Hello, everyone in this thread seems to be bullish for this cycle of defense sector rally and as we have seen in past overly bullish approach in any sector leads to disasters.

I will try to present my thesis as to why I think the valuations at the moment are stretched and very little to no valuation comfort lies which is contributing to a dangerous euphoria.

Defense Sector Red Flags:

- Indian defense sector is in itself at a nascent stage.

- We come no where close to the defense RnD spend done by countries like US, Russia and China.

- Defense sector in India is highly concentrated and dependent on govt. funding no private players exist which can give competition to big names such as HAL, Mazgaon Doc.

- Sector requires high capex before any additional set of revenue can be turned into profits.

- Intensive RnD lead sector.

- Since dependence on govt spending is key sector demands high growth in GDP to defense expenditure YoY.

- Govt policies have a strong say in spending and procurement of defense equipments, a coalition govt in centre may not be able to continue with the old growth plans although in the current scenario this is unlikely. A strong opposition also might scrutinise the defense deals leading to delays.

We will be looking at listed companies which are directly involved in making of arms, ammunitions, armoured vehicles, aircrafts, ships, frigates, UAVs, night vision devices, missiles, launchers and avionics.

The prominent listed companies along with their p/e and p/bv are: (P): PSU;

- HAL (P) – 46 ; 12xBV

- Mazgaon Dock (P) – 44 ; 14xBV

- Cochin Shipyard (P) – 42 ; 12xBV

- Bharat Electronics (P) – 56 ; 14xBV

- Data Pattern – 93 ; 13xBV

- Paras Defence – 182 ; 13xBV

- Taneja Aerospace – 141 ; 13xBV

- Bharat Dynamics (P) – 96 ; 16xBV

- Krishna Defense – 153 ; 14xBV

- Zen Technologies – 26 ; 5xBV

- DCX Systems – 60 ; 4xBV

- Bharat Forge – 85 ; 11xBV

- Garden Reach Ship Builders – 73 ; 15xBV

On current valuations the

- Avg pe: 84 vs historic avg pe: 32.3

- Avg p/bv – 12xBV vs historic avg p/bv: 4.5xBV

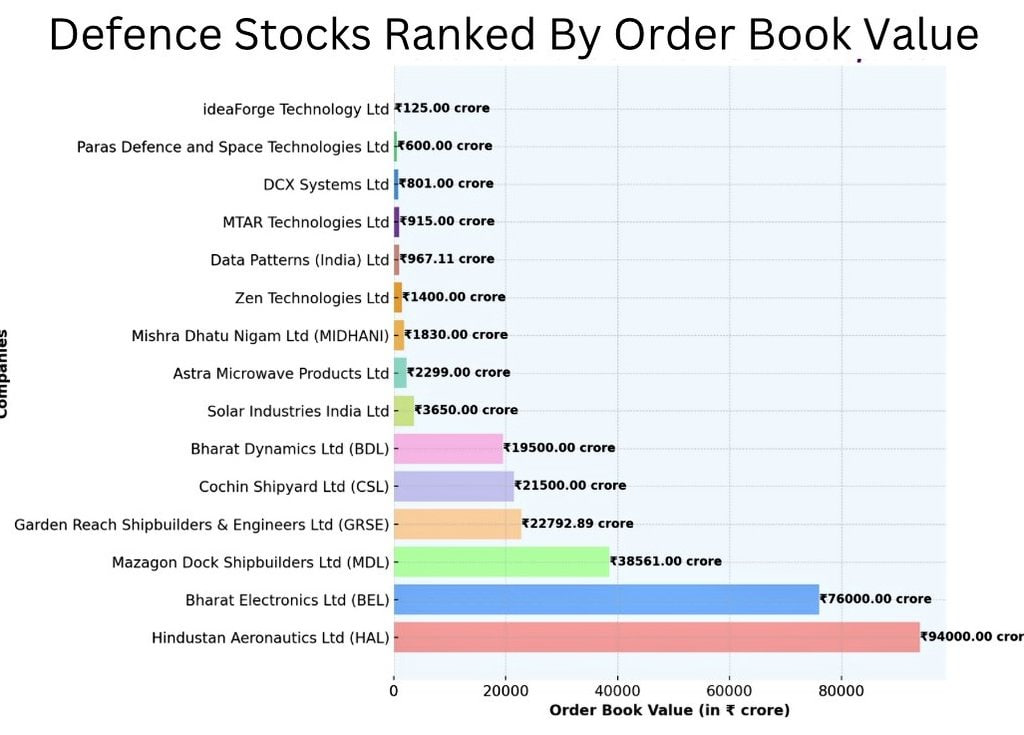

Apart from these very basic valuation metrics the order book scenario of major defense companies are below, these numbers are usually thrown around on the internet to show potential upside in top and bottom line, while this might be true in a bull run investors are often

A lot of these companies especially companies working solely in defence manufacturing are dependent on each other for components and survive through orders given to them by a bigger vendor. This poses a serious problem because if a bigger vendor is late on its payment it will have a tinkering down effect on the smaller players. Mutual fund houses also have recently launched their defense funds which is signalling exuberance in the sector.

The problem with order book led stock rerating is that while a 94,000 cr order book look monstrous from a bird eye view it might not be as attractive when the execution is done over a period of 2-3 years. Order book concentration is also something to be cautious about since a few orders in the pipeline may boasts the majority of the revenue posing a longevity threat.

What is important here is to look if the companies are going to substantially increase their revenue YoY while maintaining their margins, equally important is their profitability. Since the street tends to pay for the actual EPS growth when the froth settles down it would be dangerous to bet on stocks which tend to over estimate their growth in the next 3-5 years time frame.

Assuming all of the order book is executed on time without any operational delay and assuming the payment from govt comes on time and more new orders are procured we seem to be over paying for a lot of what these stocks are worth for.

For eg: Paras defence order book is 600cr at a market cap of 5561cr the mcap/orderbook comes close to 9.

| Subscribe To Our Free Newsletter |