Special situation –

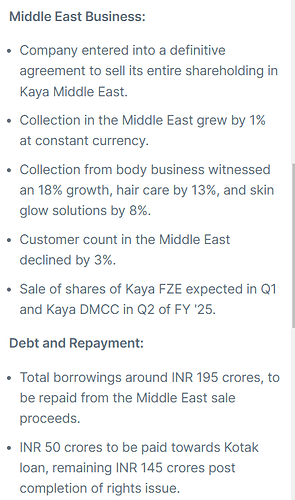

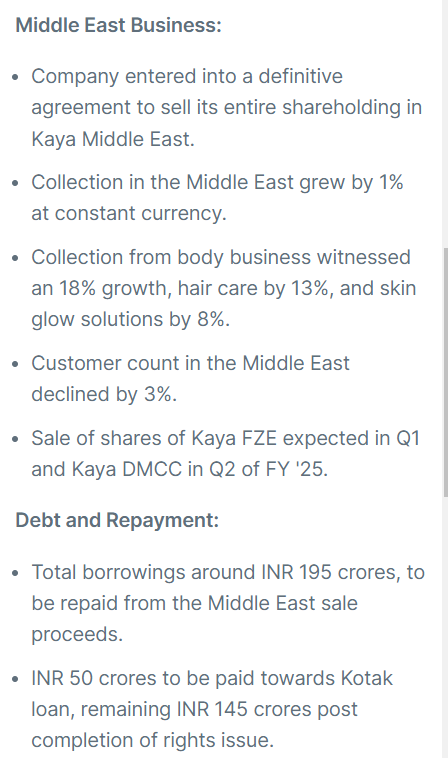

- Kaya have hived off loss making international operations

- Plans to be debt free business in next two quarters with total debt 195 cr being repaid by 50cr sales proceeds of international business and remaining 145cr through rights issue.

- India operations having decent growth and EBITDA margins of 28% should command good valuations hence getting rerating

- All india stores are profitable and guiding for rapid expansion.

- Needless to say promoters are Marico owners.

Disc – Invested this week.

| Subscribe To Our Free Newsletter |