Workiva (a much bigger competitor) released their Q1 earnings sometime ago:

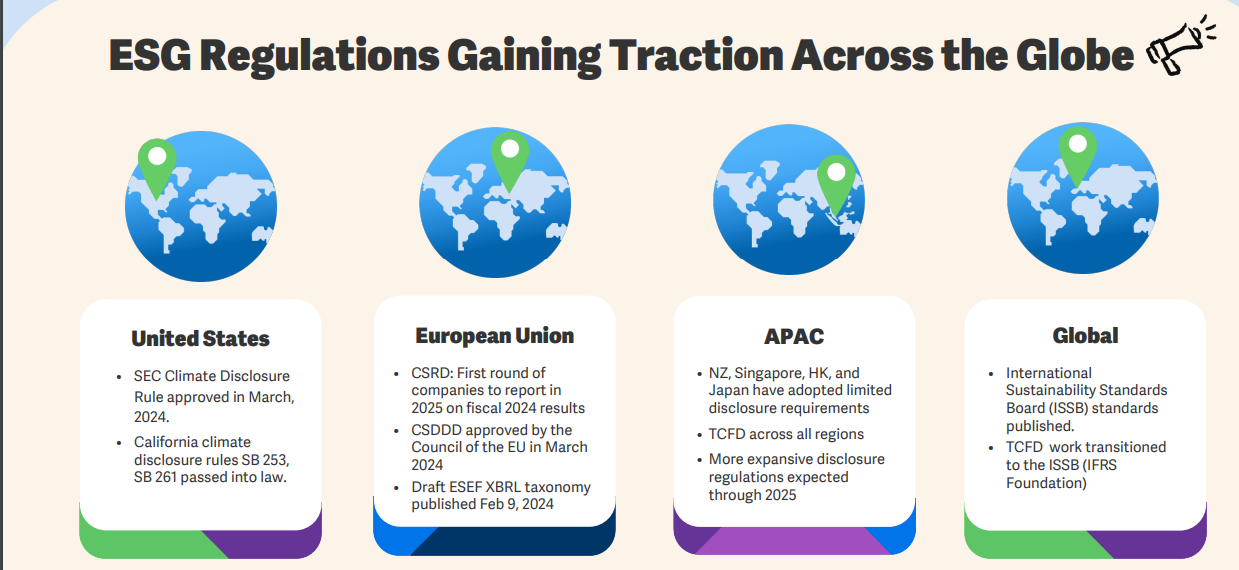

- Regulations across the globe

Note: They don’t mention that the SEC climate disclosure rules are currently stuck in legal battle and hence are on stay

-

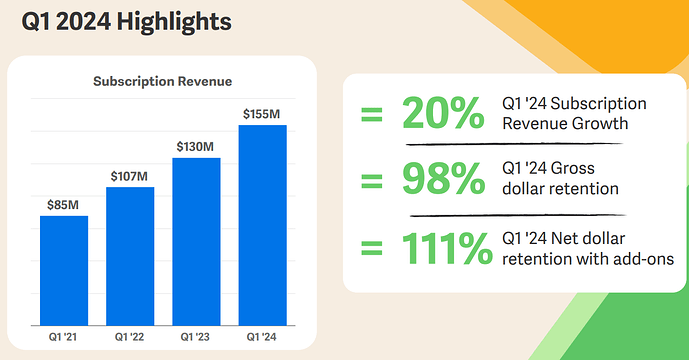

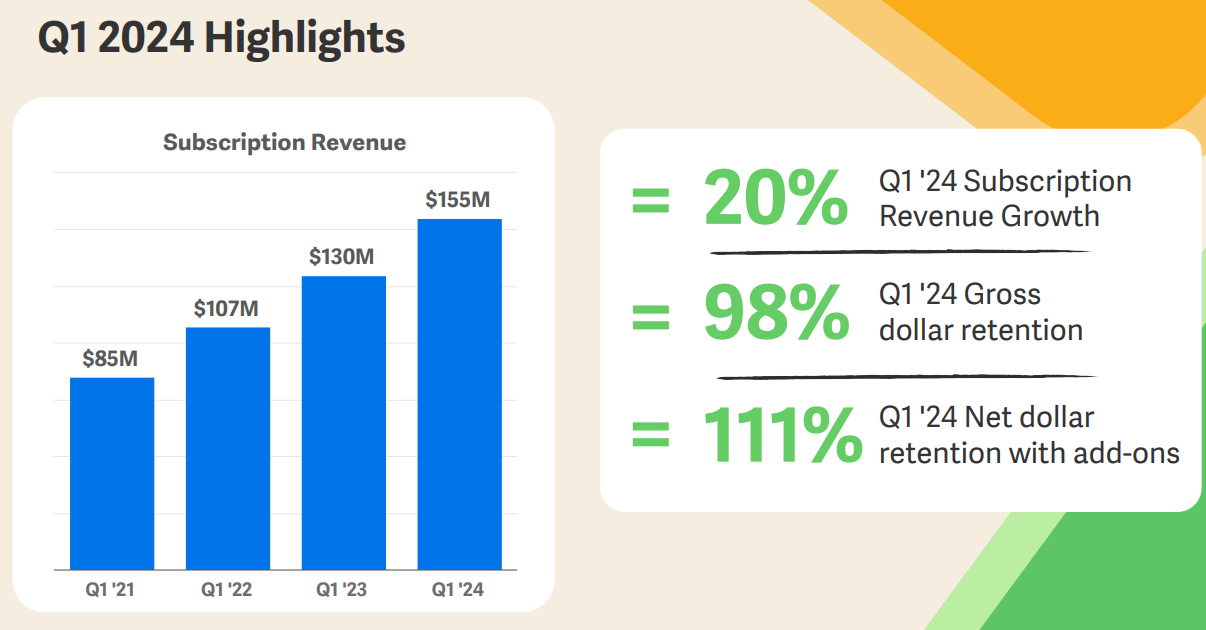

Their new customer growth is relatively slow (6% new logos, ~10 new subscription sales from them) but they’re a retention behemoth! 98% GDR is out of this world for a company of their size and showcases the major fact that once you acquire a customer in this segment, they will stick with you.

-

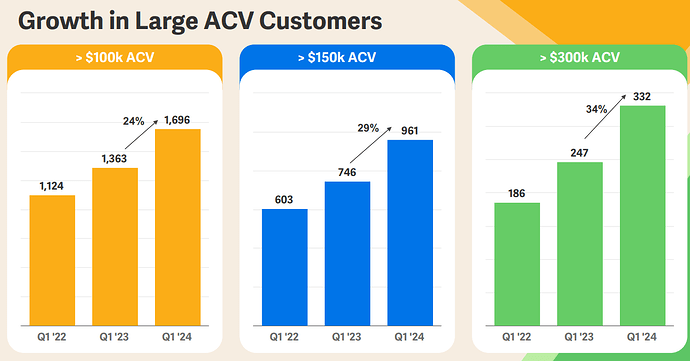

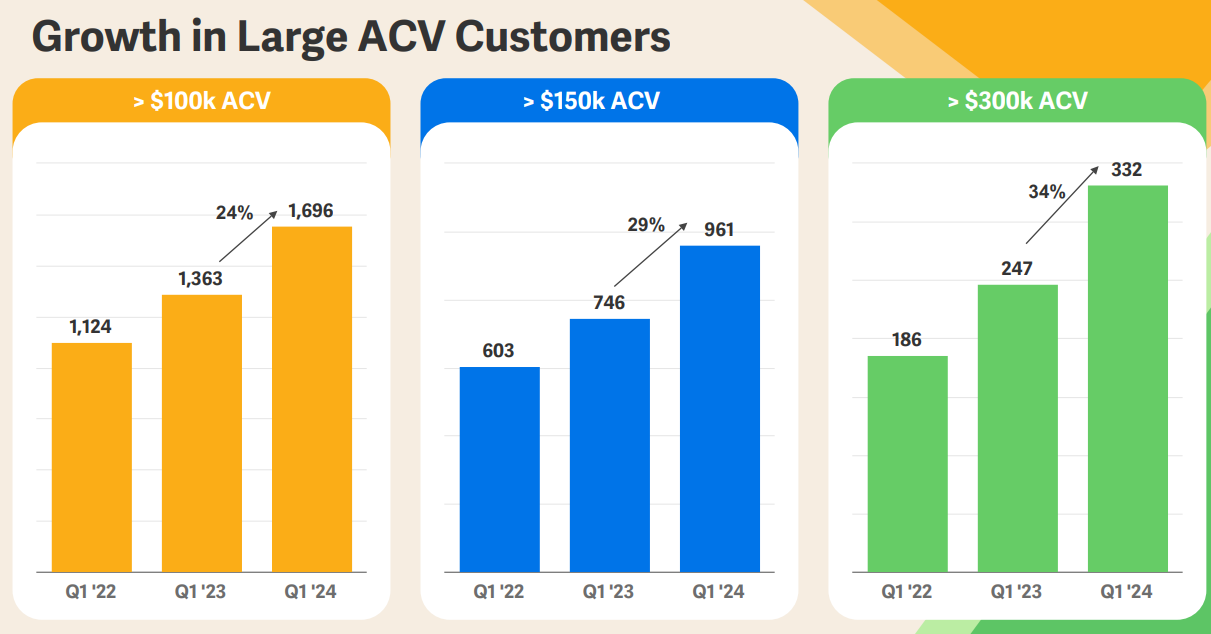

They have been able to drive a majority of their growth by capturing existing customer’s wallet share

-

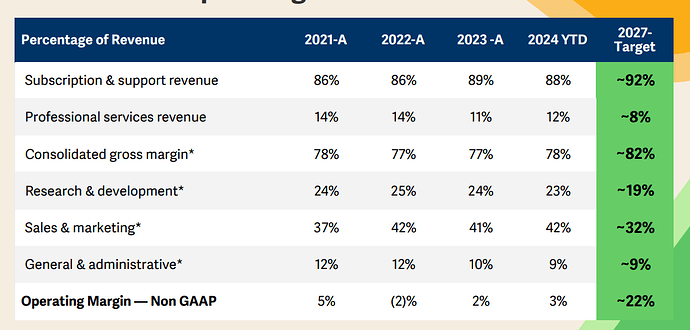

Even with lower CAC, their operating margins are just ~3%. Look at how much they’re spending on Marketing. This is where Iris can struggle because they don’t have anywhere near the capital to spend on marketing.

-

Plus they’re loss making (which is decreasing YoY) at 10% loss in 2024 YTD so far

| Subscribe To Our Free Newsletter |