-

Sir, what is the point if you don’t look up basic numbers? My previous posts have said standalone PAT was 396crs. I’m not going to post screenshot, you can check the standlaone FS for yourself. Standalone business refers to Food Delivery, which I used synonmyously in my previous post. Q4 PAT was 396 crs and the business is already at roughly 1700 crs ARR. Much of it is due to high other income, but the gap is expected to narrow as business grows sustainbly.

-

Adjusted EBITDA to PAT bridge is given in every shareholder letter and you can check how broadly the numbers are same since other income cancels out ESOP expense and rental expense etc… Given how they’re generating cash, I only expect it to inch up.

If you don’t see the fallacy in using the same PAT estimate for the next year, then its disappointing. Blinkit itself has broken even in March. So, Q1FY25 margins even on a console level will be higher due to normal trend up in Zomato and near 0-0.5% margin in Blinkit

- Sir again, how much capex? Blinkit itself is asset light due to FOCO model. Going out is built asset light. Hyperpure – granted is an asset heavy business. But how much capex? Total capex is not likely to be more than 600 crs in my view. That’s not a huge number in any way.

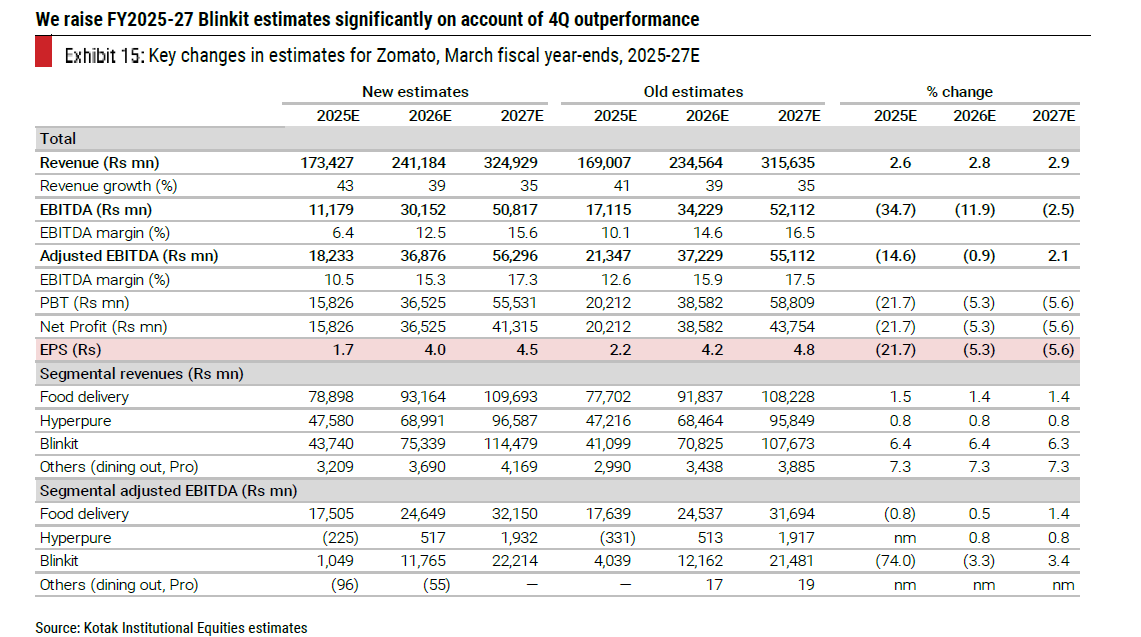

In any case, here is Kotak estimates for you

In any case, the beauty of markets is differing opinions. If its frothy, don’t buy or sell / I find immense value in these valuations right now given its a large cap.

| Subscribe To Our Free Newsletter |