In my opinion, Indigo story is at critical juncture for a new investor coming into it. FY23 and FY24 were years of continuing ASK growth, coupled with higher than pre-COVID yields/average ticket prices. All this happened when the industry has consolidated in hands of few players out of which Indigo is clear market leader with 60%+ share.

But I am thinking where this story could go now. For this, I was reading previous concalls and noted below points –

Revenue growth is function of ASKs and ticket prices. Ticket prices can change due to fuel costs and competition. Falling crude price is positive for an airline as EBITDA margins expand

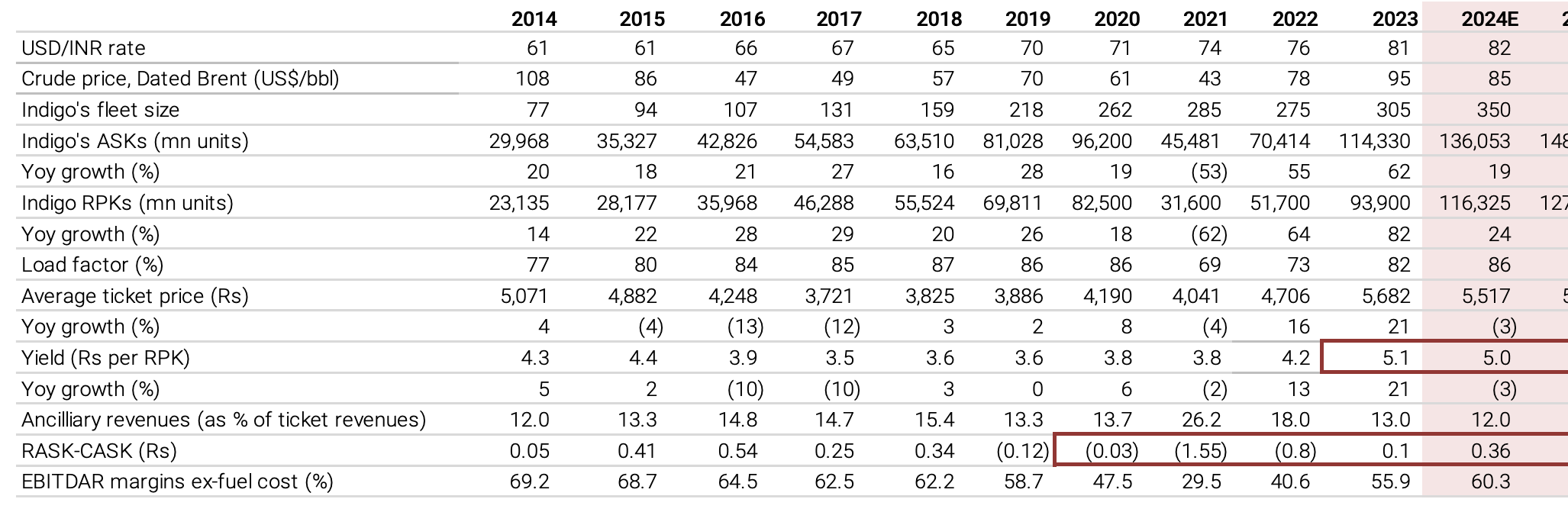

In FY16, ASKs went up by 21%, RPKs up by 27%. This meant that demand side grew faster than supply side for Indigo. Despite that Indigo had to reduce fares to remain competitive as fuel costs came down in FY16 from $86 to $47. Average ticket price came down 13%, hence yields came down 13% and the revenue growth was 15%. This also meant that margins improved from 14% to 20% due to lower fuel costs and higher utilisations.

In FY17, Indigo were pricing their fares higher than competition, and was focusing on yields. This meant that they left money on table and load factors declined. This decreased the RASK for Indigo

The year-over-year RASK growth that we have seen this quarter is a much better performance

than what we have seen over the past few quarters. It is important that I point out that in the June

quarter of last year, we did not execute optimally on our RASK performance. We placed a bit too

much emphasis on yields and were not matching competitors’ fares. Consequently, we saw a

decline in load factors and our RASK performance for the same quarter last year was adversely

impacted.

Buying power for fuel efficient airplanes can drive market share gains as when fuel prices go up, an airline with fuel efficient planes can outcompete fellow players on price and get market share or have better control on margins. This spins the flywheel of low cost airline leading to gain in market share

Management in FY16 – Look at actually what is probably going to end up happening. As fuel prices start going up and we have these more fuel efficient Neos, we will be able to display a big competitive advantage over players who will have the older airplanes and may not be able to sustain the kind of cost pressures that come with high fuel prices environment.

How competition affected the ticket price in Q1 FY17 and despite 20% higher ASKs, the EBITDAR margins and sales growth was both down.

We reported an EBITDAR of Rs.15.5 billion with an EBITDAR margin of 33.9% for the quarter ended June 2016, compared to an EBITDAR of 15.8 billion with an EBITDAR margin of 37.4% for the same period last year. We delivered earnings per share of Rs.16.42 in this quarter. We added two aircraft in the quarter including one Neo. Our total capacity of the first quarter, at 12.7 billion ASKs, is an increase of 25.1% over the same quarter last year. IndiGo’s total passengers increased to Rs.9.9 million in the June quarter, which is an increase of 20% over the same quarter last year. Our total revenue from operations for the quarter was Rs.45.8 billion and increase of 8.7% year-over-year. Our passenger revenue was Rs.39.7 billion, a growth of 6.9% versus the quarter last year and ancillary revenue was Rs.5.8billion a growth of 20.8% over the quarter last year. Our revenue per available seat kilometer or RASK for the quarter ended June, 2016 was Rs.3.62, down 12.7% from Rs.4.15 compared to the same period of last year. Our average fares reduced from Rs.4,524 from the June quarter last year to Rs.4,032 in the June quarter this year, which is a decline of 10.9% primarily due to increased competitiveness in the industry.

Despite high PLFs, competition has behaved irrationally in past and lower fares were offered.

Analyst: Hi Aditya, this is Pulkit here. Just a couple of questions. The industry is really at around 83% kind of PLFs so, we are surprised that there should be yield decline when the industry itself

operating at such high level PLF. So what is really happening out there? I mean you obviously

are the industry leaders and would have some kind of say in the pricing discipline in the industry.

But is it possible that small player can just come and disrupt the entire pricing?

Management: So Pulkit you can see that there is actually yield decline. So, as you expected it is actually happening. There is a yield decline and that is because almost everyone is throwing extremely low and competitive fares in the market place. In the past, we have not matched some of these fares and because of which we took a hit on our load factors. But as I just told Sonal, we might be rethinking that strategy now.

Analyst: I mean why would anyone need to lower fares in an environment where PLFs are already that high? That is what I am trying to understand.

Management: Good question, Pulkit. I guess this is question that some of our competitors can answer. But yes, it is the realty that we are seeing in the market place.

ASKs went going up but 2016-2019 period saw intense competition and fares/yields kept plunging. Average ticket price from top of 5014 in 2014 came to 3886 in 2019

Management in Q1FY19: The current revenue environment continues to remain weak particularly in the 0-15 day booking window. While we spoke about some signs of improvement in the last call, the fares continued to be lower in the quarter compared to the same period last year. We do not believe that these fare levels are sustainable, especially given the increase in input costs. Clearly with industry load factors in the high 80s or 90s, the industry is turning away passenger demand at current fare levels but we have no choice but to keep our fares competitive.

Despite higher fuel prices in 2019, fares were kept low by industry players and profitability of Indigo was severly impacted

This led to 50% correction in 1 year in stock price between 2018 and 2019

Business travel and business cities pairs were where yields were getting impacted most in pre-COVID era

We do not normally comment on route specific results, but what I would say is that as I mentioned before, the yield pressure we are seeing is primarily in bookings which is generally business traffic. And so, I think, as you would expect markets that typically have a lot of business traffic, we are seeing more pressure than other markets that are primarily leisure.

Plight of competition in business travel explained by management in Q1FY19

There are a lot of these cities pairs where there has never been non-stop service before and when we put capacity in there what we are finding is that there is quite a bit of demand. I mean, if you look at where we are with respect to load factors they are clearly very strong. So, the demand is there at the current price. The real challenge for us, as was mentioned by Rahul, is what is going on in the 0 to 15 day booking window. When we look at our sales outside 15 days we are actually seeing yields up year-over-year. So, the kind of pricing we are putting in the market to stimulate traffic is doing well. The challenge we are seeing is that inside 15 days the period which would typically be business travelers, who are not so price sensitive, where we would normally get higher yields, the competitive market is just not allowing us to get the kind of yields inside 15 days that we used to. I mean, it is a situation where historically airlines would use advance purchase parameters to low fares you have to buy outside 15 days. When you buy inside 15 days typically the fare is higher. Inside 7 days would be even a little bit higher. And that structure has worked very well for the industry over the years where we could take these high yields that we get from business travelers and use it to offer low fares to leisure travelers. And the problem we are seeing right now in the markets is that these sort of advanced purchase rules have been competed away and we are just not getting higher yields inside 15 days that we used to. So, our strategy is going to be that we are going to remain competitive because we do not have any choice. You have to be competitive in this market.

40% Fuel price rise in Q2FY19 & INR dep plundered the profitability.

Management: We reported an EBITDAR of 2.2 billion rupees with an EBITDAR margin of 3.6% compared to an EBITDAR of 16 billion rupees with an EBITDAR margin of 29.9% during the same period last year. As Rahul mentioned, our profitability was significantly impacted by cost pressures from the increase in fuel prices and the depreciation of the Indian rupee as well as from the competitive fare environment. The average aviation fuel price in India during the quarter was 40% higher than the same period last year. Fuel is about 40% of our total costs. After adjusting for the increased volumes, this increase in fuel price resulted in higher fuel costs of 9.1 billion rupees compared to the same period last year. The Indian rupee also depreciated significantly during the quarter and closed at 72.58 rupees per U.S. Dollar. Based on this, we booked a foreign exchange loss of 3.4 billion rupees compared to

a loss of 0.5 billion rupees during the same period last year.

Unfortunately, these higher input costs have not been recovered as fares remain low due to

continued intense competition.

Even fuel surcharge to pass on higher fuel cost was not adopted by industry despite losing money in 2019. Indigo had to remove it

Management: And I think at the end of May, it was that we put in a fuel surcharge. And so we made the first move, as it were, to increase the prices. But it was not matched by the competition. Everyone can have their own reasons for doing that. But as a result we have to withdraw that surcharge. And as, I think, Mr. Bhatia said earlier, we are not the people that are interested in having low prices, and we are doing our best to lead the yields up.

After reading pre-COVID summary and what has happened in last 2 years, the story has kind of reversed. But there have been two constant things –

- Indigo market share has been rising. It was 30-40% in 2015-2016 period, today it is 60%+

- ASK growth has been secular trend. I expect this to grow at 15-16% CAGR going forward as well.

Now things which changed –

- Prior to COVID, Indigo was fighting for yields with competitors who despite losing money were cutting ticket fares.

- Fuel prices went up and the industry still did not increase the fares. It was never the case that demand was off as indicated by high passenger load factors but the competition was just unhealthy.

- But after COVID, this has not happened so far. Fuel prices went up and Indigo was able to impose fuel surcharge on customers and the yields have largely remained stable.

- Indigo now dominates most of the routes it is part of.

- Flywheel of lower costs bringing market share with margins has played out perfectly so far in last 2 years.

But what if

Tomorrow crude prices rise substantially due to some macro event –

- Indigo and others would pass major portion of it to customers. This seems more likely scenario. But even in this case, there could be some price increase that may not get passed off and that would negatively swing the EBITDAR margins as the base is very strong at the moment.

- Indigo tries to pass the price increase like it did in 2019 but failed and it fails again due to competition not complying with it. This seems less likely

Excessive competition comes back in the picture and starts undercutting each other like it did in 2017-2019 period.

This has lesser probability to happen again since competition is losing money and Indigo has 60%+ market share, but cannot be ruled out. Earlier also competition was losing money but despite that it did undercut

Summary

Thesis

- Economy is doing very good and GDP growth rates are coming above average which means air travel demand is stronger than before.

- Indigo is trying to increase international ASKs and business class travel which will improve yields

- Secular ASK growth story with new aircrafts coming every few days. ASKs should grow around mid-teens without much interruption.

Anti Thesis

- The base is very strong and there could be quarters where ASK growth is 15% but there is marginal yield compression leading to subdued revenue growth.

- The average ticket prices/yields on existing routes don’t seem to have much headroom to expand but even if they remain stable that would be encouraging.

- Crude price inflation or USD/INR depreciation is the biggest anti thesis pointer as that would swing the margins downward strongly especially on such a high base.

- Increase in competitive intensity as seen during 2017-2019 era.

- Pricing regulations by government

Key things to track here

- ASK growth of Indigo and industry (measures supply)

- Yields/Average ticket prices (measures demand & competitive intensity). ASK X Yield is topline and bottomline gets decided by factors such as fuel costs, maintainence costs, rentals and other opex

- Crude price shocks

- Currency movements

- Significant maintainence costs being incurred

| Subscribe To Our Free Newsletter |