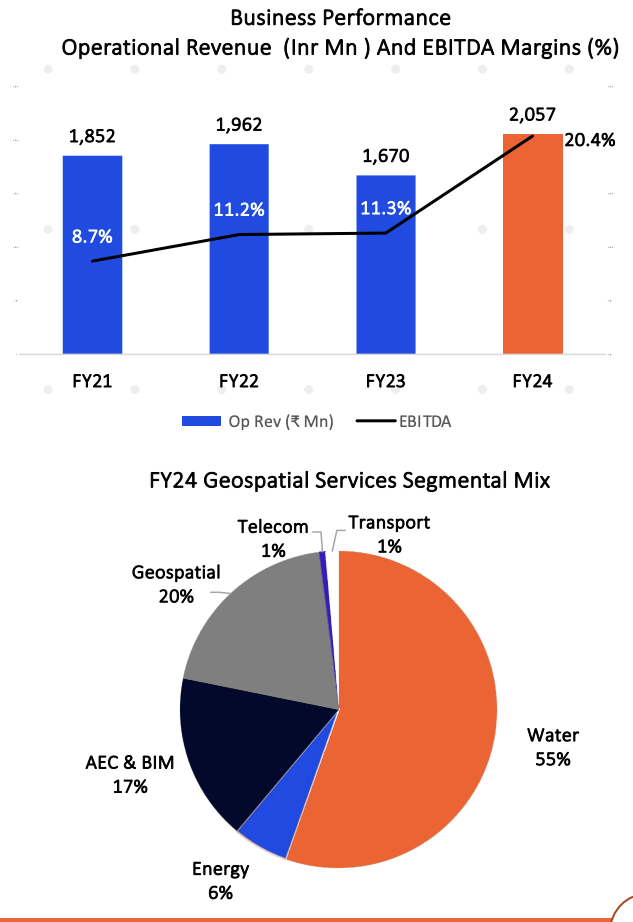

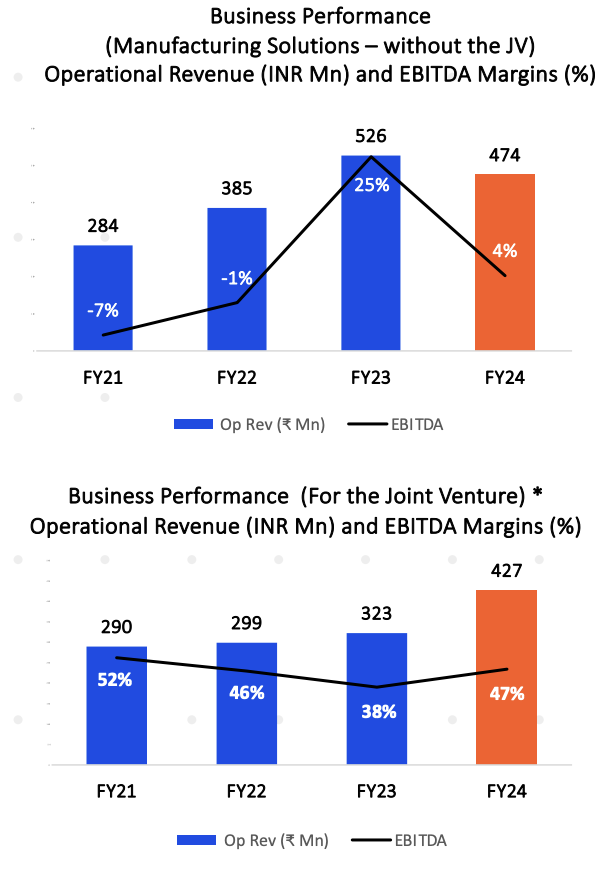

The performance of AllyGrow and AllyGram, their JV with Grammer AG. There’s a severe compression of margins in AllyGrow in FY23 while there’s healthy growth in AllyGram. Not sure if this is due to movement of business from AllyGrow to AllyGram but if its not, then an increase in revenue in FY25 could mean margins coming back in AllyGrow which could be a good kicker on top of geospatial business growth.

The order book position as well is updated. I had mentioned order book was 650 Cr. Looks like it stands at 710 Cr. The deferred large order in Q4 could show up in Q1 or Q2 and hopefully should lead to healthy growth. Overall I don’t see the business performing poorly but on the contrary, could actually be performing quite well.

Taal, Weekly – This is an old position which has been underperforming somewhat. There’s lot of volatility contraction and consolidation within that triangle last 6 months.

There was severe margin contraction in Q3 which led to big selloff post results but the margins are back this quarter back to 27% levels it used to be at.

Disc: Invested in both as disclosed before

| Subscribe To Our Free Newsletter |