Q4 Fy24 Concall

~ Current Operational Performance:

^ In 2024, revenue from CRO has largely remain flat YoY while CDMO has seen 25% growth.

Business Structure

^ If you’re going to take and transfer some work out of China, the easiest and the most fungible, certainly the quickest, is just the research part of it, so discovery research contracts. Just because of their very nature, they tend to be short-term or annual FTE contracts. Once you move into development, it’s a bit stickier, and of course then product manufacturing, whether it’s API or drug product, is much less agile and not easy to move.

Business Changes

^ Plans to invest around USD60 million in capital expenditures, primarily in research services and development and manufacturing services, half of this is expected in research services, around 40% is planned for the CDMO business, and remaining includes investment in digitization and ESG initiatives.

Guidance

^ We anticipate high single digit to low-double digit growth on a constant currency basis for the year.

^ The effective tax rate is expected to increase to around 23% in the current fiscal year.

Remark

^ Startup biotech funding hit a road bump.

^ For big pharma company, biosecure act will cause slow & steady diversification from China.

^ Demand may come back in H2Fy25.

Goldman Sachs CDMO Report Apr 2024

20% plus growth in CRO in a biotech funding winter appears to be very much optimistic, i expect it to be around 8-12% at max. However, CRO is not as sticky as CDMO and in an “CHINA+1” scenario, this may actually touch 15-20%. Regarding CDMO, it is already growing at 25%+.

ANNUAL REPORT 2024

^ The global CDMO market (comprising small and large molecules) was valued at USD 82 bn in 2023 and is expected to grow at a CAGR of 14% to reach a market size of USD 208 Bn in 2030.

^ Development and Manufacturing Services revenue grew by 26%.

^ All the existing mAbs manufacturing capacity is utilized. The new facilities acquired from Stelis will be available for business in the second half of FY25.

^ In the biologics development laboratories, the focus was on piloting high-yielding cell lines.

^ We anticipate stabilization in demand growth from small- and medium-sized biotechnology clients based in the US from second half of FY25, as the funding environment normalizes.

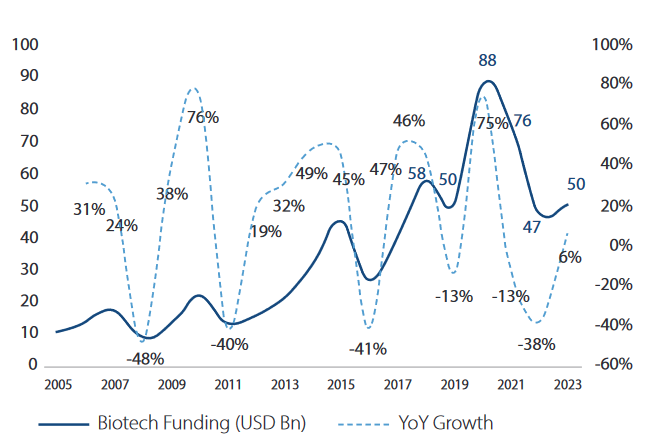

^ Biotechnology funding remains robust, with 2023 levels comparable to pre-pandemic figures from 2019 and exhibiting a long-term CAGR of 6%. While 2023 has been challenging for biotech funding, Jan to March 2024 funding levels were the highest in previous 14 quarters, similar to funding levels in 2021.

^ The global pharmaceutical market for human health is shifting towards large molecule drugs and expected to grow at a 12% CAGR from 2022 to 2026, contrasting with 2% for small molecules. Consequently, demand for biologics manufacturing capacity is rising at a 9% rate, but only 2% will be met by in-house expansions.

^ Commissioning of Automated Central Compound Management Facility, a first-of-its-kind in India. This state-of-the-art facility acts as a repository for all compounds synthesized by Syngene. The CCM can store between half to one Mn compounds in controlled environments.

Present status of funding in CRDMO Src: AR 2024

Funding is back to pre-covid level. Management is expecting it to go upwards from here on.

CREDIT REPORT Nov 2023

^ Over the past 2-3 years, Syngene has undertaken high capex towards commercialisation of the API manufacturing facility in Mangaluru & research centres in Hyderabad.

^ The company has organic capex plans of Rs 500-600 crore annually towards adding laboratory space for future expansion of the R&D business and capability additions across other services.

^ Syngene will remain exposed to risks related to stabilisation and ramp-up in production and services. However, its history of timely project completion provides comfort.

^ Any time or cost overrun in the planned capex will be a key monitorable.

VALUATION

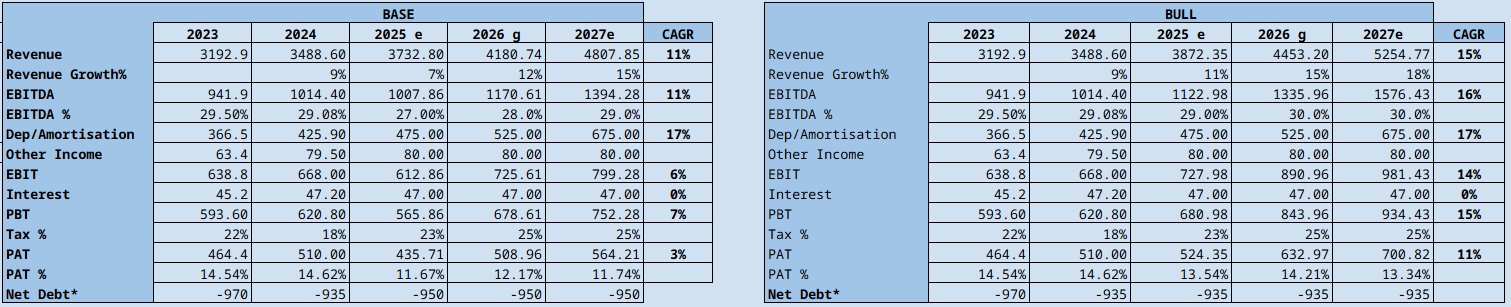

My view on Base & Bull case. For me the company is trading at (Rs 700/-) fair valuation of 3year projected earning in bull case.

Disc: Holding & hopeful on the future.

| Subscribe To Our Free Newsletter |