Q4FY24:

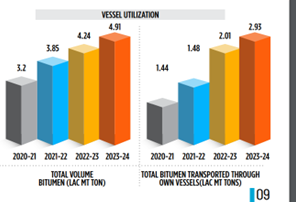

• FY24 Volumes: 4,90,813 MTs vs 4,23,925 MTs (15.78% growth)

•

•

• Company has plans to enter into the Bitumen market in North region of India, to increase its customer base and revenue

CONCALL NOTES:

• Our volume target for FY ’25 is set at 6 lakh metric tons, aiming for a 20% year-on-year increase. So we expect some increase of around 15% to 20% in terms of revenue.

• With capacity constraints in India for bitumen and AICL being the only integrated player in the private sector for bitumen, we have been able to increase our market share.

• India saw a 6% increase in bitumen consumption to nearly 9 million metric tons.

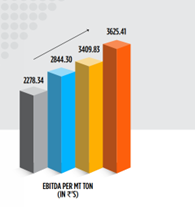

• Currently, EBITDA per metric ton is around INR3.625 which we expected to increase to INR3,800/3900 per metric ton, reflecting our ongoing efforts to enhance profitability.

• Our economies of scale achieved from own feet of bitumen logistics vessels and road transport vehicles enable us to outbid competitors, secure tenders and ensure high standards of supply and service to our customers.

• Targeting 65-70% volume through own vessels (60% this year) (25-35% growth)

• Red Sea is not a problem for us because we are not going towards that side. We are coming from the Gulf countries to India, where we do not fall in between Red Sea.

• BITUMEN REALIZATION DETAILS: The total realization for the entire year has been comparatively low. Last year, the total realization was around 42,000, which this year it is around 36,800. We have lost nearly about INR300 to INR400 crores of turnover due to the price fluctuations.

Realization for this year should be than FY24.

• So ultimately our dependency on third party will stay till the time we have in house capacity of around or more than 2 lakh tons.

• COMPETITIVE CHALLENGES: Challenges we don’t see a great challenge because the company is well positioned in terms of locations and the logistics advantage that we have. I don’t think any other player in the entire Indian state is having the setup that we have already built in the last few years. We just have to turn around the throughput from the storage tanks or the storage manufacturing capacities that the company is having. So, we don’t see a very good or much challenge from the market.

• We have always been focusing on forward and backward integration. So, in the coming future, maybe the company may produce bitumen on its own as well.

• Debt is always cheaper than equity. If there is any plan for the company to add more vessels in terms of capex, the company will not dilute.

| Subscribe To Our Free Newsletter |