Thanks for the reply!

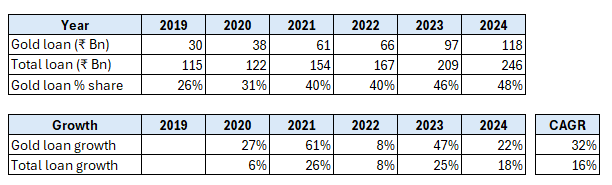

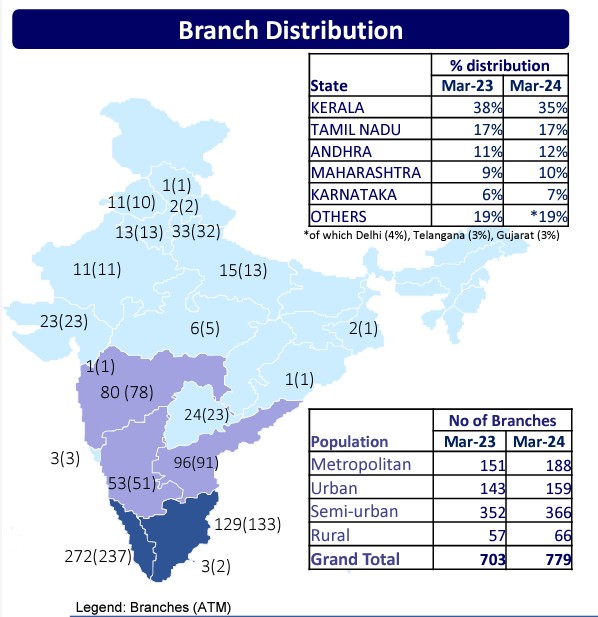

I did some more digging into CSB bank. I think I have identified one clear moat which has also been their growth engine for the last 6 years: gold loans. Since 2019, CSB’s gold loan book has grown 32% CAGR – going from 26% of their loan book to 48% at the end of Q4 2024. They have been able to do this, as they charge only around 9.5%~12% interest for these loans vs. Muthoot / Manappuram (the largest gold loan players) who charge 20%~25% interest. I think they charge less interest because they lend to more safe customers than Muthoot. This can be seen via their NPA ratios: CSB has 0.5% NNPA vs. Muthoot at 3% (meaning 6x more defaults at Muthoot). CSB’s gold loan book at ₹118Bn is 16% of Muthoot, who is at ₹729Bn. CSB’s moat here is low interest rates combined with being a trusted bank with a good branch network in Kerala and TN (seen below) – so people are not wary of trusting CSB to hold their gold safe.

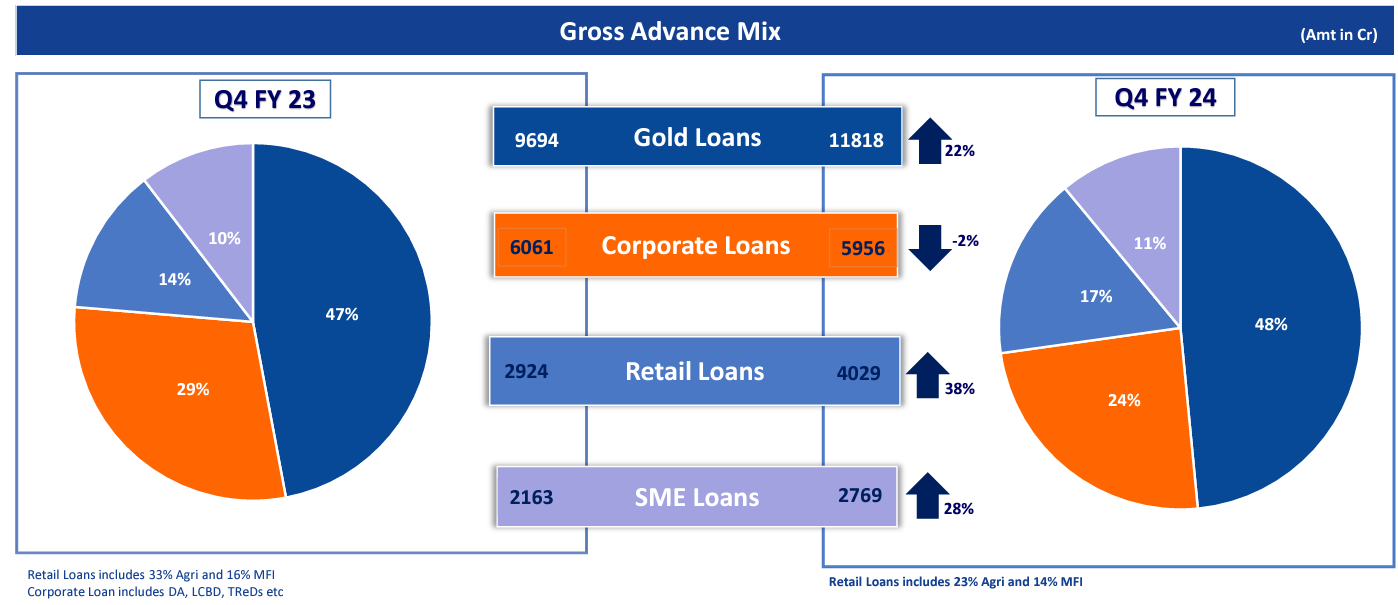

Pralay Mondal (CSB’s MD & CEO) is cautious about gold loan growth. My guess is that the pool of safe customers for gold loans is limited. So, I don’t expect them to ever reach the scale of Muthoot / Manappuram. Mr Mondal also mentions that he expects “wholesale” and SME business to grow faster next year (which can be seen already from Q4 2023 to Q4 2024). Gold loans have a higher NIM and lower net NPA than Wholesale & SME Loans, so these will potentially both be impacted if gold loan share of total loan book reduces. Link to the interview.

However, if they manage to maintain their NIM at 4%~5%, I don’t see a reason for concern. For comparison: HDFC, ICICI and Kotak have NIMs of 3.6%, 4.4% and 5.3% respectively, while Muthoot and Mannapuram have NIMs of 11.6% and 15%. I double whether the latter is sustainable long-term, especially when loan customers get more internet savvy and are able to compare loan interest rates across banks/NBFCs.

In summary, CSB seems to be a promising bank , which will grow at 10%~15%+ in the next few years, as India is still very credit-starved and more people will move up the wealth pyramid from low-income to the aspirational / middle-class.

Gold loans vs. overall loan book:

Retail and SME is growing faster than gold loans:

Branches:

Disc: Have decided to start a small position and monitor this stock in the coming quarters

Thanks,

Sharad

OpenSourceInvestor @ Substack

| Subscribe To Our Free Newsletter |