List of the capexes

- FY18: Doing 70 cr. capex for a new surfactant plant in Naidupet (30’000 MTPA capacity; delayed and commercialized in FY21)

- FY21: Greenfield capex of 67 cr. (revised cost: 76 cr.) for premium grade pigments at Naidupet (1’500 MTPA capacity; commercialized in FY22)

- FY22:

- Capex of 21 cr. for specialty chemicals i.e. ingredients for food, cosmetics, personal care (capacity: 1’800 MT) (commercialized in FY23)

- Capex of 24.4 cr. for mixed metal oxides in Naidupet (expected commercialization in FY23)

- Capex for 61.5 cr. for additional pigment capacity in Naidupet (1’500 MTPA)

- FY23

- Capex of 80 cr. in another new Pigments Projects at Naidupeta (capacity: 2250 MT). Expect some portion of the capacity to come online in FY24

- Another project for complex inorganic pigments. Partially completed, balance in FY24. Total cost: 37 cr.

- FY24

- Capex of 80 cr. in pigments (capacity: 1,500 MT) at Naidupeta. Expect commercialization over 18 months, with part of capacity to be commissioned in FY25

AR24 notes

Business related

-

Exports dropped by (-21%) (131 cr. vs 165 cr. in FY23)

-

Export volumes dropped by (-21%). Domestic demand compensated for drop in exports

-

Witnessed pricing pressure across segments due to declining input costs resulting in lower realization. Margins were lower due to high-cost inventory

-

Capacity utilization of Sulphonation plant at Naidupeta improved from H2FY24 and is expected to stabilize in FY25

-

Power & fuel costs : 31.88 cr. (vs 36.17 cr. in FY23)

-

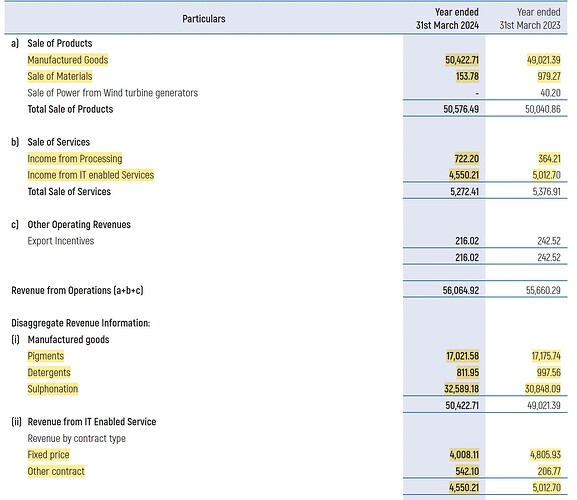

Revenue breakup

-

Other expenses: 68.8 cr. (vs 72.13 cr. in FY23)

Pigment Division:

- Revenue 135 cr. (vs 158 cr. in FY23), -14% and volumes -2%

- Domestic industrial market witnessed robust growth while exports fell

- Expanding customer base in international markets by tapping new areas

- Ultramarine Specialty Chemicals Ltd. achieved a capacity utilization of 82% (revenue of 38 cr. vs 16 cr. in FY23)

Surfactants Division:

- Revenue 343 cr. (vs 333 cr. in FY23)

- Lower realizations. They added more specialty chemicals through in-house development efforts, which will help improve the bottom line

Wind Power Generation

- Own and operate 6 wind turbine generators at 3 locations in Tamil Nadu, capacity of 4.3 MW

- All the units generated are consumed at Ranipet and Ambattur Plants

- Generated 61 lakh units (vs 61.84 lakh units in FY23)

- Captive consumption 61 lakh units (vs 49.36 lakh units in FY23). Green energy contributed 55% of consumption in chemical division

ITeS Division:

- Revenue: 46 cr. (vs 50 cr. in FY23). PAT: 12 cr. (vs 15 cr. in FY23) (exports of 42.08 cr.)

- Scheduled end of certain projects in healthcare caused an overall dip in revenue

Capex

- Subsidiary commissioned a facility to manufacture Inorganic Pigments

- Adding capacity of 1,500 MT in Pigments in the subsidiary at Naidupeta with a capex of 80 cr . Expect commercialization over 18 months, with part of capacity to be commissioned in FY25

- PPE addition is in freehold land (Industrial Park, Naidupet) + buildings and plant & machinery

Subsidiaries

- Ultramarine Fine Chemicals Limited is yet to commence operations

R&D

- One product was commercialized

- Capital: 2.99 cr. (vs 0.3 cr. in FY23). Recurring: 2.17 cr. (vs 1.99 cr. in FY23)

- Total : 5.16 cr. (vs 2.3 cr. in FY23)

Miscellaneous

- Permanent employees : 472 (median remuneration increased by 9%)

- Auditor remuneration : 27.65 lakhs (vs 28.8 lakhs in FY23)

- Shareholders : 22’168 (vs 23’036 in FY23)

- Share price : 306.3 (low), 463.3 (high)

- Investment in Thirumalai : 478.47 cr. (vs 351.36 cr. in FY23) affected by MTM

- Receivables : doubtful of 3.11 cr. (same as FY23). Fully provisioned

- Most bank loans are at 6-9.25%

Disclosure: Invested (no transactions in last-30 days)

| Subscribe To Our Free Newsletter |