Hi Sumit,

Correct me if I’m wrong, have just glanced through the latest financial, ppt and concall:

-

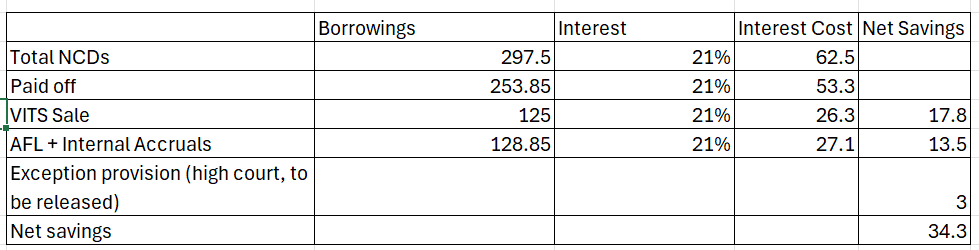

Net Savings should look like this subtracting 8.5 Cr of lease (this is from latest concall, not sure where 20 Cr number has been published)

-

Currently a bunch of unexercised warrants are still left to exercise from both promoters and investors, which would dilute the EPS

-

So, assuming a base case of 30% turnover growth as guided and translating the same to PAT growth @ 30% (Management has actually guided an EBITDA growth of 50%+ which is not far-off, assuming 7% ARR increase, 10-15% occupancy increase but let’s be conservative)

| Subscribe To Our Free Newsletter |