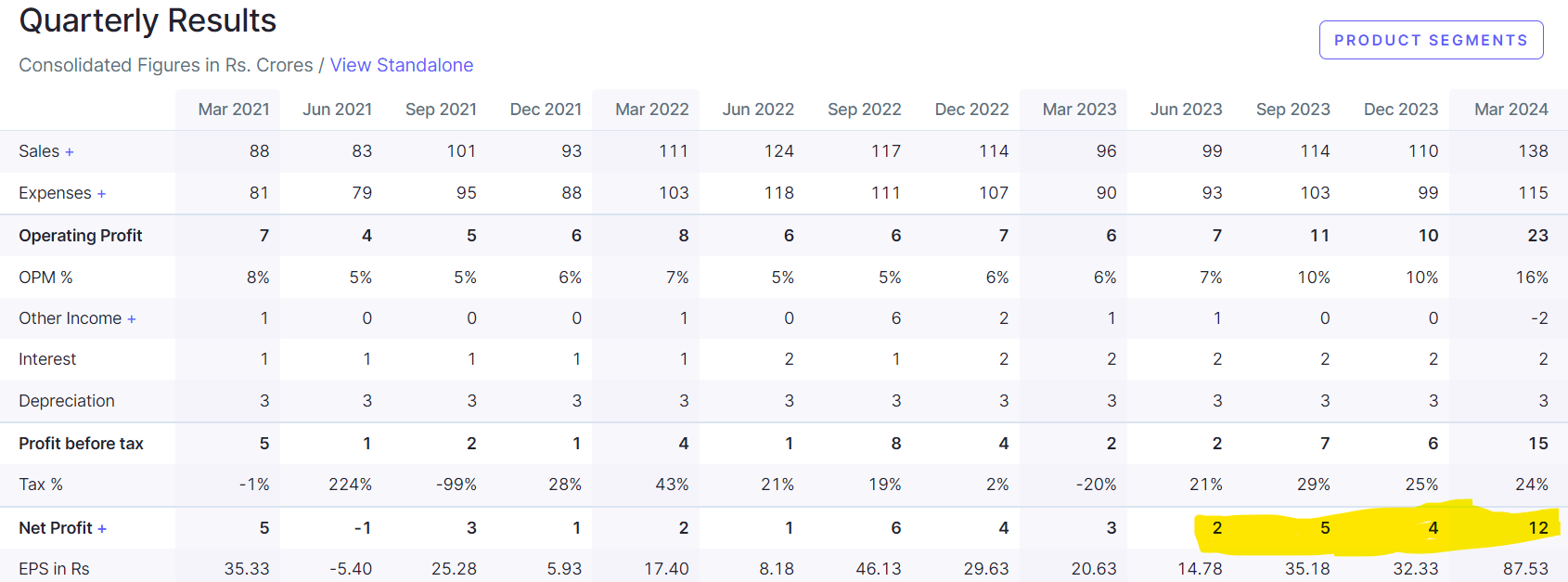

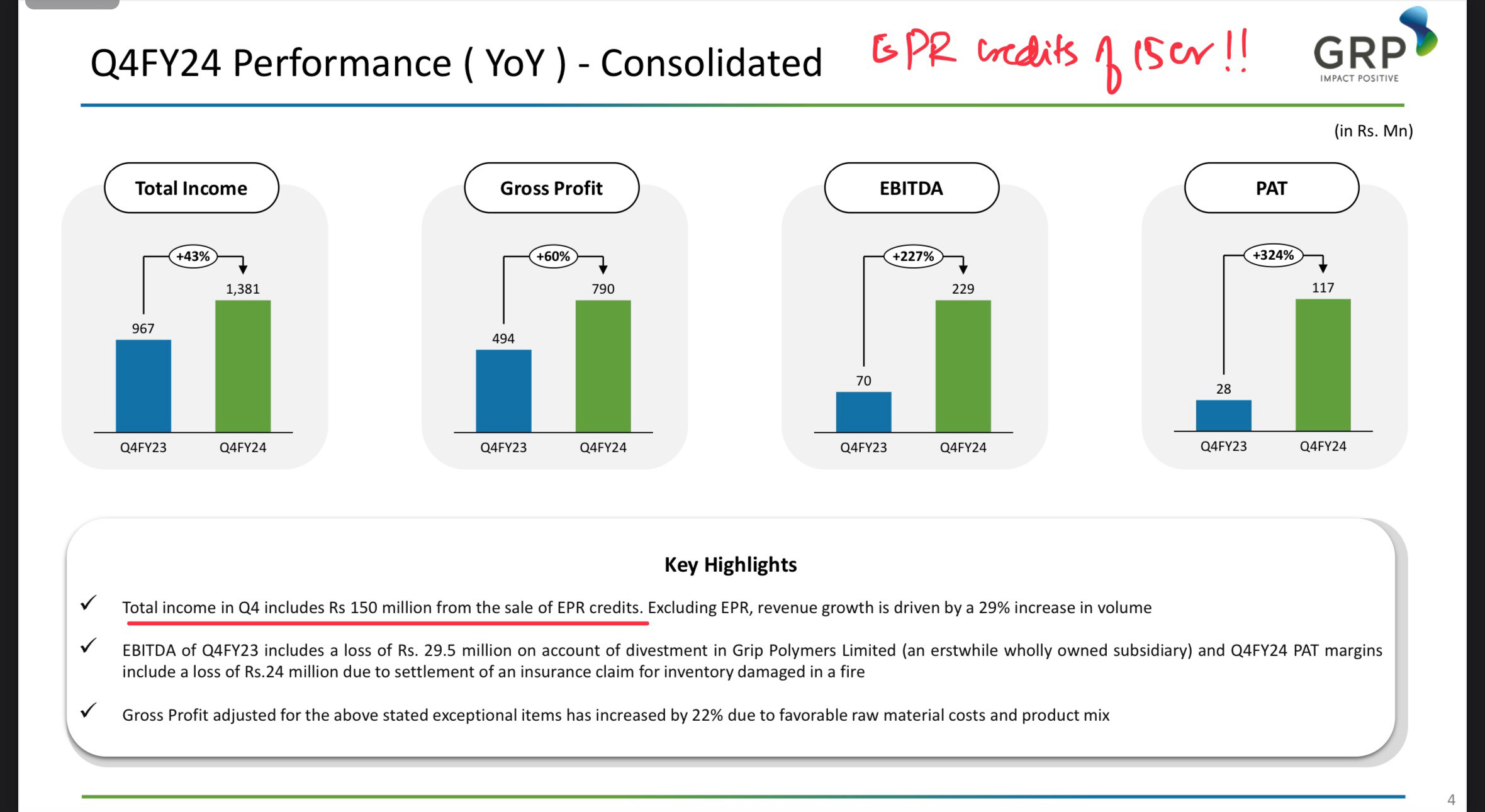

This stock delivered 3x of their usual PAT avg in Q4 . This is what piqued my interest.

.

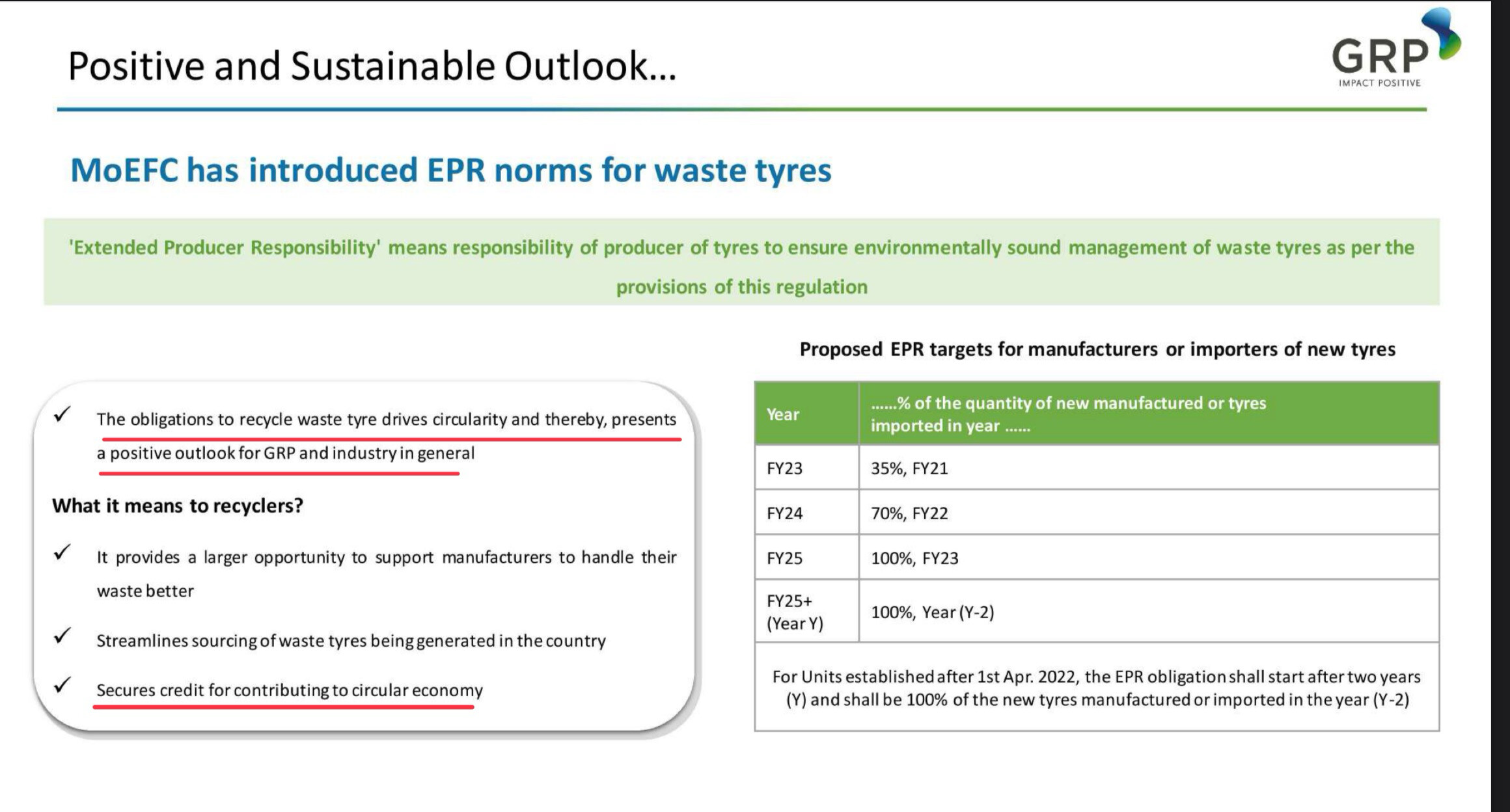

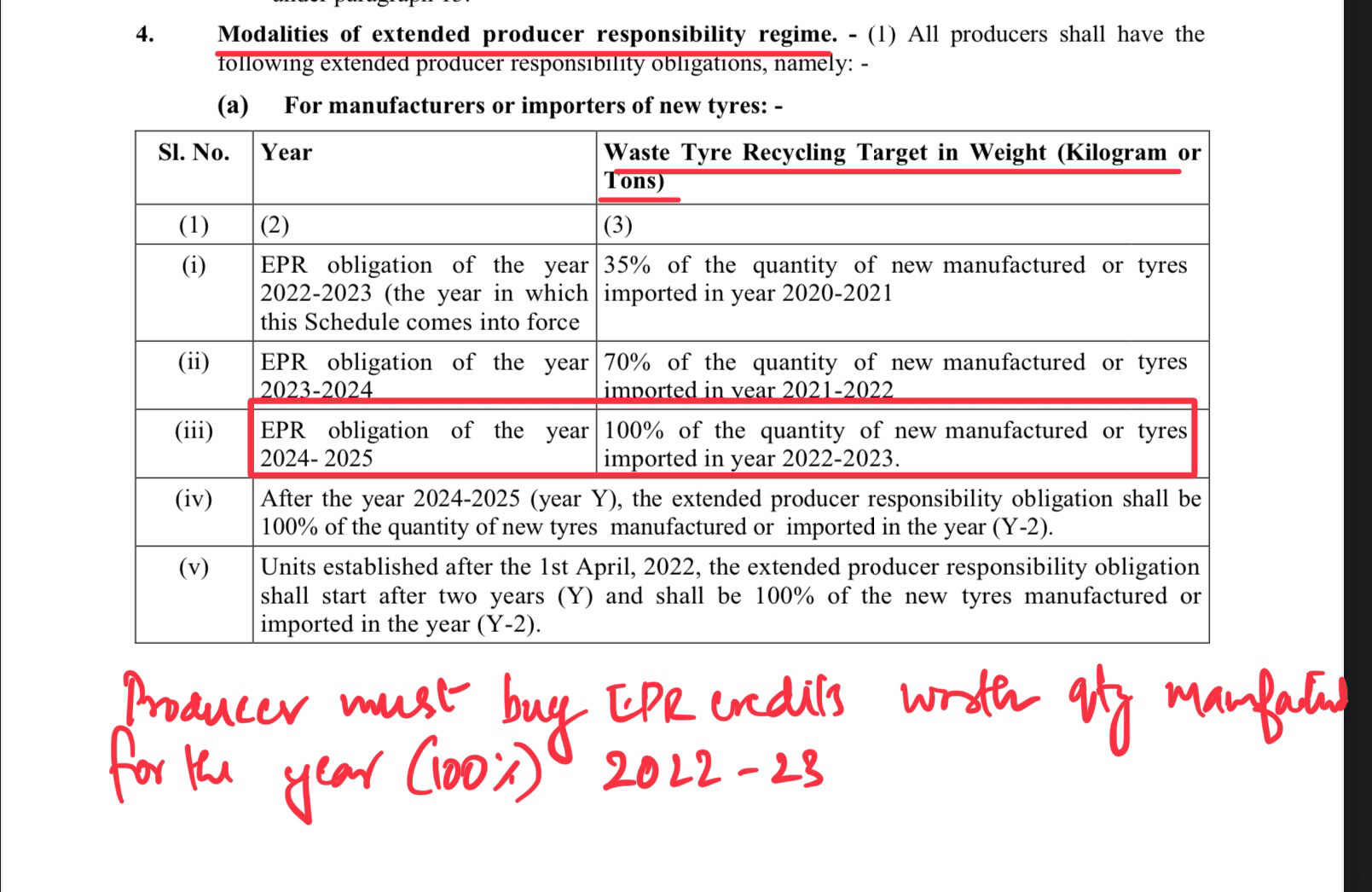

Part of the reason for this bumper performance is due to EPR (Extended Producer Responsibility). I believe this has the potential to change the fortunes of this once loved now forgotten company.

Back of the Envelope Calculation on the EPR credits for GRP:

Current Capacity: 72000 MT

Capacity Utilization : 85%

Production : 60,000 MT

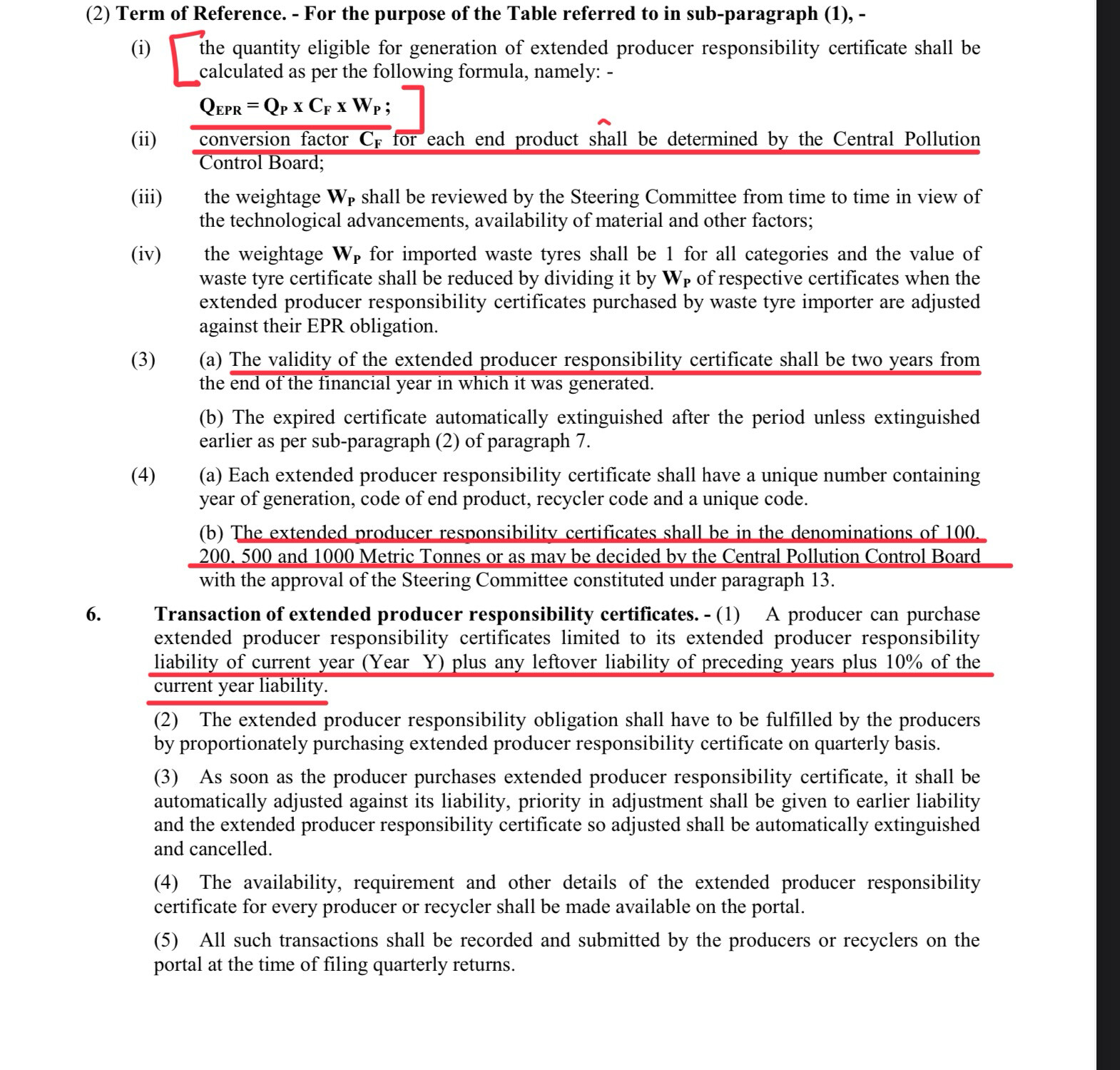

Q(EPR) = Q(P)x C(P) x W(P) = 60000x .78x 1.3 ~ 60000 certificates/ 600 certificates of 100 MT denomination.

In Q4 FY24 GRP has realised 15 Cr from EPR credits (As per management only partial credits realised for FY 22-23 ).

Assuming 60% of the credits are realised for FY 23 we can arrive at approx Rs 4000/MT as addnl realisation due to EPR credit .

The beauty of this is that this amount directly flows into the the EBITDA and boosting the margins as evident from Q4 .

P.S : Realisation for EPR credit is negotiated one on one with the tyre manufactures and this value is bound to vary depending on the demand and supply. However since GRP has several years long relationship with major tyre manufactures they have a natural advantage.

Brief Note on the company :

Concall Notes :

-

EPR for tyres started after 3 years of extensive work including the govt. /CPCB/ Tyre brands etc.

-

Partially realised EPR credits for FY 22-23 . Company has generated credits in CPCB portal for FY 22-23, 23-24 and 24-25 .

-

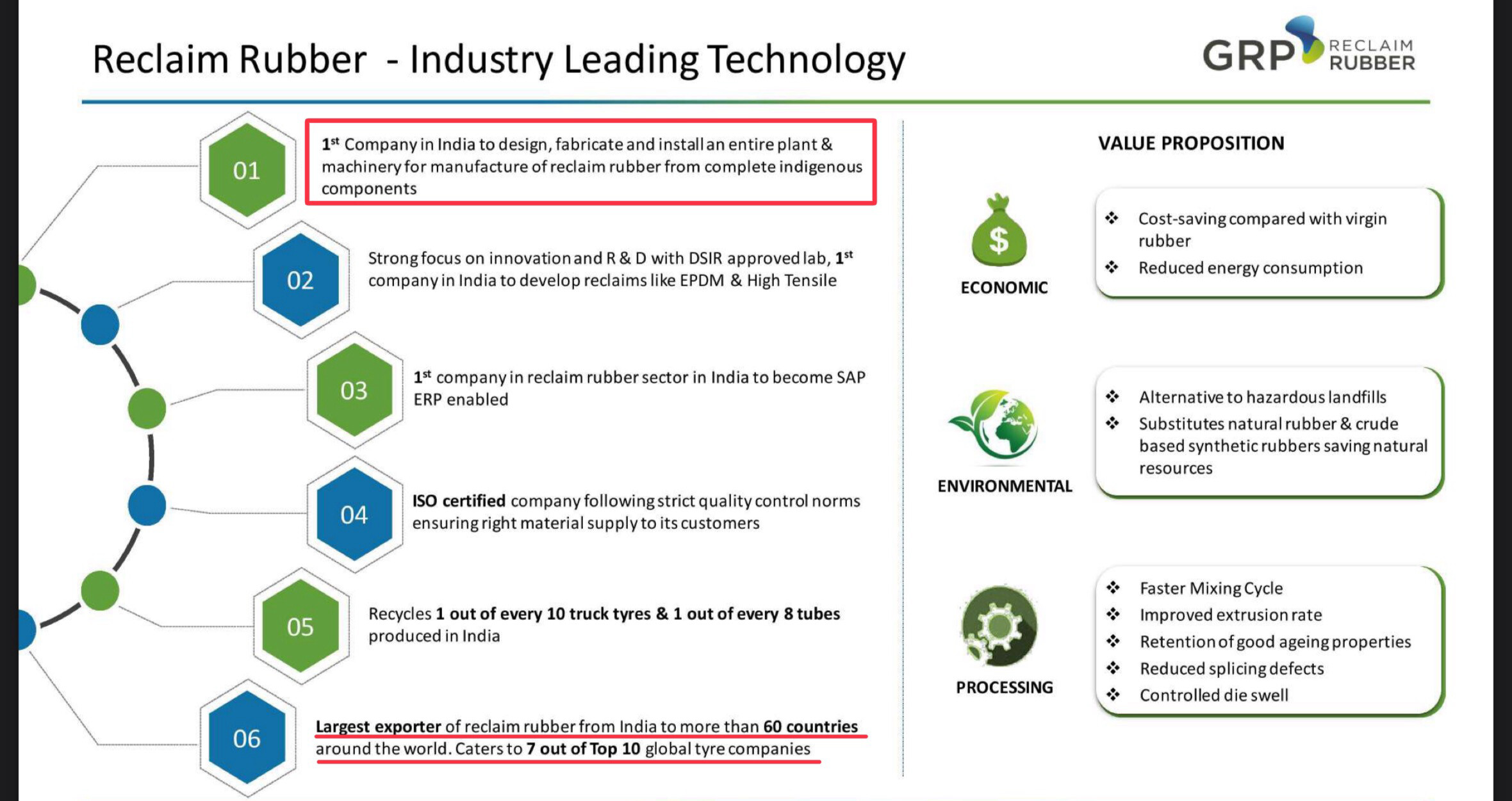

Global brand owners are also focused on the sustainability initiatives of the recyclers. GRP is the first Indian company to be certified for ISCC- ” International Sustainability and Carbon certification “

-

100% subsidiary launched for repurpose Polyolefins business . Applications in paint and Lubricant sector.

-

Successful approval of Engineering plastics business by a European major , paving the way for entry into major auto OEMs.

-

Successfully commissioned new technology for manufacturing reclaimed rubber.

-

Additional land acquired in Sholapur for crumb rubber plant and venture into down stream recycling.

-

EPR regulations in plastics is getting delayed for implementation , expected in current FY.

-

New range of products in engineering plastics business from ocean plastics. Eg : Fish net waste.

Conclusion:

GRP is positioning itself not as a tyre recycler but as the most important cog in the circular economy .Their entire business is in the ESG domain. With the current tailwinds on environment, recycling etc and with introduction of EPR looks like good times are ahead.

Disc: Invested after Q4 results.

| Subscribe To Our Free Newsletter |