Q1 FY25 Results Presentation

COMPANY OVERVIEW

•100+ Countries Exports ₹

•4 Countries Operations

•16 Manufacturing facilities

•9000 global workforce

Q1 fy25

•₹ 3464.1 cr. Revenue (3.8% YOY)

•₹ 645.9 cr. EBITDA (-11.yoy)

•₹ 252.2 cr. PAT (-29.8%) yoy PAT Margin 7.3%

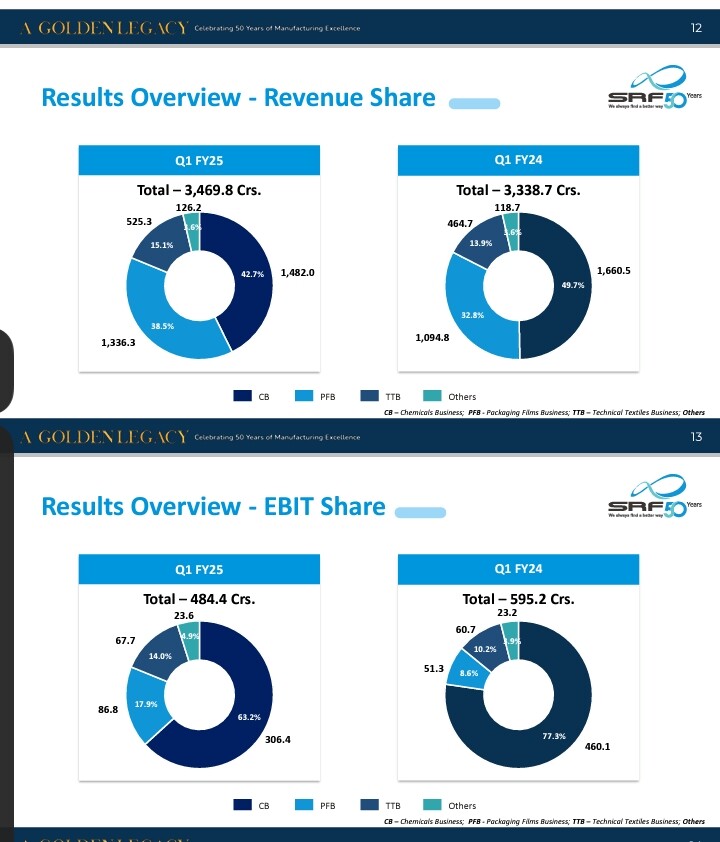

•48% chemicals 34% packaging films 18% technical textiles and others

Overview Business Profile

Chemicals

No of Plants 2, EBIT ₹2 1,627 cr. Revenue Rs. 6297 cr

Packaging Films

No of Plants 8 , EBIT Rs. 207 cr , revenue Rs.4489cr

Technical textiles

No of plants 4, EBIT Rs. 274 cr, Revenue Rs.1898 cr.

•Domestic market leader in Tyre Cord manufacturing and Belting Fabrics Tyre

• ~40% share in India’s Nylon tyre cord market 5th largest player globally

• 2nd largest manufacturer of Conveyor Belting Fabrics in the world

Others (Coated Fabrics,Laminated Fabric)

No of plants 4, EBIT Rs. 93 cr , Revenue Rs. 465 cr growth Drivers

•Continue to build new competencies in the Chemicals Technology space

•Build and maintain market leadership in business segments

•Greater focus on ESG initiatives • • •

• Benefit the communities where we work •Embrace diversity, equity & inclusion

•Enhance focus on the 3R’s Reduce,Recycle, Reuse

•Increase consumption of green/renewable sources of energy

•Nurture innovation through R&D

Results overview revenue and Ebita share

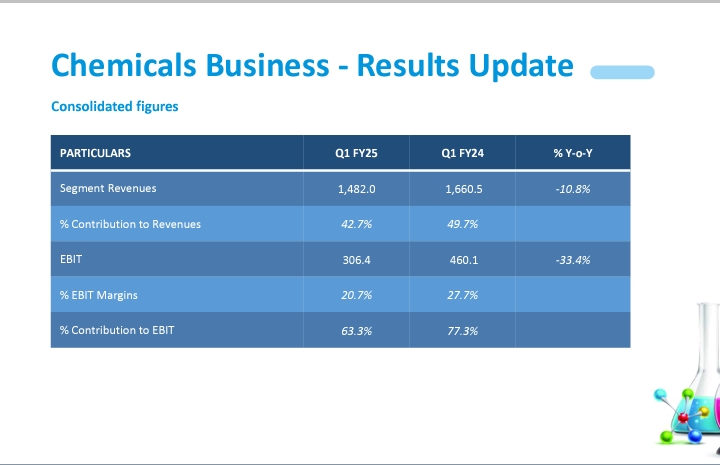

Chemicals Business

Specialty Chemicals Business key highlights

•Inventory rationalization trends continued in Agro chemicals market, impacted performance ➢To prioritize process improvements and cost efficiencies through tech breakthroughs as margin improvement initiatives

•Focus on ramp-up of multiple new plants commissioned in FY’24

•Multiple AIs in advanced stages of commercialization; to contribute to future growth

Market Trends

Agrochemical companies continue to focus on inventory rationalization

•Demand subdued for certain key Agro intermediates

•Chinese manufacturers continued pushing cheaper Agrochemicals and intermediates in the market

•India’s momentum as a key specialty chemicals manufacturing base remains fundamentally strong

Chemicals Technology Group

•Chemicals Technology Group (CTG) is actively engaged in the development of new process technologies

•Key focus on high end molecules

•Strong internal competencies and capabilities •Equipped with state-of-the-art R&D facilities and an ingenious team of scientists and engineers

•2 R&D centres in India – Bhiwadi, Rajasthan and Gurugram, Haryana

•2 new process patents granted in Q1FY25

•151 Global Patents granted

•451 patent applied

Fluorochemicals Business key highlights

Refrigerant gases performed well in the domestic market

➢HFC volumes witnessed significant growth over CPLY

➢Demand for Dymel®/ Pharma propellant remained strong

•Witnessed reduced volumes and pricing of R125 in the US market

•CMS products continue to witness pricing pressures due to agro chemical demand being weak; pulling down the overall performance •PTFE gaining traction in domestic market; work on free flow and fine cut grades continuing as planned

Market Trends

•Global Ref gas demand expected to remain stable to strong, with growth in India and the Middle East, while the US market may see a decline due to reduced HFC consumption

•Implementation of Chinese HFC quotas and consumption growth should help stabilize Ref gas prices

•Key raw material prices were stable

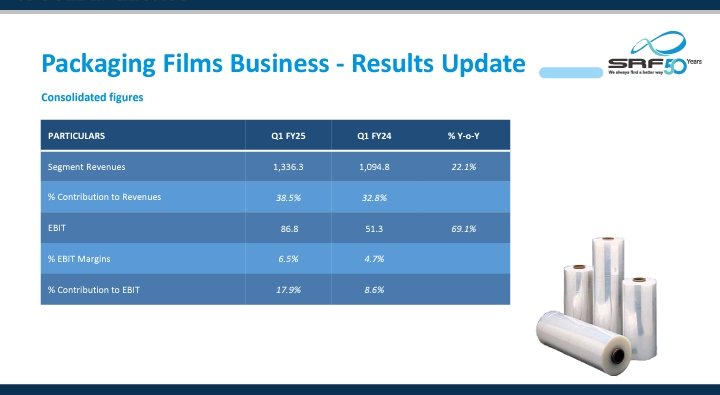

Packaging Films Business – Results Update Consolidated figures

Key Highlights

•BOPET witnessed some pricing improvement towards end of June; however supply still far exceeds demand

•Higher BOPP margins due to balanced demandsupply scenario

•Significant increase in VAP sales over CPLY

•Aluminium foil export sampling under way; anticipate ramp-up towards H2

•Continue to focus on optimizing product mix and cost efficiencies, increase VAP sales and new product development to counter market challenges

Market Trends

•Significant global demand-supply gap remains due to new BOPP and BOPET lines being commissioned in China and India

•BOPP demand continues to benefit from sustainability related actions

•Freight costs witnessed significant uptrends due to shipping line challenges

•Severe competition from Chinese players likely to continue in South-East Asia

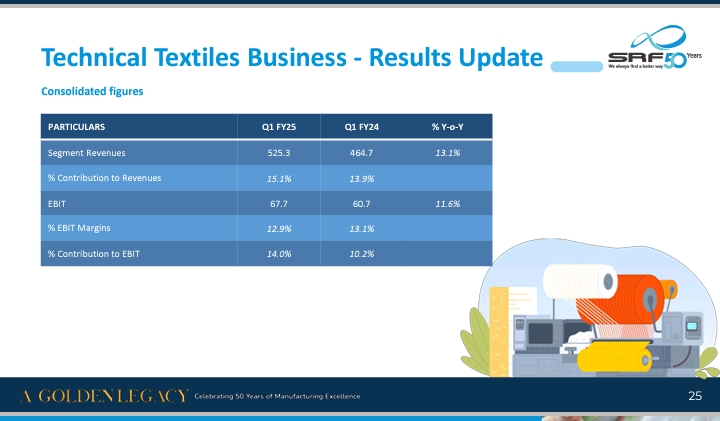

Technical Textiles Business – Results Update

Key Highlights

•Segment performance was steady with healthy volumes reported in Nylon Tyre Cord Fabrics (NTCF) and Polyester Industrial Yarn (PIY)

➢Continued emphasis on highermargin value-added sales

•Lower volumes witnessed in Belting Fabrics (BF)

•Enhanced use of renewable energy a

•Dipping and BF capacity expansion projects progressing as planned

Market Trends

•Demand for NTCF and PIY remained strong, while demand for BF declined

•2/3-wheeler vehicle segment witnessed robust growth

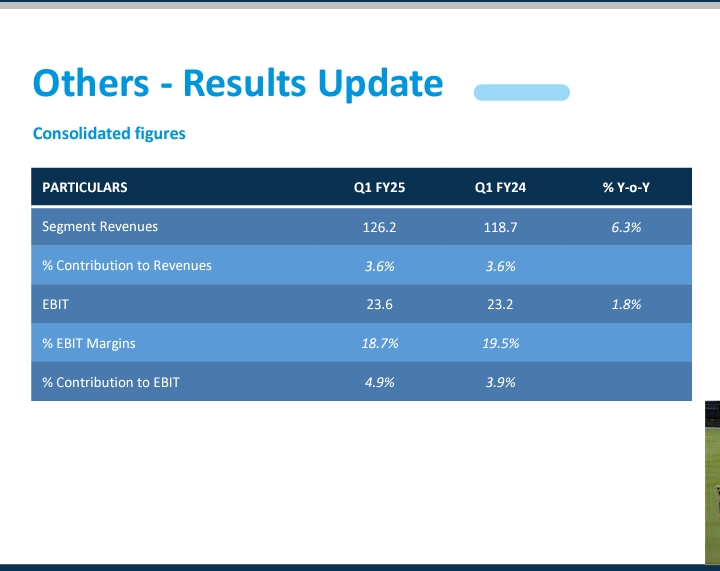

Others

Coated Fabrics

•SRF retained its leadership in domestic market in volume & price

•Achieved record domestic sales during the quarter, with strong demand anticipated in Q2 due to seasonal trends

•Business aims to improve profitability by enhancing domestic volumes through VAPs and expanding in new segments

Laminated Fabrics

•Business maintained its price leadership by selling at full capacity

•Oversupply situation continues; putting pressure on margins

•Expect demand slowdown for outdoor campaigns in Q2 due to monsoons

Outlook – Chemicals Business

Specialty Chemicals

•Agrochemicals segment likely to show improvement; demand to pick up gradually

•Work on AIs progressing as per plan

•Product funnel remains strong

•Launch of new pharma intermediates and ramp up of recently commissioned facilities to drive growth

•Tech interventions in reducing costs / steps for certain key products should counter-balance pricing pressure

Fluorochemicals

Focus on maximizing HFC production

•SRF’s integrated play provides significant advantages

•CMS demand and prices likely to be stable; creating export ability to offset pricing pressure •PTFE should witness traction around value added grades in H2 FY25 •New HF plant commissioning in Q2; should provide cost advantages post-stabilization

Outlook Packaging Films Business

•Expect ongoing demandsupply imbalance and margin pressure to continue in BOPET

•Rampup in sales of identified VAPs in both BOPET and BOPP

•Hungary expected to perform better, owing to increased sales to Mainland Europe

•BOPP to perform relatively better

•Newly commissioned Aluminium Foil facility to contribute positively to the overall performance in FY25

•South Africa to continue performing well

Outlook Technical Textiles Business

•Demand for NTCF likely to be stable •Focus on highend VAPs in BF and expanded capacity to be the future growth drivers

•Polyester and Nylon Industrial Yarn sales witnessing positive trends

Disc -Tracking

| Subscribe To Our Free Newsletter |