Plant Visit Notes

Date 23Jun

Biddadi Plant 11: Interaction with the plant head

-

General Info:

a. Plant head is an ex-Bosch employee who moved to Sansera in 2019-20

b. Plant 11 is focused on automotive parts doing forging, machining of steel parts and for Aluminium parts it does the forging/casting, machining and anodizing

c. Currently the plant contributes to 500 cr of revenues, and is spread over 15 acres of land; there is construction going on which will max out the capacity of the plant; post expansion this plant can support 1000 cr of revenues (mgmt in transcripts have mentioned 400-420 going to 800-850 post expansion) -

Clients serviced through this plant:

a. BMW for Aluminium parts (80% of Al revenue is through BMW; overall Al is 20% of revenues, currently manufacturing 42 parts for BMW, and this is expected to increase to 143 parts by Jun’25 [not sure if this part count increase is BMW only or overall]), Daimler (for both India + Exports), Cummins, Stellantis, Polaris (for ATVs), Bajaj + Triumph (currently through T2 but direct relations also starting)

b. EV clients: Ola, TVS, Bajaj Chetak, HMSI (suspension parts for Activa EV), Ather (side park stand)

c. Recently started for Jaguar EV (first car part known as end-cap being manufactured), business has just started; peak revenues to come from FY26

d. Overall Sansera Level:

i. Korean Clients: Currently the company doesn’t services any korean clients, however their facilities have been inspected and audited by Hyundai (seems Hyundai does this on behalf of Kia as well); but no movement on orders as of now

ii. Mahindra also in talks/coming to Sansera

iii. Ford initial product for testing to be delivered in Oct’25; Go-live from Aug 26 -

Raw Materials:

a. Inventory maintained for about 45 days in the Plant; they also have a warehouse in Germany where another 30 days of inventory is maintained

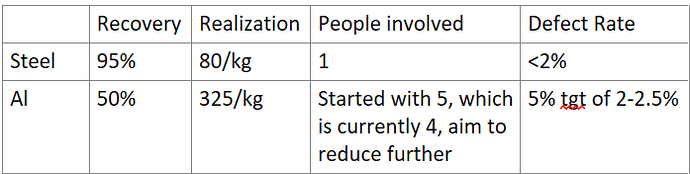

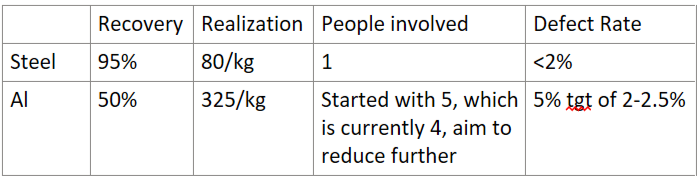

b. Steel vs Aluminium

-

Defect rate of Al is higher due to softness of the product, parts being more aesthetic in nature; manufacturing defect also arises due to variation of temperature in the furnance, company has learnt about it over a period of time and is trying to control these variations

-

Current Infra:

a. Products: Steel forging and Al casting

b. To manufacture these products, the company uses tonne presses (e.g. 4,000 Ton Ajax Forging Press, this is not Sansera presses but mentioned for understanding) which compresses the steel/aluminum products into the desired shapes

c. These presses are procured from China (Shang De named vendor), in total 4 presses in operations -

Expansion:

a. They are in the process of procuring three more presses 1600T, 2500T, 4000T; all are expected to be delivered in the next 6 months

b. Post getting these presses esp 4000T, Sansera can start producing auto comp (body internal + external) for 4Ws and heavier vehicles

c. Currently for Cummins [non-auto] they procure the forged connecting rods from CIE and then do the machining work; once the 4K Tonne press comes in, they would be able to manufacture these parts in house; currently they manufacture one connecting rod, once the 4K press comes in, they can manufacture 4 more new models; Cummins is a difficult client, they want the forging to be done in-house

d. Currently they manufacture 1.5L parts, aim to increase it to 4.5 lakhs within 2-3 years

e. Company is in the process of finalizing land deal for 50 acres -

Competition:

a. For Al parts → Bill Forge (acq. by CIE) in Faridabad is the only other competition as Sansera is doing Aesthetic parts where the quality requirements of the customer is very high, there is limited competition

b. For Steel parts → Amtec, Amul, Fortune; one of the players shut down among the three (most prob Amtek Auto) which allowed Sansera to make an entry into Tata Motors where its ramping up the business now -

Aluminium Parts:

a. Area where Sansera differentiates itself is that it provides all the client requirements under one roof

b. Requirements means → Solution Treatment, Heat Treatment, Casting, Anodizing, Painting

c. In-house Anodizing is critical esp for aesthetic parts; as the final product quality gets discovered post anodising; in 2022 when the company started Al products, they were facing 25% rejection rates and the company was using a vendor from Pune for anodizing; they subsequently got the competency in-house and has gotten the overall reject rates to 5% (tgt is 2-2.5%) -

Overall Sansera related points:

a. Sansera’s differentiators are: Traceability of product raw materials, Automation, Process Knowledge, Speed to Design, Vertically integrated manufacturing

b. Post IPO company has gotten into place lot of new things to drive scalability, like New Product development department, central procurements, moving from process engineering to CoE for Tech manufacturing, structure financial approval/planning

c. Ability to design in-house machines which costs 50Lakhs vs 3-4 cr if bought from outside; however these machines which are manufactured in-house are special purpose machines which can be used for mulitple things allowing fungibility in the manufacturing purposes; Sansera has a team of 60 engineers who only focus on the manufacturing of these SPMs

Management meeting: CEO, Founders (MD and Jt. MD), CFO

Discussion focused more on the aerospace and defence capabilities

- Evolution:

a. Aerospace and Defense business was started in 2010, however at that time most of the business coming to India was overflow (capacity o/s) or low value add business

b. Breakthrough for Sansera came with the order of manufacturing power drive housing units for aircrafts (POWER DRIVE UNIT TIPS✈ CARGO #aircraftmechanic #aviation #aircraft #cargo #airplane #PDU #shorts this unit directs the cargo for optimal space utilization)

c. Since then the products offered by Sansera has increased to Actuators for planes, flap tracks, and is now trying to move into higher value added parts in engines and landing gears

d. The main issue in aerospace business is that its takes a long period for the OEs (Boeing, Airbus of the world) to trust a manufacturer upto 10 years; (seems that Sansera has put in those hard yards, and is getting traction from the Oes)

e. One of the reasons for Sansera to enter the aerospace was that a lot of tech of aerospace gradually moves to Automobiles and thus presence in Aero also helps them prepare for the Auto tech - Business:

a. Current customers: Boeing 60% (T1); Airbus 40% (T2/3, direct billing under progress)

b. Revenues comes from MRO + New Planes

c. Expect to grow 40-50% due to lower base effect (one program of Boeing got shifted to FY26)

d. Current new plant can do 350 cr full capacity; current infra can do 250 cr

e. Being export business margins are 6-8% higher

f. 25% EBITDA margins are possible for the business

g. Movement from ICE focus to other businesses:

i. Mgmt saw the transition towards EV, while they didn’t see that there would be an overnight shift to EV, they started diversifying revenues

ii. Started leveraging their precision manufacturing capabilities and more towards safety, higher emission norm

iii. Now they are seeing Hybrid as something that would go-up before eventual EV

i. Wrt machines and Plant:

i. Aerospace machines are Japanese manufactured, they don’t allow manufacturer to use their machines for Defence purposes

ii. Defence machines are German

iii. Limited Sansera manufactured machines (saw one Sansera machine out of 72 CNC machines in the plant)

iv. Defence players don’t like inter-mingling of infra, and therefore the company created dedicated plant for this business (separate segregation of Defence manufacturing in the Aerospace and Defence plant)

j. Defence:

i. Manufacture for HAL helicopter plants

ii. Manufacture canister for Brahmos missiles for L&T

k. MMRFIC:

i. Started by technocrats who worked with DRDO to get product approvals for over 3.5-4 years

ii. The company was looking for investors to help in the scale-up of the business given approval were in place, that’s where Sansera comes in

iii. Of the products that MMRFIC has approval for, two main products discussed: - Gimbal based seeking radar

a.

b. Each of the black text items are individual components which gets approved individually by the DRDO

c. This component goes inside a high-end missile which can stirke a target with an distance of 1m

d. MMRFIC is qualified for 4 components, the DSP is approved for by some other vendor (also this is the way that DRDO functions, no vendor whole approval)

e. There is opportunity for Sansera for being the final integrator, with 4 components coming from MMRFIC and one by the other vendor

f. Currently India imports these items from Belarus and Israel costing 3.5-4.5 cr per unit; with Sansera+MMRFIC the whole thing can be done at 1.3-1.4 cr costing

g. Demand in qty can be 2000 units over 4 years

h. Application is also in bombs (to trigger the fuse for ignition), drones - Surveillance radars

a. Radar for usage of surveillance at border areas where visibilty is a challenge (e.g. Siachen, Indo-China border in winters)

b. These radars are size of a credit card, and can be put on the back pack as well

c. Company expected to get grant of 12 cr

d. Along with defence, the application is also in automobiles which is like ADAS/sensing ahead - AESA: Aircraft deactivate radar beam bomber

a. Can deactivate radar/beams which comes under its area - Expect 20-25 cr revenues from MMRFIC w/o including the grant

iv. Sansera is also pursuing capability developments for semiconductors

Automobiles business:

- Question was on moving up on the sub-system vs component: Currently to OEs like Maruti, Sansera is providing only Connecting Rods; but Maruti is expecting the Auto Ancs to combine Piston and Connecting rods and supply in one shot; given Sansera is focusing on Connecting Rods only, the option is to tie-up with a pistons manufacturer and package and deliver to Maruti; however it’s a tedious + manual process with limited value add, and margins may come down, which is not what Sansera does → need to confirm what Sansera finally decided to do with this

- Scooters (6-8% of revenues):

a. For ICE customers include: HMSI, Suzuki, Yamaha (for Suzuki and Yamaha the component counts have reduced)

b. For EV: Ola, TVS, Ather, Chetak, HMSI (stem comp)

i. Wrt Ola: Not working at desired margins but working at acceptable margins

ii. Ather + HMSI → supply limited components

iii. Components supplied includes: stam comp, suspension base, side stand (which has become complicated forging due to aluminium and light weighting) - Motorcycle

a. EV adoption might be far way down the line, this is driven due to speed and range requirements; as speed and range requirements go-up so does the battery which means far higher light weighting would be required and costs goes up due to higher cost of Al

b. Currently providing Cat A&B (which are customer visible & aesthetic parts) mostly for 400+ CC machines; this is possible only due to higher costs of these vehicles which allows the cost absorption of higher Al - Biddadi plant would max out with 10 presses, and currently they are booked out; this is in spite of not having approached the 4W for Al parts

- When they started they were focused on connecting rods business, but toyota pushed them to do more components as they didn’t like one product only vendor; slowly grew offerings to 22 products; now they supply these 22 parts + 4 shaft products (2 finished and 2 semi-finished) which are EV compliant as well

- Case study of product quality:

a. An OEM wanted 12-14 parts; Sansera won 8-9 parts and remaining to other vendors

b. The OEM had a requirement of 1800 hours xenon testing (which basically means the color on the parts have to remain same over 3-4 years)

c. After 2-3 years the client came back to Sansera to give order for the remaining parts as other vendors were not able to give that performance - On Hyundai and Kia: Facilities are audited and cleared

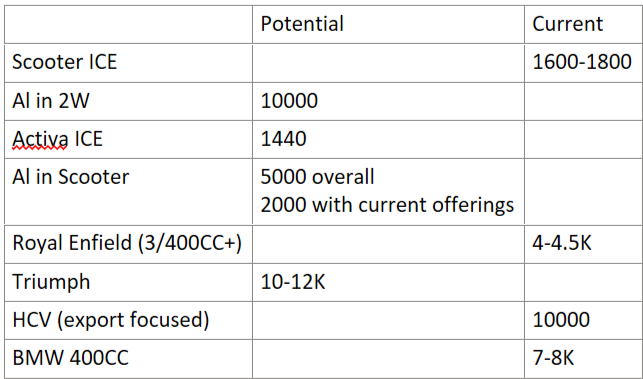

Current Kit Value per vehicle

Financial Metrics/Ratios:

- Capex done in a particular year is for revenues for 1.5-2 years hence; customer gives order only when there is capacity

- Export vs Domestic margins: 6-8% higher

- AR Domestic 40 days; exports 110 days

- Inventory domestic <50 days, exports 160 days

- Tgt exports level: 35-40% in 2-3 years

- Last 2-3 years due to all the logistics issues, OEs are following a supplier managed inventory model

- Machine life is 20-25 years

AEROSPACE AND DEFENCE PLANT:

- Currently manufactures 1550 part counts/SKUs; manufactured 25000 parts

- Part upto 2.2 meter length being manufactured (mostly air plane’s tail cone)

- What OEs want is special project capabilities which basically means coating functionality

- Plant is highly automated:

a. The production of a particular item is pre-programmed by engineers centrally

b. A block of material (say Al/Titanium) is put in the CNC machine

c. Then the CNC machine executes these instructions one after the other

d. There is an attender on the machine (as product manufacturing matures, one person can handle two machines at the same time), person is required to take noting at some defined intervals - Intensity of work with Airbus is increasing as the company becomes a T1 supplier; 4-5 team visits are planned within the next month

- 40 employees are working on the R&D which focuses on how to manufacture the products more efficiently (wrt time, material consumed)

- Current revenue break up Structural components 15%, Actuators 25%, Avionics just started

- Current rejection rate of 0.75%

- Airbus had a european manufacturer for actuators, however due to cost and relative quality issues, Airbus gave Acutators manufacturing to Sansera; for A350 and A320, Sansera is the single source manufacturer

- Defence current utilization is ~30% which in 6-7 months is expected to hit 60%

- Airbus Defence visit planned in July, for becoming a T1 vendor for them

| Subscribe To Our Free Newsletter |