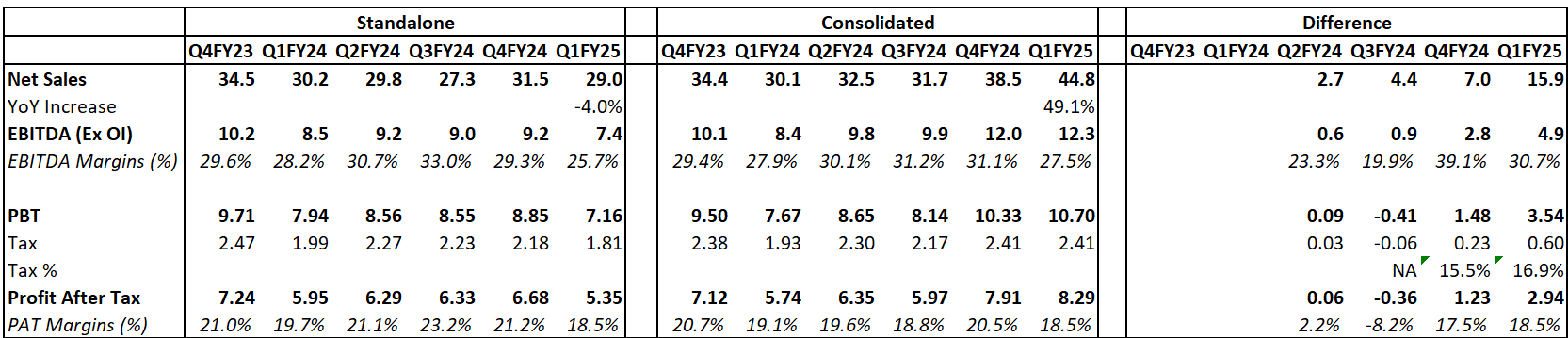

One thing which to be noted is that the new capex which they have done is under a 100% owned subsidiary. Although the difference can be because of other subsidiaries too, but the primary delta seems to be from the new plant.

The fact is very well known that the new plant is very efficient in terms of production and also has better quality of ramming mass.

By comparing the numbers (consol (-) standalone), it might be seem like the new plant is doing very well! Q1 is typically a weaker qtr for the company, but still the new plant might be doing 30% EBITDA margins. I will be little skeptical to reach to conclusion very quickly that they might have done 39% EBITDA margins in Q4, but this is definitely interesting.

Happy to be corrected if this logic is flawed.

| Subscribe To Our Free Newsletter |