Source PM kusum govt website https://pmkusum.mnre.gov.in/#/landing

x.com

If you don’t agree with below data, Why don’t you pull data by yourself and show everyone that this are incorrect projections ?

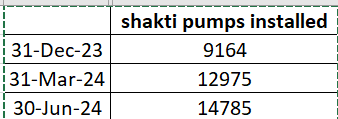

Shakti Pumps Q1 revenue excellent. PAT margin improved to 16.3% vs people expecting EBITDA to be 15%. From solar pumps installation data we got 16001 pumps installed in Q1. Co installed 14785 pumps as per their own investor presentation.

(x.com)

So no of pumps installed is more even QoQ. B2G is their highest revenue earner. Means q1 should be higher than q4. But it didn’t happen? Really (all doubters will run away now) Lets’ compare their 2 investor presentations only. Anyone can do this comparison from the investor presentations.

(x.com)

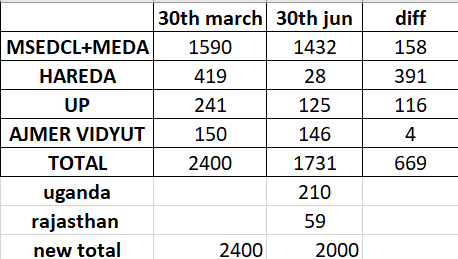

Difference of orderbook between 30th march and 30th june. Only 4 agencies MSEDCL, HAREDA, UP AJMER VIDYUT shows that 670 crores of orders already executed in Q1. On top of this, the export for full year in FY23 was 286 crores so 70 crores per quarter. This quarter declared is just 22 crores. And add the B2B vertical which in Q4 was 130 cr. Add all of these and you would know how much revenue was generated in Q1. Exports aur B2B ko side bhi rakh do. Just the difference of their govt orderbook executed in Q1 is 670 crores.

Bottomline. Expect q2, q3, q4 to be even more blockbusters.

For full year yahi aayega, 3000 cr revenue,

600 cr pat

300 eps available at just pe of 13 vs KSB at 74.

| Subscribe To Our Free Newsletter |