A few thoughts

-

My gut likes the promoters

- the company was fully bootstrapped, the promoters started fresh out of college and funded 2L each

- Profitable since inception

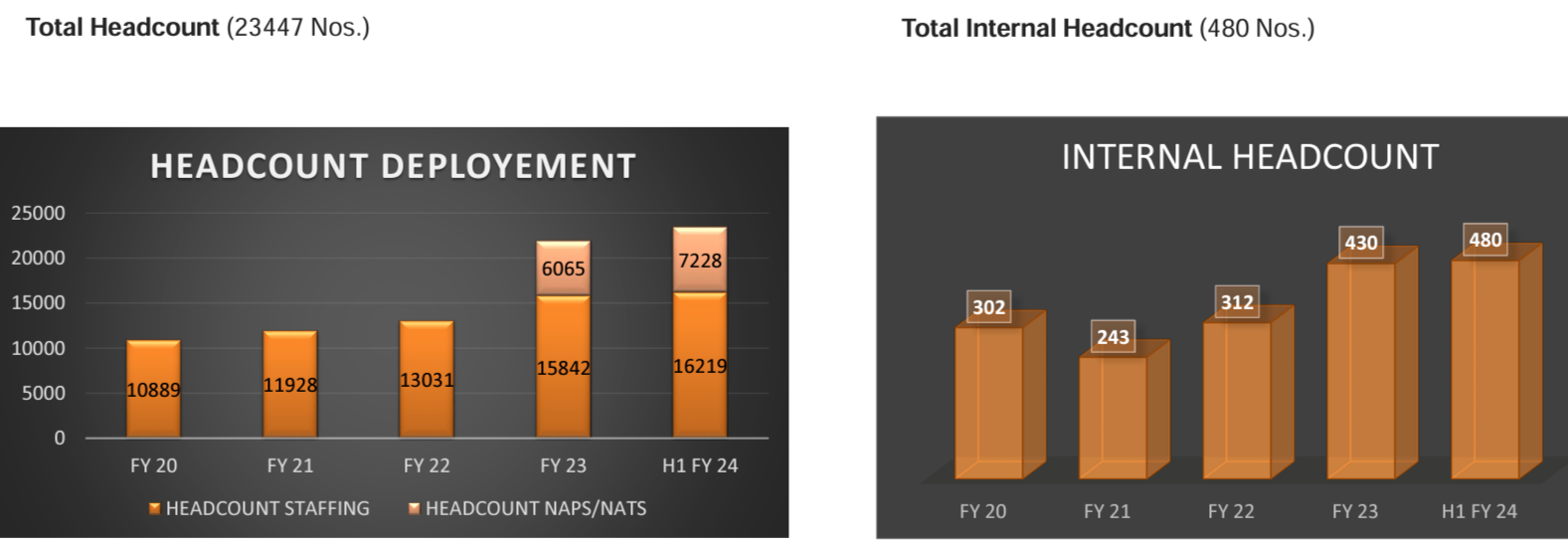

- just look at the scaleup, within 8yrs of incorporation did 200cr in 2019, and now doing 600cr+, in such a commoditised industry thats a significant achievement i believe

-

Few pieces from the concall

- ‘‘Chanishji, we are holding an earnings call, facing the music and giving you all the justifications. Regarding the stock price, the drop that you said that sir, our significant wealth is in this organization only for both of us, and we are we are collectively holding over 70%. So, trust me, it bothers me a lot more compared to what it would bother you. But then we are confident on the business. And we are here –we are in it for the long run.’’

- there were a lot of questions on stock price and biz performance, above replies seem prompt and genuine

- A question on ipo funds- ‘‘we were very clear that we don’t want to – instead of reporting it, we voluntarily chose a monitoring agency. So that we can put in better corporate governance and build the right amount of trust.’’

- ‘‘Chanishji, we are holding an earnings call, facing the music and giving you all the justifications. Regarding the stock price, the drop that you said that sir, our significant wealth is in this organization only for both of us, and we are we are collectively holding over 70%. So, trust me, it bothers me a lot more compared to what it would bother you. But then we are confident on the business. And we are here –we are in it for the long run.’’

-

One needs to understand the fund flow in this industry, without working capital one would need significant debt, look at the other players in the industry

- Considering this is a new guy with a lot of wc funds acquired through the ipo, it shouldnt face any debt issues in the medium term, causing the ebitda to flow down directly, adding to it the tax benefit

-

Global hr biz has a huge potential as and when the foreign markets turn

- The US staffing business was started in the year 2020. It has grown over 100% last year in FY23. Such growth in such a short time is commendable however small the actual amount be, and now again they have started seeing mandates coming in proofing their demand.

-

Cannot find the names of customer, and not that it matters as much considering the quantum they have, but back around 2013-16, they have been appreciated from very senior KMPs of companies, primarily MNC pharma names

- This is especially important because the year of their incorporation was 2012, within such a short period penetrating into such MNC customers, especially serving niche and quality driven requirements of pharma sector, says something atleast

-

Electronics business is soon to be sold out, this would thus not dilute the margins going ahead

Nothing is fully clean/great always

-

There are some doubts on few datapoints, looking closely they have lost of per employee realization, basically they have been needing a higher amt of emps to do the same rev

-

Also the NATS/NAPS scheme is a bucket with a hole, since after their cycles the employees mostly will not join in with spectrum

-

Previously the CFO to EBITDA conversion was high, but since the last 2-3 years it has been dropping, even negative

- The receivables have spiked up a bit, which can somewhat be expected due to the industry downturn

- in this industry i have seen debtors cycle inc and then slowly but surely damaging the bs and thus the bottomline, so this needs to be watched very closely.

-

Peers are not seeing any revival in demand in the short term

Conclusion

-

even commodity biz at certain valuations become desirable, everything is based on demand and supply, and mind it in comparison to peers it is vastly undervalued, also now that the low value trading biz is to be cut out, the coal should burn brighter (purposely chose the coal analogy, because it is nowhere near a dimaond)

-

They have been doing a lot of hiring, across mid and senior levels. Previously they werent able to attract talent due to their size, but now post the IPO the company has seen recognition. Also because of the industry downturn the peers are somewhat reducing their force and with the rest they are trying to control the salaries (reduced salaries), during this scenario Spectrum is trying to be the outlier and getting in as much talent as they can, which i find extremely interesting

- Sales team is up from 11 to 23- new sales head for RPO and a team of 10 under him were just brought in, last yr it was only 3

- Operating leverage potential is significant, keeping in mind the sheer quantum and the quality of hires

-

-

There are too many new hires from all MNC competitors, like- Adecco, Quess corp, Terrier security, Teamlease, Randstad, IBM, several other names

- There are many names, which can be individually looked for on linkedin

-

the recruitment and the professional staffing or the IT staffing businesses are highly dependent on the internal manpower that they have. These are higher margins segments, and like i shared above as soon as the industry turns, there should be significant opt lvg

this industry has never been valued to its potential considering the commoditised structure ensuring there to be no entry barrier. No point in being delusional of there being any moat or structure in this industry. Hence no one in this industry is ever valued highly or even decently, few players are even languishing in the mud.

-

Although I find it hard to understand such undervaluation considering the industry’s simplicity in terms of factors to be tracked, cash flows, such roce, simple cycles where once the cycle turns the earnings explode (mann, this is what happened post covid and hence the ipo post growth)

-

I feel the margins have bottomed more or less, and if not today then tomorrow the demand will come back, and like indicated by the promoter whenever cycle turns it turns for the extreme bull case.

-

It should be a simple play on dirt cheap valuations and earnings growth, dont expect significant rerating

- I got in here when it valued the lowest among the whole industry (still is, but here the margin of safety reduced a bit for me), almost as if the business wouldnt survive. I wouldnt add much until i start seeing some earnings turnaround

- Already margins have slightly started increasing, doesnt mean cycle has turned ofcourse

- I got in here when it valued the lowest among the whole industry (still is, but here the margin of safety reduced a bit for me), almost as if the business wouldnt survive. I wouldnt add much until i start seeing some earnings turnaround

-

Also keep in mind other players with worse economics were trading higher

Have created a small position at lower levels, hence biased

| Subscribe To Our Free Newsletter |