I agree with the profit part, but I don’t understand how this RM addition and Dubai investment could affect the WM segmental revenue(topline) growth.

In fact, looking at the WM segment on a longer time frame

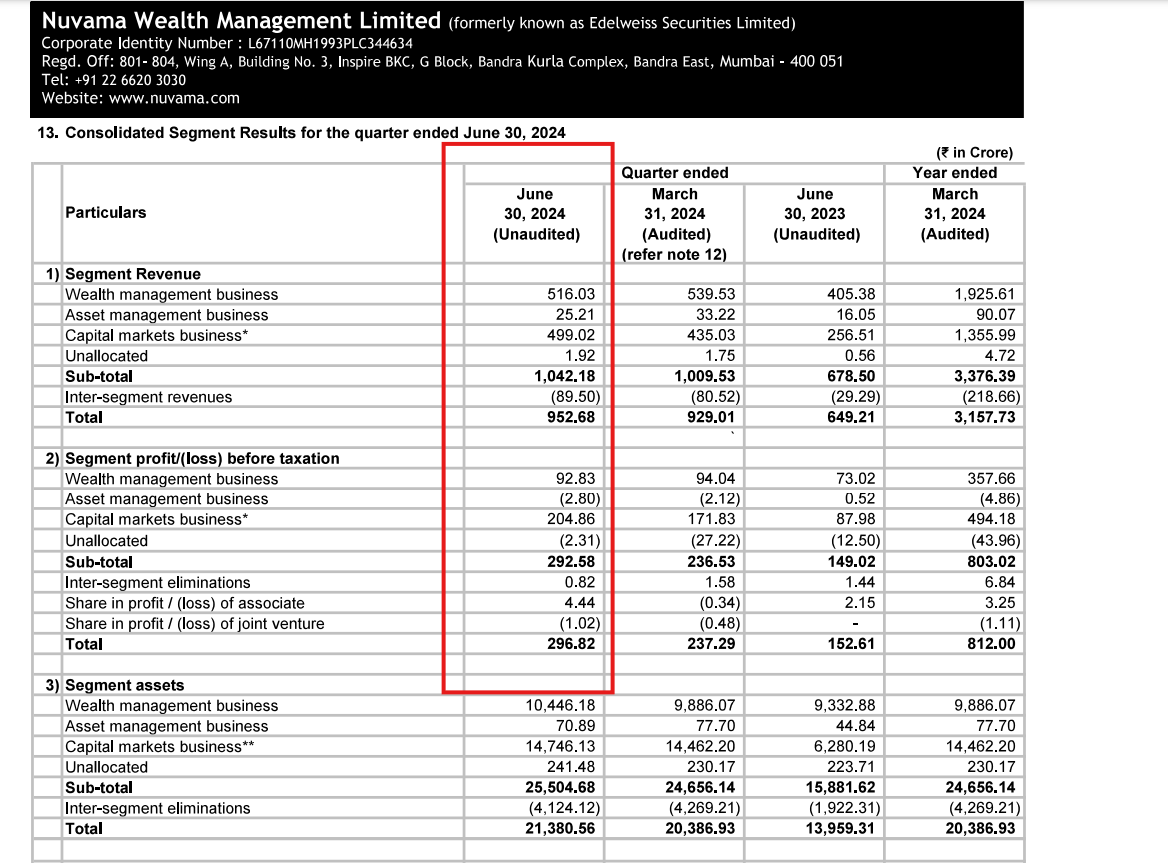

Revenue: Q2FY23 → 455 : Q1FY25 → 516

PBT: Q2FY23 → 105 : Q1FY25 → 93

I know revenue to AUM should not be looked at in a linearity. But in about 2 years where AUM grew 30-40% CAGR, where is the incremental ARR?

On a positive note, I hope the WM revenue can jump exponentially in the coming quarters, looking at how revenue recognition has been falling behind the exceptional AUM growth.

| Subscribe To Our Free Newsletter |