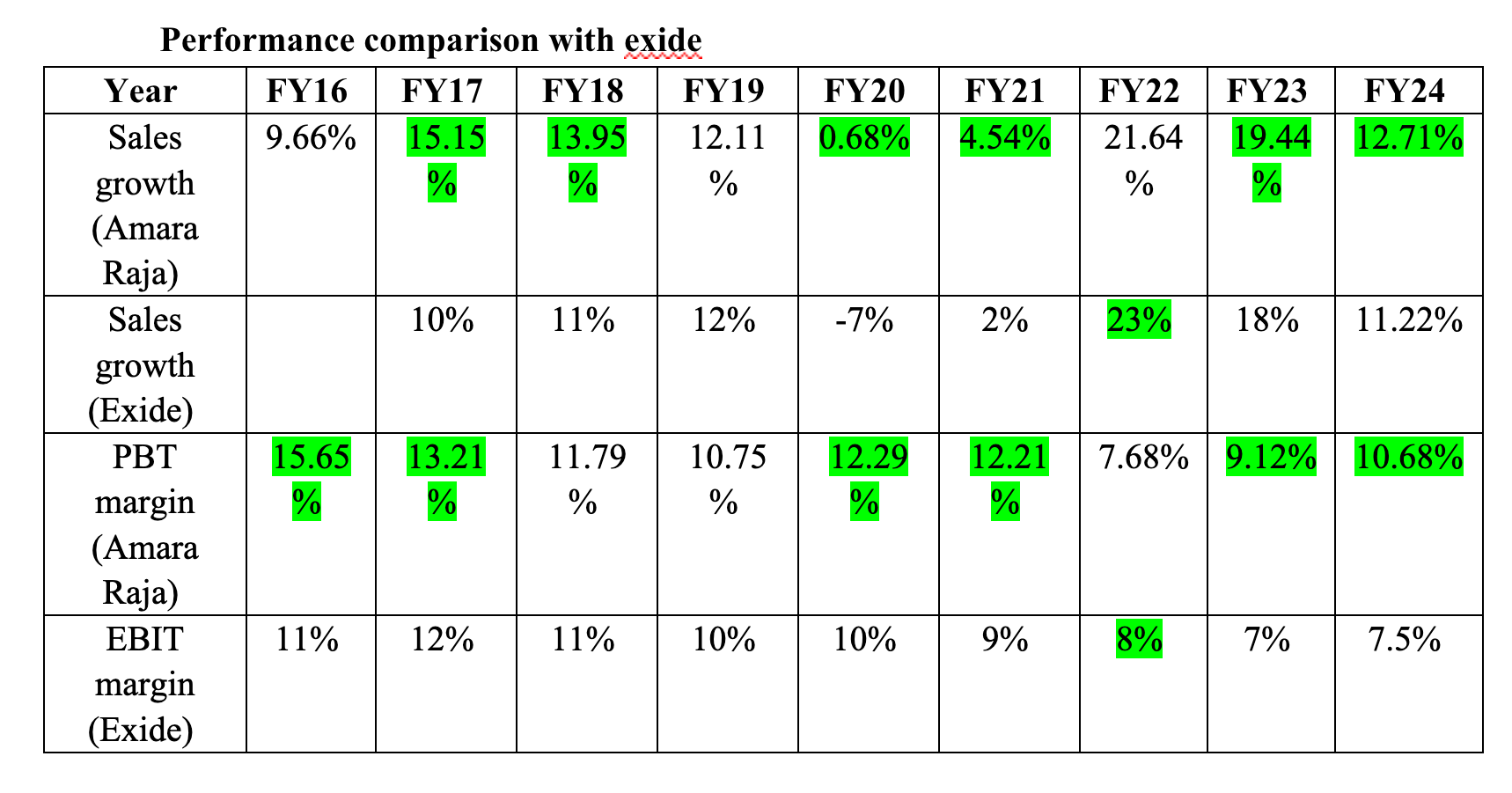

Amara came with good results with sales growing by 19.5% and EPS by 50%. They continue doing better than Exide. Concall notes below

FY24Q4

-

Lead acid battery : 16% YOY volume growth domestic + 30% exports

-

4-W volumes : OEM: 2%, after-market: 15%

-

2-W volumes : OEM: 15%, after-market: 18-19%

-

Industrial volumes : growth of 5-6%

-

Exports grew by 19% in FY24

-

Export growth is driven by new markets (USA/Africa) + APAC + Middle east. Ranked #1 in UAE and #2 in GCC

-

Made international inroads on UPS products in existing geographies in Southeast Asia and Middle East, and in Europe and North America

-

Trading revenue of 10-11%

-

-

New energy business :

-

116 cr. (vs 148 cr. in Q3FY24 and 88 cr. in Q4FY23)

-

FY24: 522 cr. (vs 249 cr. in FY23; 110% growth)

-

Batteries: 80%, Chargers: 20%

-

Invested 650 cr. so far

-

Commenced 2-W battery packs

-

Looking for partner with technology + R&D pipeline + reliable supply chain

-

Have submitted PLI application

-

Considering asset turns of 1.3-1.4x and 10-11% EBITDA margins, can get ROE of 12-15% once they reach 10-11 Gwh

-

Expect commercialization of 2Gwh line by end of FY26 (cost ~1500 cr.)

-

-

Lubricant : 25 cr. in Q4. Targeting 150 cr. in FY25 (same margins as lead acid). Reflected in standalone numbers

-

Related party mergers : Companies selling significant quantities to the listed entity has been merged or acquired. There is a construction company that will not be merged as majority of their sales comes from outside. An electronic manufacturing company providing home UPS systems going into Amaron Power Zone won’t be merged as its not seen as core

-

Distribution increased to 550+ franchisees and 115,000+ retailers

-

Battery recycling plant (150,000 MTPA capacity) – 80% completed, expect commercialization in Q2/Q3FY25. Consume 3 lakh tonnes of lead per annum with 70-75% coming from recycled sources. The plant will recycle both lead and plastic. Expect 2-3% increase in gross margins and 0.5-0.7% increase in EBITDA margins

-

Tubular plant (1mn+ battery capacity) should commercialize by Q4FY25

-

20 cr. one-time expenses due to stamp duty payments for merger with plastic division

-

FY24 capex: 800 cr.

-

FY25 capex: 1500 cr. (300-400 cr. lead acid + 1000-1100 cr. new energy)

Disclosure: Invested (position size here, sold shares in last-30 days)

| Subscribe To Our Free Newsletter |