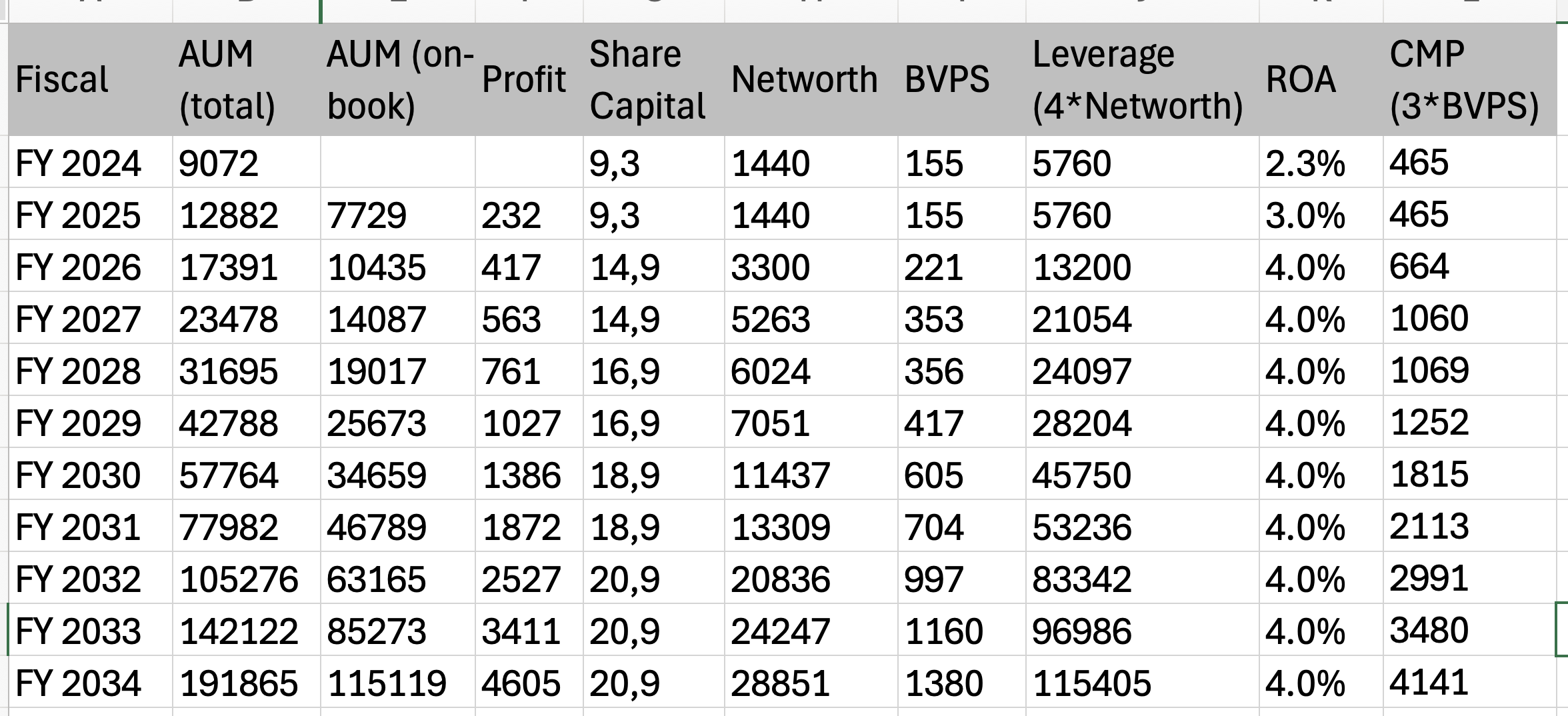

Assumption:

AUM growth of 30% continuously for the next 10years. IMHO it is doable, the TAM is huge, if management has a good control over the ALM, this rate of growth shouldn’t be a problem.

ROA on continuous basis = 4%

Co-lending percentage = 50%

Fund raising in 2028, 2030 and in 2032 by QIP of 2cr shares in each fund raise.

Note:

- Not considering any AUM and PAT addition from Myshubhlife acquisition and any other potential future acquisitions.

- ROA of 4% is on the lower side, it could be higher going forward basis controlled credit cost.

- Valuation of 3BVPS is also on the lower side. It could easily trade at 4BVPS if market wants to give the premium valuation.

Note2: This is a very naive and superfluous analysis with several assumptions, however I sill think Ugro capital has very scalable business model and market at some point in time reward it.

Invested and biased.

| Subscribe To Our Free Newsletter |