Some valuation data purely from company’s own data sources –

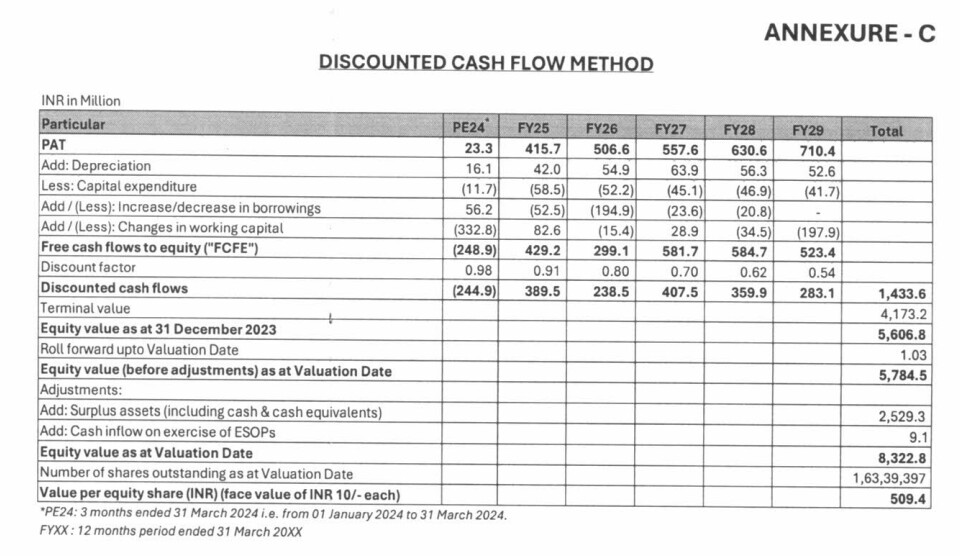

The DCF method accounted. Look at jump in PAT expected from FY25

source : https://www.ceinsys.com/wp-content/uploads/2024/04/Valuation-Report_Mr.-Shryansh-Jain.pdf

Based on these, Market Price per Share: INR 559.90

Current Total Shares: 1,63,39,397

Current Market Capitalization≈INR91,47,05,38,220.30

Now the company has also proposed to issue fresh shares and warrants to raise capital.

Share Warrants: 14,89,086

Equity Shares: 12,50,658

New Total Shares Post-Issuance

1,63,39,397+27,39,744=1,90,79,1411

After the issuance of the new share warrants and equity shares, the company’s total number of shares will increase from 1,63,39,397 to 1,90,79,141. This results in a dilution of approximately 14.35% for existing shareholders.

Current Market Capitalization: Approximately INR 91,47,05,38,220.30

Market Capitalization After Issuance: Approximately INR 1,06,83,25,63,959.90

The increase in market capitalization shows the additional capital raised through the issuance of new shares and share warrants.

But the market is valuing Ceinsys at 770cr. Is the valuation report off? Specially with the DCF method? Or is the company really undervalued as @phreakv6 pointed out in his thread?

Thoughts?

| Subscribe To Our Free Newsletter |