Hi,

As we all know KSL has acquired Kamineini’s plant for Rs. ~450 cr which has capacity of 350,000 MT.

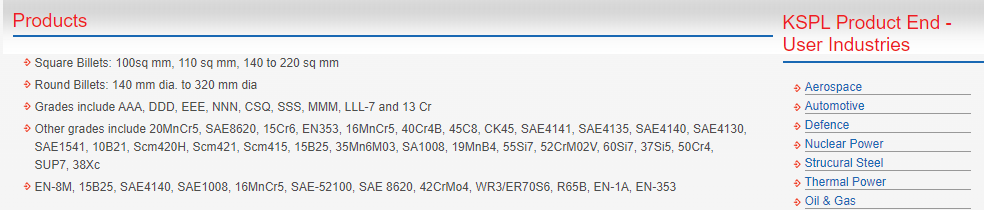

On Kamineine’s website it is mentioned that they manufacture Billets:

If my understanding is correct, Steel Billets have realization of ~Rs. 40-45,000/ MT, right or am I wrong?

KSL’s current realization are almost Rs. 75-77,000/MT

| (All Rs. In cr) | FY22 | FY23 | FY24 |

|---|---|---|---|

| Total Revenue (Rs. cr) | 1,706 | 1,899 | 1,959 |

| Total Volume | 2,28,578 | 2,45,364 | 2,47,500 |

| CU% | 91.4% | 98.1% | 99% |

| Blended realization (Rs/MT) | 74,635 | 77,395 | 79,152 |

| RM Cost (Rs. cr) | 967.3 | 1185.0 | 1120.8 |

| RM Cost per tonne (Rs/MT) | 42,317 | 48,294 | 45,285 |

| Gross Profit per tonne (RS/MT) | 32,319 | 29,101 | 33,867 |

| EBITDA (Rs. cr) | 338.6 | 245.7 | 371.0 |

| EBITDA per tonne | 14,812 | 10,012 | 14,988 |

I have 3 questions from this:

- Will KSL sell commodity Billets from Kamineini’s plant or Carbon/Alloy it after processing?

- What could be the realization and EBITDA/MT of Kamineni’s products?

- Is Kaminein’s entire capacity available for production or actual utlization would be lower because the plant is old?

Would be great if anyone tracking thye Co. closely could enlighten on this. Thanks

| Subscribe To Our Free Newsletter |