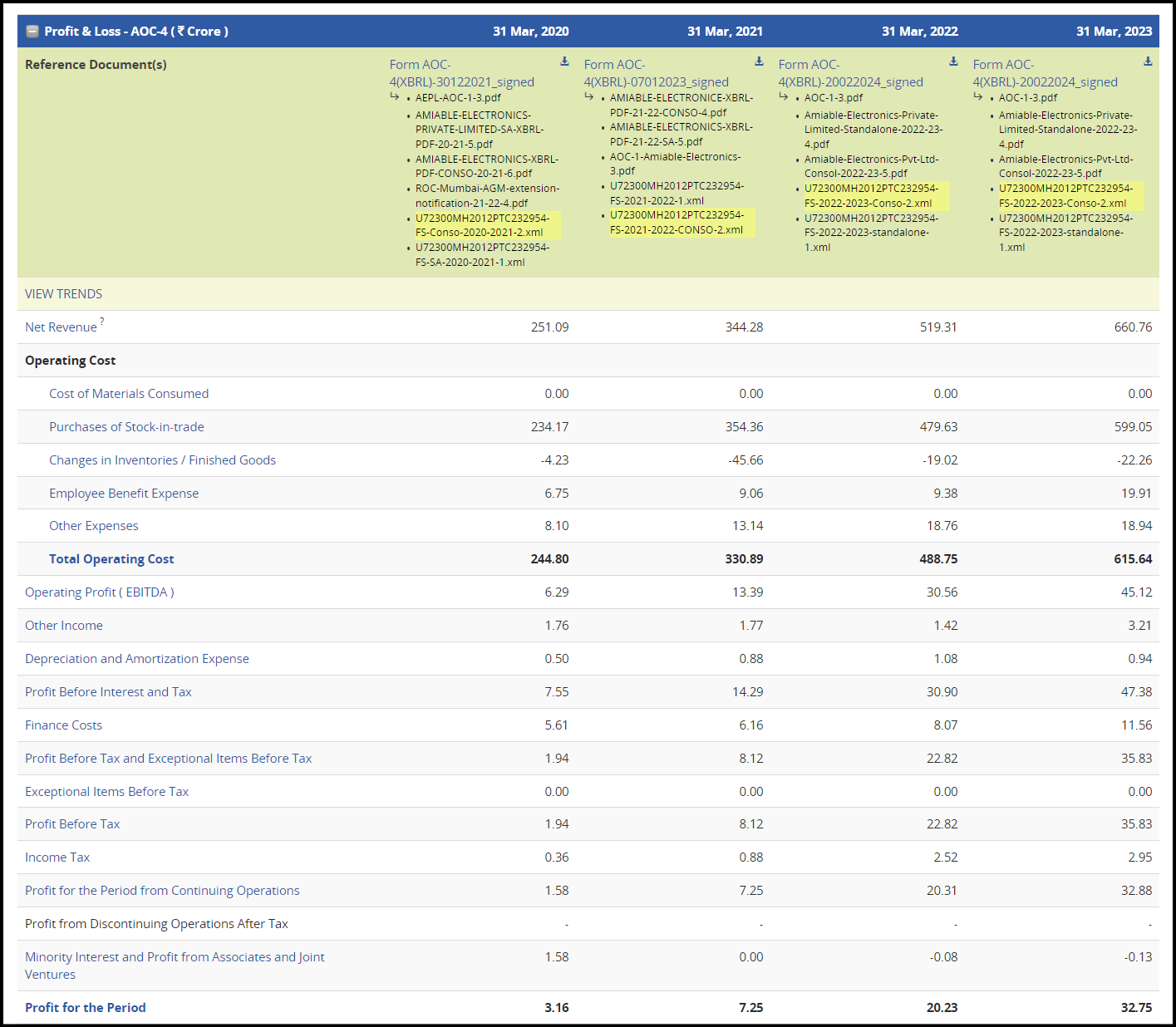

Competitor Financials

Electronics Bazaar

-

Have scaled revenues from 250 Cr. in FY20 to 660 in FY23.

-

Business is almost entirely trading. Generates <10% EBITDA margins.

-

Employee expense is only 3% of revenues.

-

30 Cr. PAT in FY23, around 5% PAT margins.

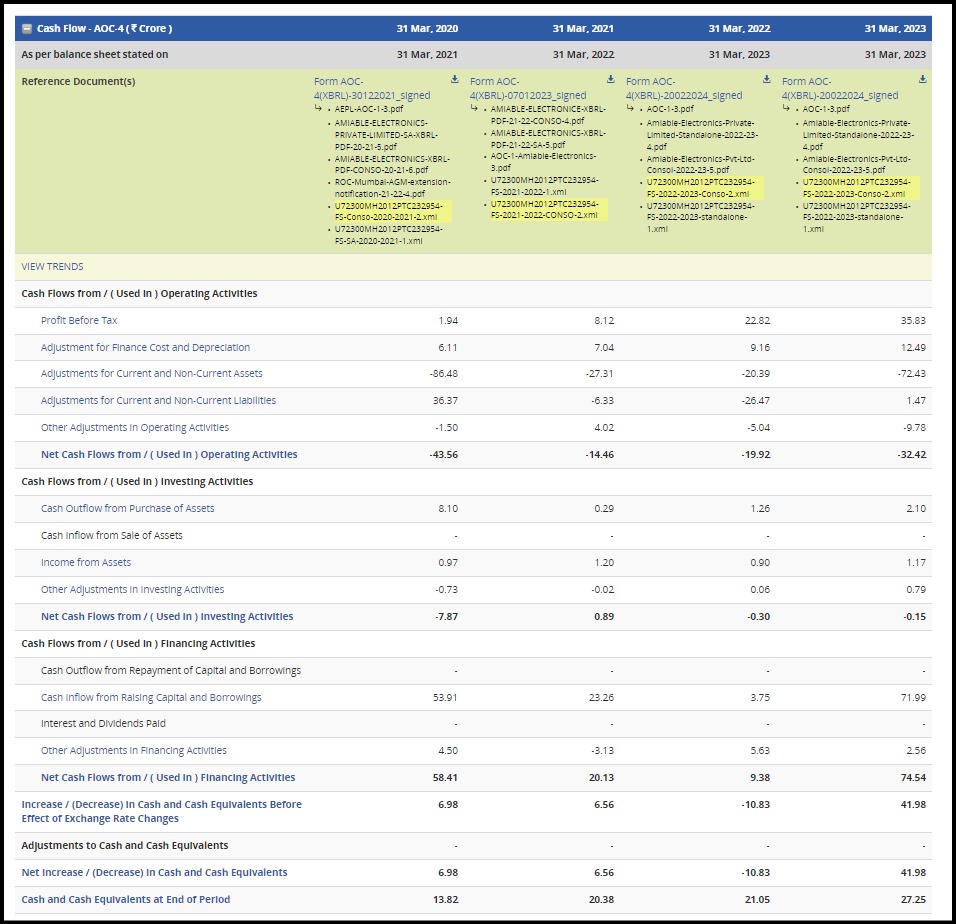

- Negative cash flows despite posting profits.

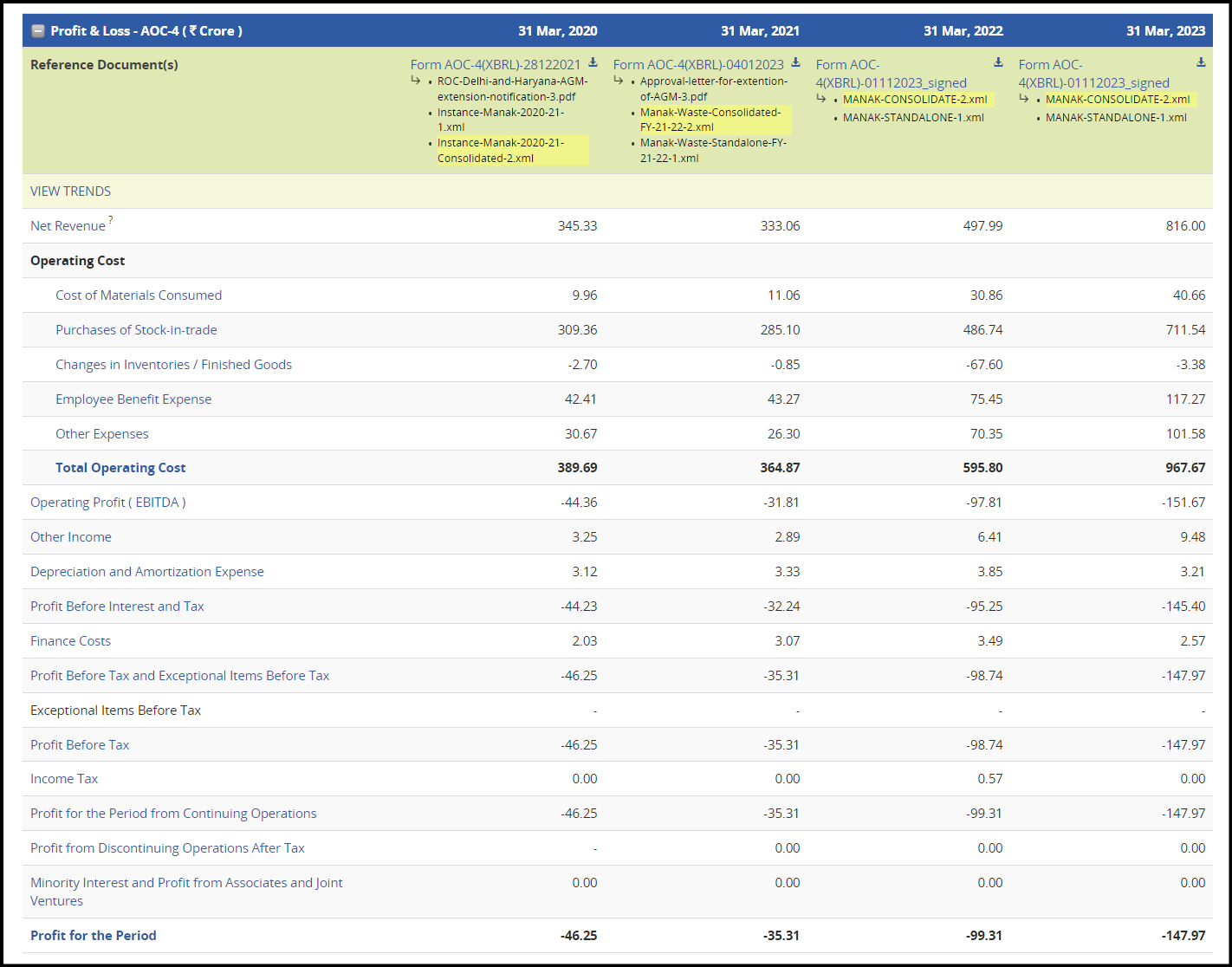

Cashify

-

Cashify sells refurbished phones + other electronics on top of laptops. Not a perfect peer.

-

Scaled revenues from 350 Cr. in FY20 to 800 Cr. in FY23

-

Employee cost is very high given the trading business. Other expenses are equally high.

-

Could have been profitable save for these two line items.

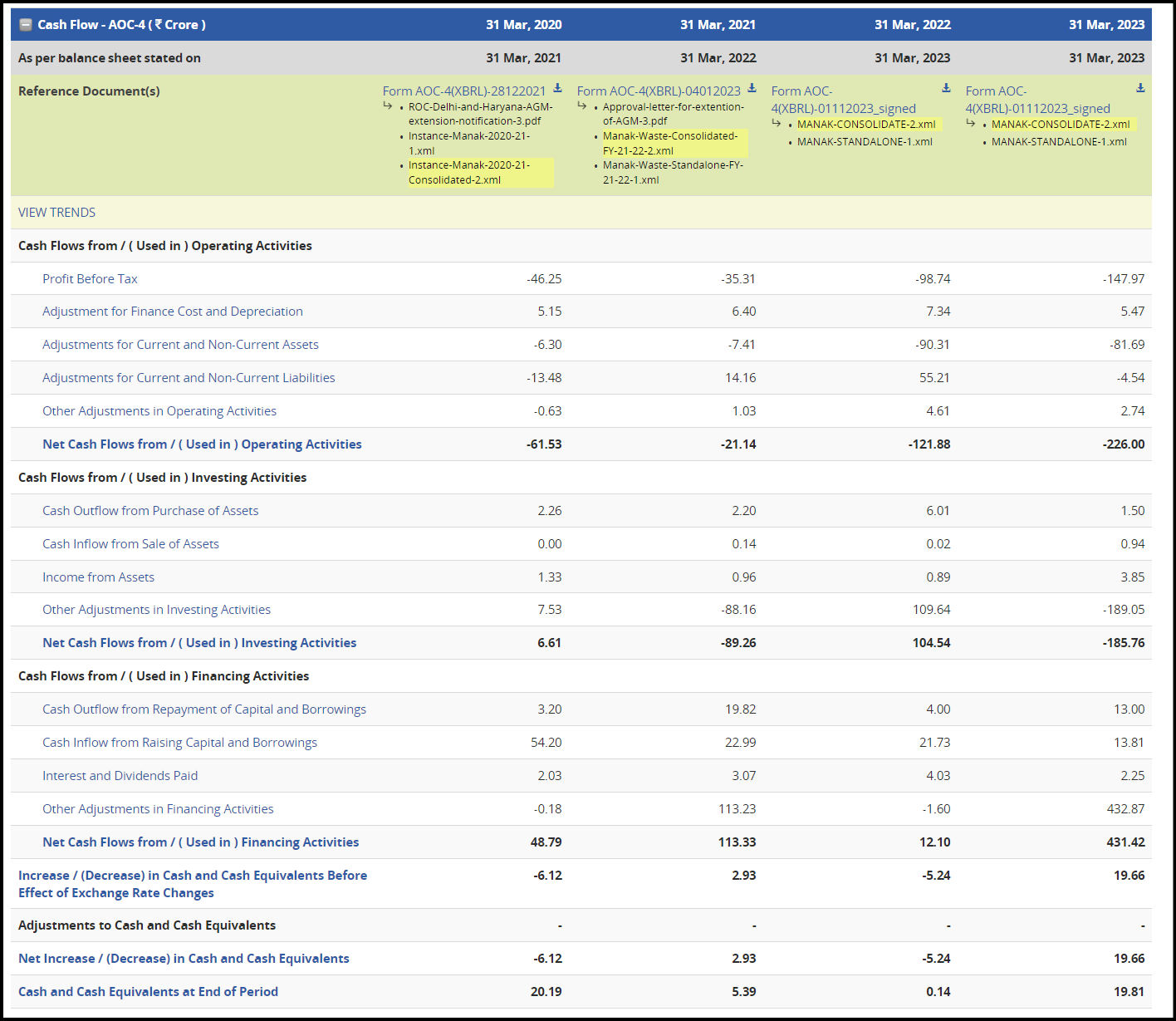

- Cash flows are equally shady with several adjustments. I wouldn’t go anywhere near this business.

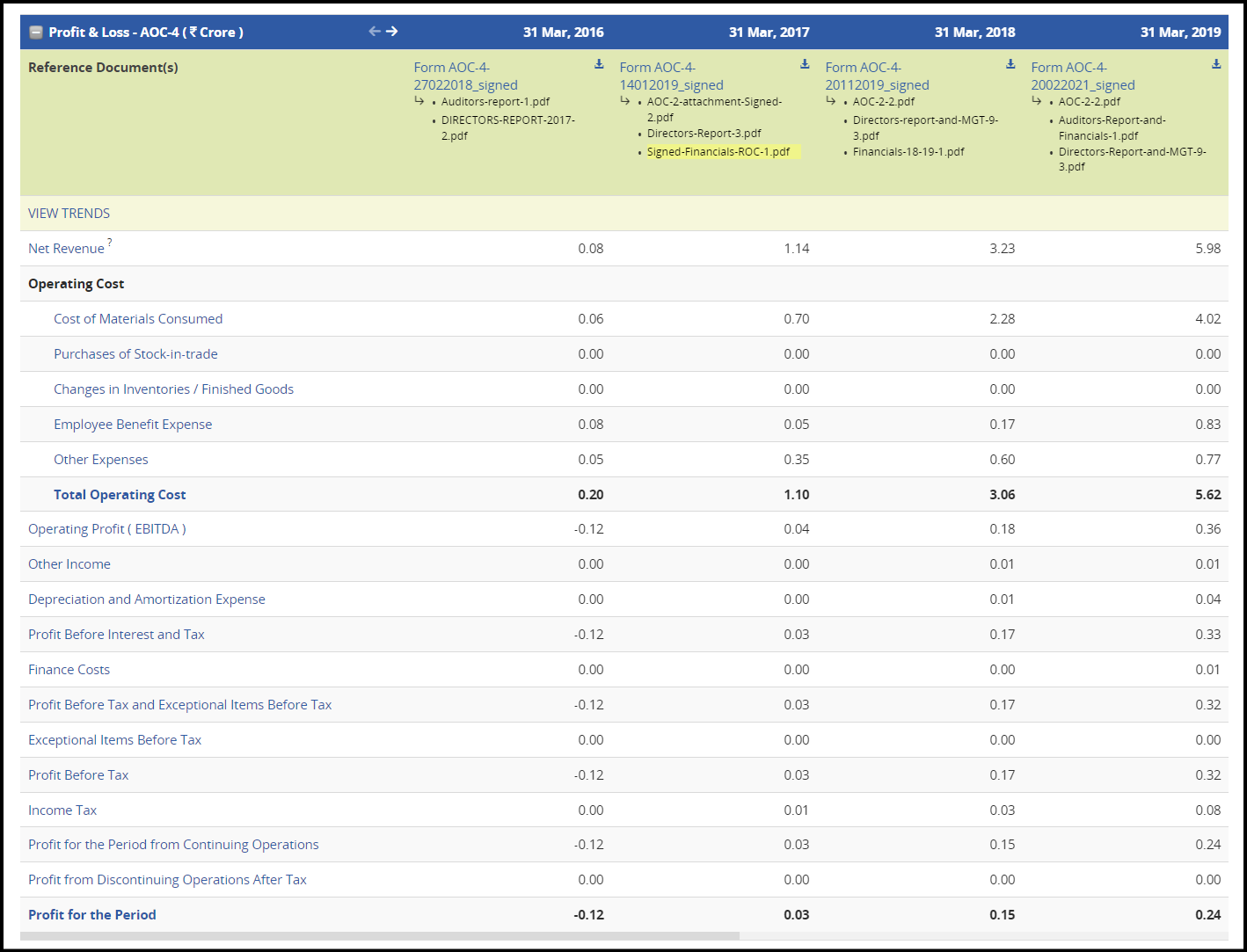

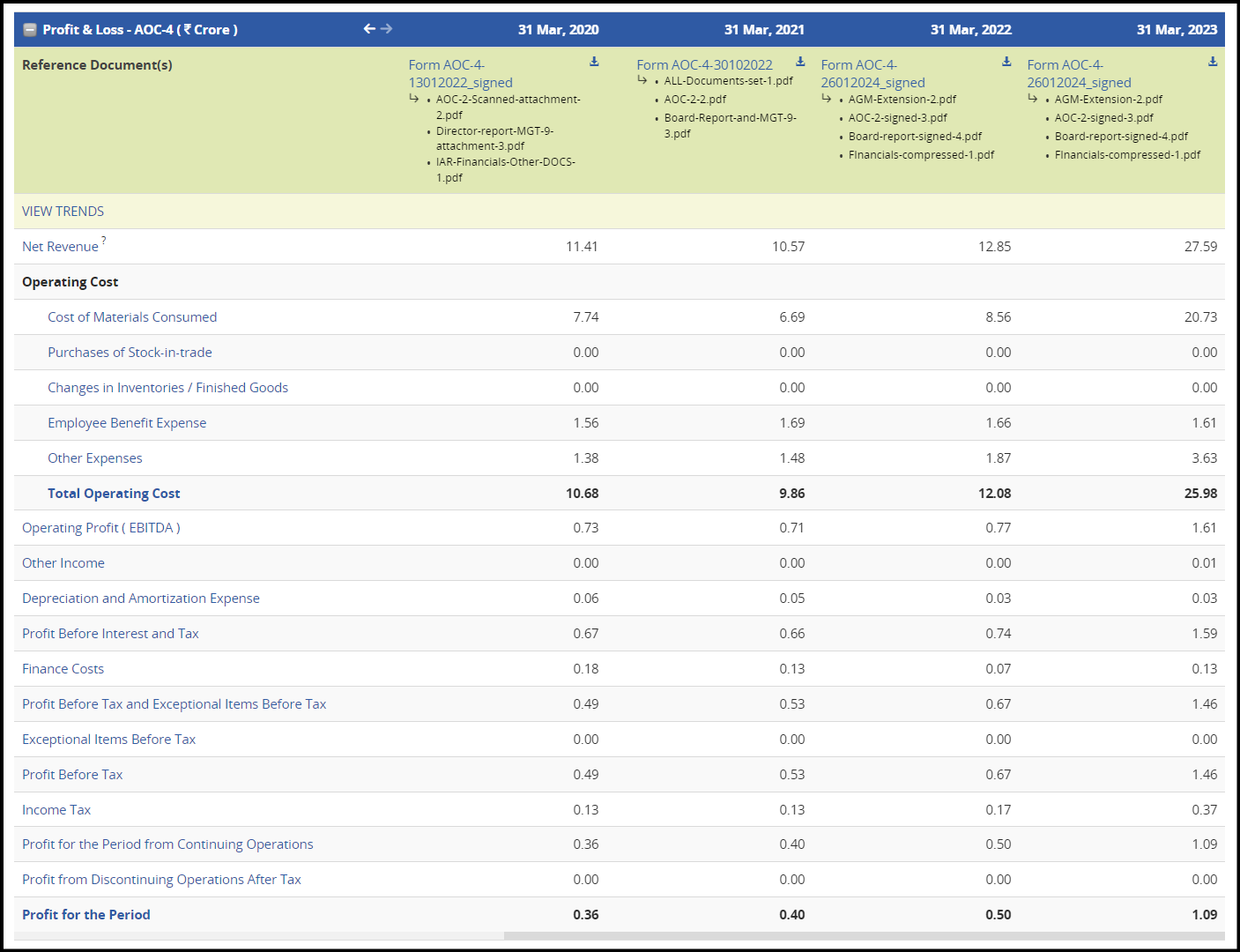

Salori e-Commerce

-

Scaled to 5 Cr. in the first four years of operations, 30 Cr. at the end of 8 years.

-

24% gross margins in FY23.

-

5% EBITDA margins, 4% PAT margins.

-

Looking at these companies, no one seems to be doing any serious refurbishment work (reflected in low gross margins and high trading line items). Management’s claim of competitors being traders looks to be true.

-

This should put to bed any questions about Salori e-Commerce. New Jaisa has scaled to 60 Cr. of revenue in four years, with 47% gross margins compared to 24% for Salori.

-

Electronics Bazaar and Cashify seem to have lots of scale despite poor unit economics. With eventual forays into adjacent kinds of laptops and eventually cell phones, I would expect New Jaisa to eventually reach EB’s scale of 500+ Cr. of revenue.

| Subscribe To Our Free Newsletter |