About the company

Specializes in: Original Design Manufacturing (ODM), Original Equipment Manufacturing (OEM) and Plastic Injection Moulding.

- Original Design Manufacturing (ODM) is a business model in which a manufacturer designs and produces products according to its own specifications and sells them to another company, which then markets and sells these products under its own brand name.

- Original Equipment Manufacturing (OEM) is a business model in which a company manufactures products or components that are purchased by another company and retailed under the purchasing company’s brand name. Unlike ODM, where the manufacturer also designs the product, in OEM, the purchasing company typically provides the specifications and design, while the OEM company is responsible for producing the product or component.

- Plastic injection molding is a manufacturing process used to produce large quantities of plastic parts with high precision and repeatability. It is commonly used in various industries, including automotive, consumer electronics, medical devices, and packaging.

Q4 FY24

Financials

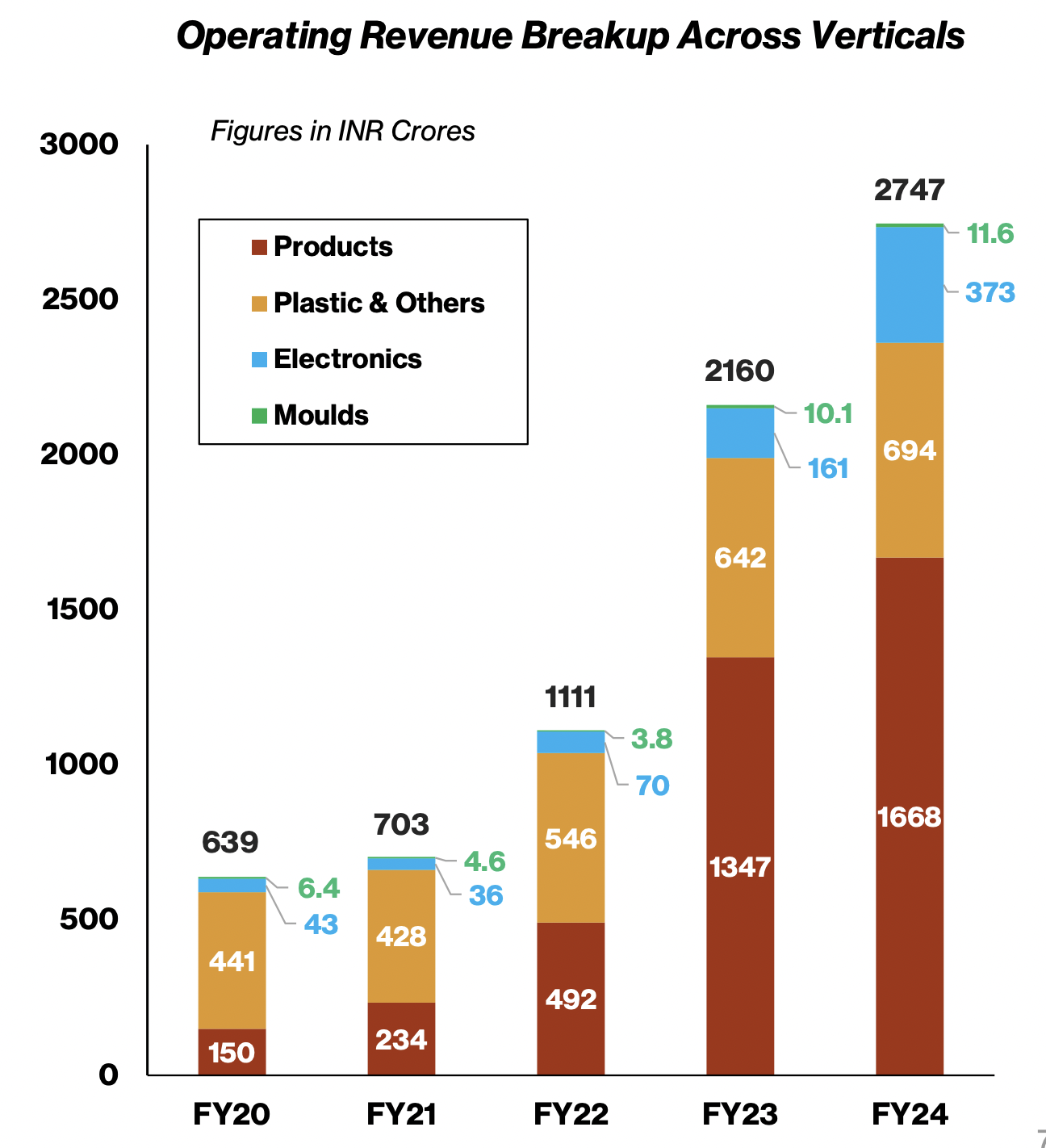

- The Product business contributed 60.7% of the total revenues in FY24. Room AC business at INR 1317 crores grew 26% during the period while the Washing Machines business had a growth of 20% YoY.

- PGEL’s 100% subsidiary, PG Technoplast, crossed INR 1456 crores in revenue in its third year of operations. Company’s Bhiwadi AC Unit became operational during the year

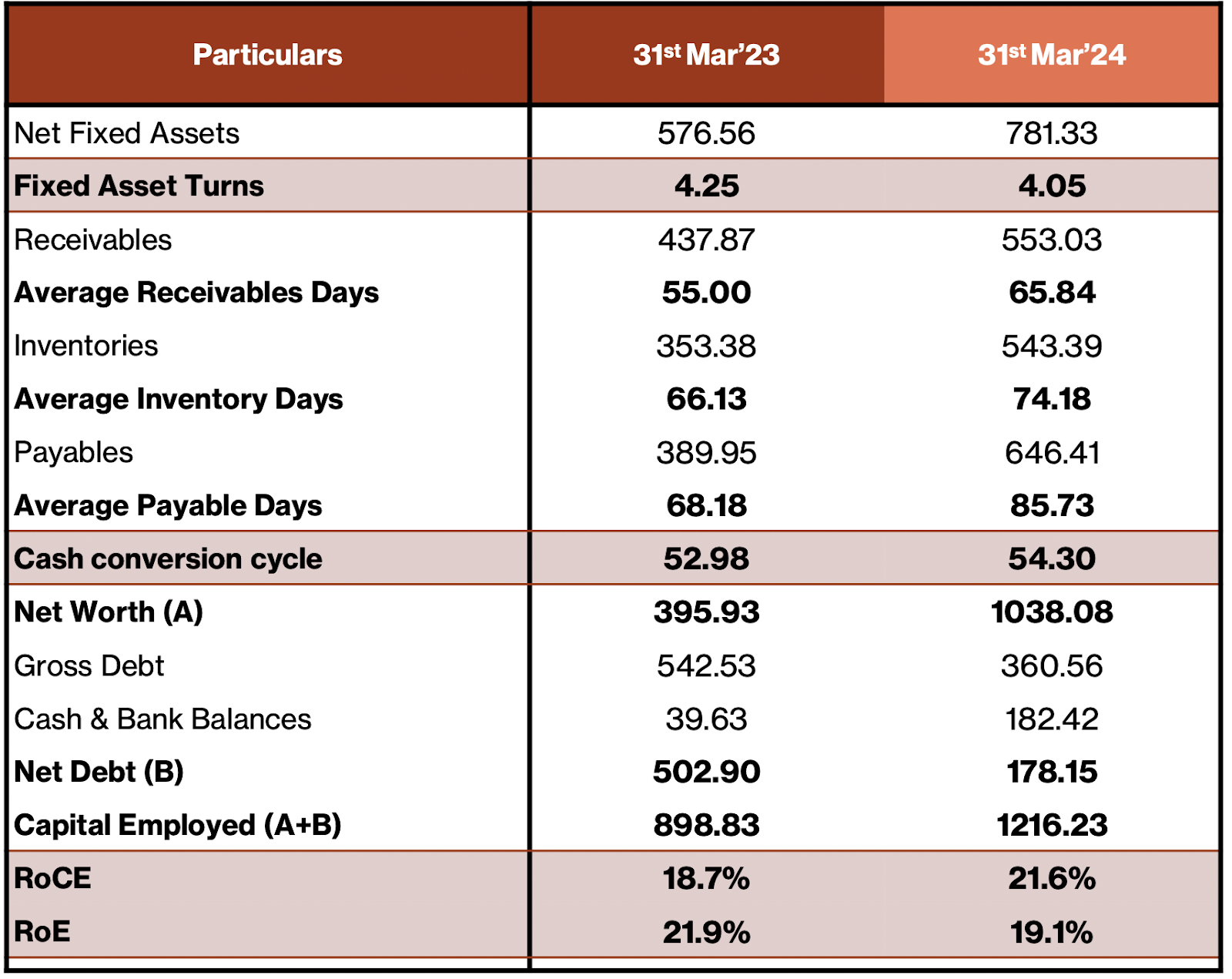

- operating margins have improved QoQ and YoY due cost control, softer commodity prices and operating leverage.

- Net debt has decreased by almost INR 325 crores in FY24 despite Capex and acquisition of NGM.

- The room AC business contributed INR1,317 crores, which is a 26% growth on a year-by-year basis. The washing machine business had a growth of 20% on a year-by-year basis, and coolest operating revenues were flat, largely because of steep fall in ASP

Business details

- The company has also forged a new JV partnership for the TV and hardware business, and the JV company, Goodworth Electronics, was selected for IT hardware PLI 2.0. Jaina had a Google ODM license which only two other people have in India Dixon and one more company. So that comes into the JV because of the JV with Jaina. Second thing is that they have very good sourcing capability because they have been the promoters earlier of Karbon brand and they still own the Karbon brand.

- Posted a 26% growth in product segment despite of the average selling price being down by 8%

- The room AC business contributed INR1,317 crores, which is a 26% growth on a year-by-year basis.

- The ASPs in the RAC washing machine and coolers were down significantly due to low commodity prices during the year and especially in the fourth quarter. Also, the business in the first half of FY24 suffered due to unseasonal rains, and despite these challenges, we have posted industry-leading growth in RAC revenues of 25% for the full year.

- 20 crores as a part of incentive is accounted for in the earnings

- This year, plastic molding is about 7.5% margin business electronics is about 2% and then the rest of the margin whichever way you look is coming from the product business.

- The business has seasonality because a high chunk of revenue comes from ACs, coolers etc and hence we cant extrapolate the margins of one quarter for the whole year. Q1 and Q4 are good margins because of high demand which leads to operating leverage.

- Our pricing is almost same as the competition or slightly in some cases slightly better than competition and we are not compromising on the pricing because we have some cost advantage or we have some PLI benefits as of now.

- In the AC revenue, 85% or so goes to branded players and the rest goes to private levels.

- When they take up a project, they aim for 15-16% pre tax ROCE

Outlook

- PGEL Net profit guidance of INR 200 crores which is a growth of 46% over FY2024 Net profit of INR 137 crores.

- FY2025, Management expects EBITDA margins to have slight upward bias because the TV business which is low margin in nature isn’t a part of the company anymore. Q1 will still have some inventory worth 40 crores to be sold but after that no contribution.

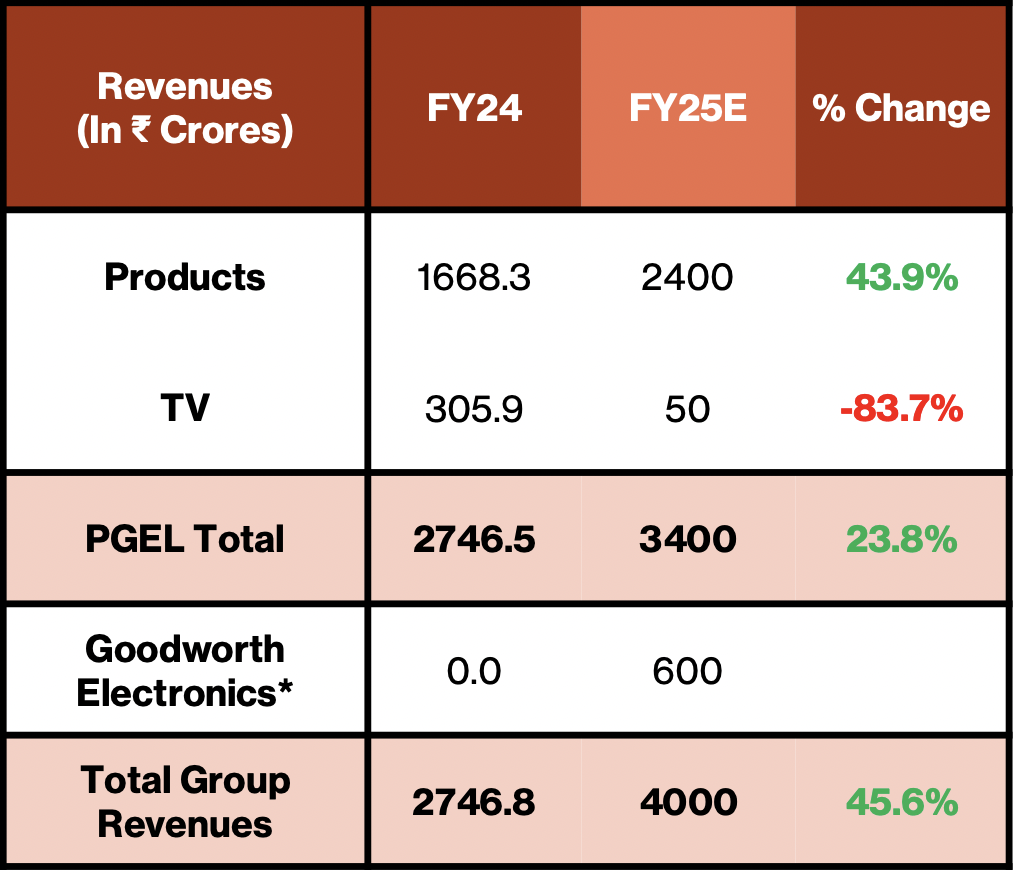

- The growth in product business i.e., WM, RAC and Coolers is expected to be around 44% to over INR 2400 crores from INR 1668 crores in FY2024.

- Capex guidance for FY25 is in the range of INR370 to INR380 crores, and the company has planned to further expand room AC capacity by setting up a new integrated unit in Rajasthan. It will largely be funded internally.

- hopes to accelerate the product business growth in FY2025.

- Aiming for 25-30% growth for the RAC business.

- total INR65 crores will get incentive next year. PLI of INR30 crores and INR35 crores-INR40 crores of state government incentive. Out of 200, around 30 crores is PLI scheme which was 11 crores this year.

- They want their asset turns to improve and expect minimum 4-4.5 of asset turns.

- Over the next 3-5 years, they expect the industry to grow 15-20% and they are also gaining market share so they believe they can grow around the industry average or a little higher.

- Employee cost should grow in line with the revenues, In the last 1 years, 2 years there has been significant portion in employee cost almost 10% to 12% in the last 2 years which is coming from the hit on account of ESOPs. So we have given quite decent ESOPs, almost 200 people in our company are covered under ESOP and we have taken INR15.5 crores hit this year which is a part of our employee cost because of the ESOP and therefore our employee cost looks slightly higher.

- In PLI: if we meet all the targets then next year the number is in FY25 we should

- get INR30 crores after that INR 36.5 crores then year after that INR51 crores and year after that last year’s number was INR60 crores. In case of state government benefits, the first year is going to be little bump up maybe INR35, INR40 crores and then year after that every year about INR20 to INR25 crores.

- If the seasonality isn’t very stark, can expect 25% ish ROCE

Risks

Industry

- why we are doing such a heavy capex, as I told you last year this year we are doing a huge capex on creating an infrastructure which is land and building for future growth. We are seeing some very exciting huge opportunities coming at our doorstep, which we are in the active stage of discussion with significant clients which are looking to shift their work to India from China and some clients which are looking to actually expand their relationship with us. Now because of that, we think that we are getting into a phase where the growth could be accelerating in the coming year and we may be short of infrastructure for growth, because ready sheds are not available typically for leasing out and therefore we need to create some of those optionality for us and that money is going into creating those optionality and that, we should be able to utilize most of it in the next 2-3 years in our opinion.

- We are seeing industry overall being slightly short of the capacity right now on the monthly demand which we saw in month of April, May and June probably. April, May, also there was a little bit of planning shortfall, nobody actually anticipated such strong growth in the demand and therefore people were probably not ready to take care of such a huge, I’ll say demand and therefore probably in the coming weeks or we will see some stock outs in some of the major brands, probably because the material is just not there.

these are just my notes on Q4. Very strong growth ahead. I wish I could have picked it earlier when it corrected.

| Subscribe To Our Free Newsletter |