Few observations that are remarkable for Dharmaj.

- Have clocked 35% CAGR revenue growth in last 5 years (though from a lower base). Remarkable that they have been able to achieve 25% growth in FY24 despite a challenging environment where most of the AgChem players were struggling on volume/margin front.

- Significant 9x capacity increase underway, major part of that being covered by IPO proceeds (reduced impact of negative leverage in the initial years).

- Capex is focused on Pyrathroids, which is 2nd highest type of AgChem globally. 2 levels of backward integration (Technical and intermediates) will help them be cost competitive to gain market share.

Pyrathroids (Global perspective):

- Pyrethroids were first developed in the 1950s. Are synthetic chemical compounds that are procured from chrysanthemum cinerariaefolium flowers. Pyrethroids are cost-effective alternatives & less toxic compound as compared to conventionally used insecticides. They are also replacing traditionally used or ganophosphates (majorly used as insecticides).

- Global Pyrathroid market is estimated to be ~2 Bn USD.

- The consumption is concentrated in developing markets like Asia, LatAm and Africa while developed markets like the USA, Canada and the EU have been witnessing a declining trend owing to the newer chemistries and local regulations imposed for restricted usage. (could be a potential threat if the developing markets adopt to the restricted usages guidelines)

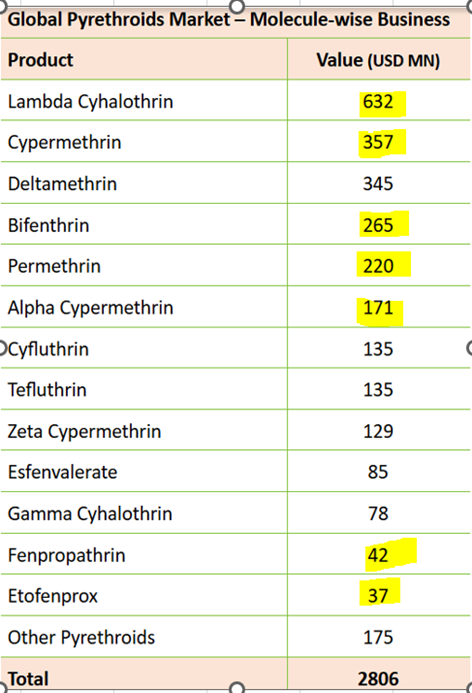

- Among the Pyrethroids, Lambda Cyhalothrin, Cypermethrin, Permethrin, Alpha Cypermethrin, Bifenthrin and Deltamethrin contribute to about 70% of the total Pyrethroid business generating a revenue of USD 1990 MN.

- Global pyrethroid market break up by key molecules. (Highlighted in yellow are the molecules which Dharmaj intends to produce. Good news is that production has already commissioned for top 5-6 molecules starting Q4’FY24. !!!

Pyrathroid (India landscape)

-

India is the the biggest manufacturer of pyrethroids. In fact supplying intermediates to China.

-

On demand size, China accounts for more than 50% of global demand for pyrethroids. China used to manufacture pyrethroids after importing intermediates from India. However, China’s pursuit of the ‘Blue Sky’ initiative to realize green GDP lead to the closure of several chemical plants. This in turn resulted in higher volumes of pyrethroids being exported out of India.

-

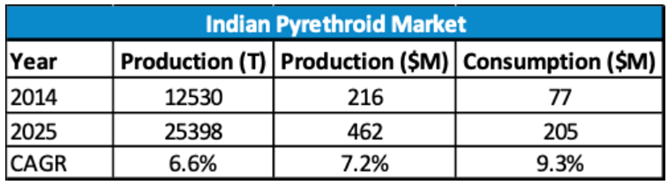

The pyrethroid market in India is expected to grow ~10% CAGR. The key driving factor will be regulatory outlook, China factor, wide spectrum crop application and the substitution of organophosphorus compounds.

-

In 2019, Heranba Industries Limited dominated the India pyrethroids market, accounting for a share of 19.5% of the total Indian pyrethroids production values. Heranba Industries was followed by Tagros Chemicals India (14.8%), Hemani Industries (9.9%), Dhanuka Agritech (8.7%), Insecticides (India) (7.9%), Syngenta India (6.2%), Sumitomo Chemical India (5.8%), UPL (4.2%), Bayer CropScience (3.9%), Rallis India (3.6%), Excel Crop Care (3.4%) and Others (12.1%).

-

One of the key reason for Heranbas pole position in India pyraethroids market is backward integration in CMAC (Cypermethric Acid Chloride). The EOU facility has made Heranba one of the largest manufacturers of CMAC in India, with new production capacity of ~3000 metric tons per year.

-

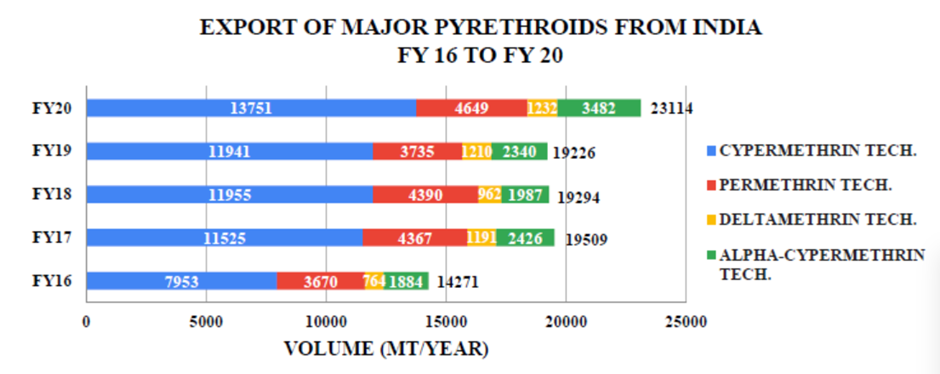

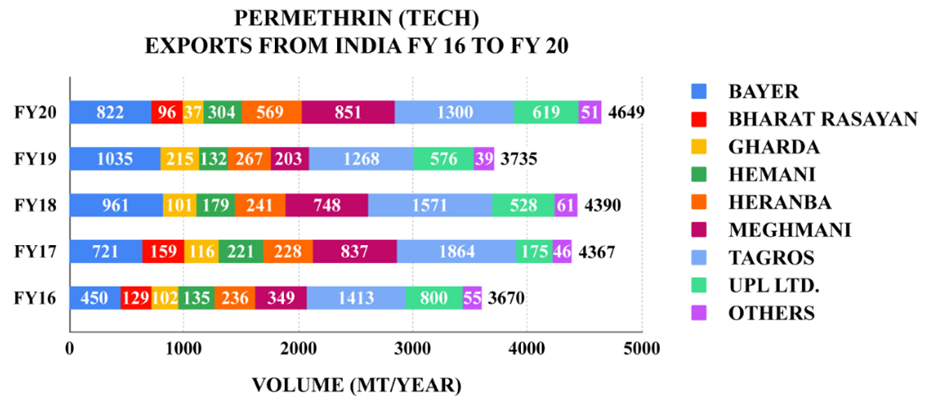

Export contribution by each of the major pyrathroides: (overall and each of the molecules almost doubling in 5 year window between (FY16-20).

-

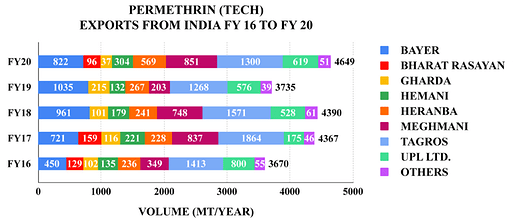

Of all major Pyrethroids produced in the country, Permethrin has a special significance. India is the only manufacturer of Permethrin (Tech.) in the world catering to global Permethrin consumption under all Crop and Non-Crop segments.

-

Hemani and Heranba has cornered max market share vacated by Gharda and Bharat Rasayan.

-

Another significant molecule is Transfluthrin, India is the leading producer of Transfluthrin tech. with over 30% market share in the global Transfluthrin tech. business.

Dharmaj Crop Guard:

- Current formulation plant (Ahmedabad) had gone through 2x+ capacity augmentation to 25,500 MT/year between 2022-24 . Running at 51% capacity utilization in FY24. So, significant headroom to ramp-up formulation side of the business. In fact, is well positioned to drive a much better growth aided by backward integration.

- Recent capex of ~275 Crs for greenfield capex at Saykha. ~100 Crs each from IPO proceed and Project finance, rest met by internal accruals.

- Saykah plant has capacity of 8,000 MT Technical & Intermediates Capacity. Initial plan was for

- 2,500 TPA dedicated MPBD capacity

- 2,500 TPA dedicated CMAC capacity

- 3,000 TPA multi -purpose technical capacity.

- However, going by Q4 presentation and concall hints, seems that they have converted MPBD capacity to multi-purpose.

- 60-70% captive consumption for intermediates • 20 -25% captive consumption for technicals

- Potential ~3X Fixed Asset Turns at Optimum Capacity Utilization & Product -Mix

Somehow, I find striking similarities in the glidepath between Dharmaj and Heranba – be it product profile, break up of revenue across B2b and B2C, domestic vs export, backward integration etc. Hopefully, similarities ends there. (you know what does that mean😉).

Setting up CMAC (Cypermethric Acid Chloride) capacity of 2500 MT/year against the biggest Pyrethroid manufacture Heranba’s backward integrated CMAC capacity of 3000 MT/year is something noteworthy.

Disc: Initated a small position in last 30 days.

Thanks,

Tarun

| Subscribe To Our Free Newsletter |