Skipper Ltd

Skipper Limited (Skipper) is a Kolkata based company, incorporated in 1981. It is India’s

largest manufacturer of Transmission & Distribution (T&D) structures and ranks among

the top 10 globally.

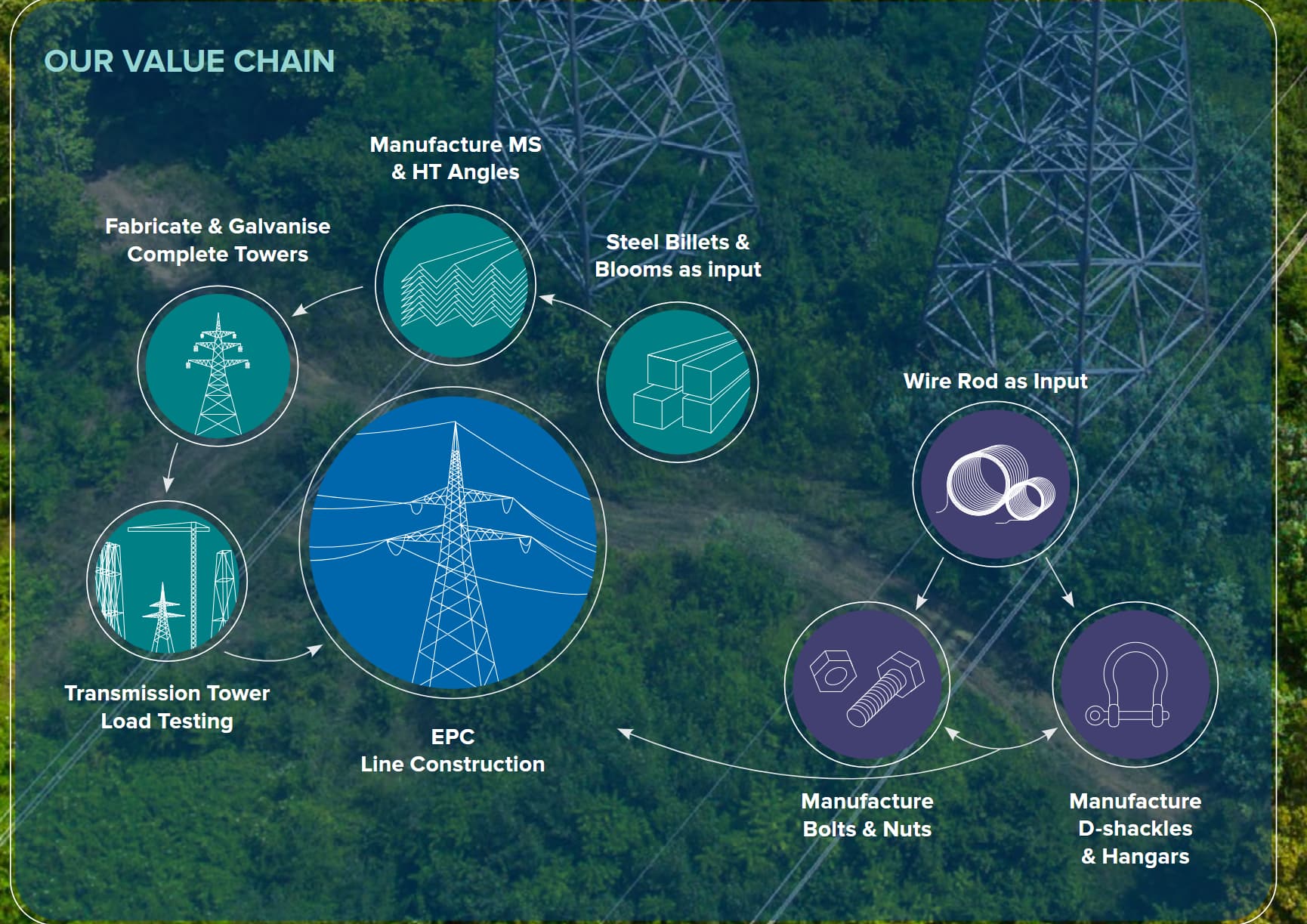

It is world’s only Integrated T&D company having its own Structure rolling, manufacturing, Tower Load Testing Station & Transmission Line EPC.

Source:AR

The company is managed by an experienced management which includes Mr. Sajan Kumar Bansal who has more than 3 decades of experience in same line of business who is ably supported by his three sons and qualified personnel.

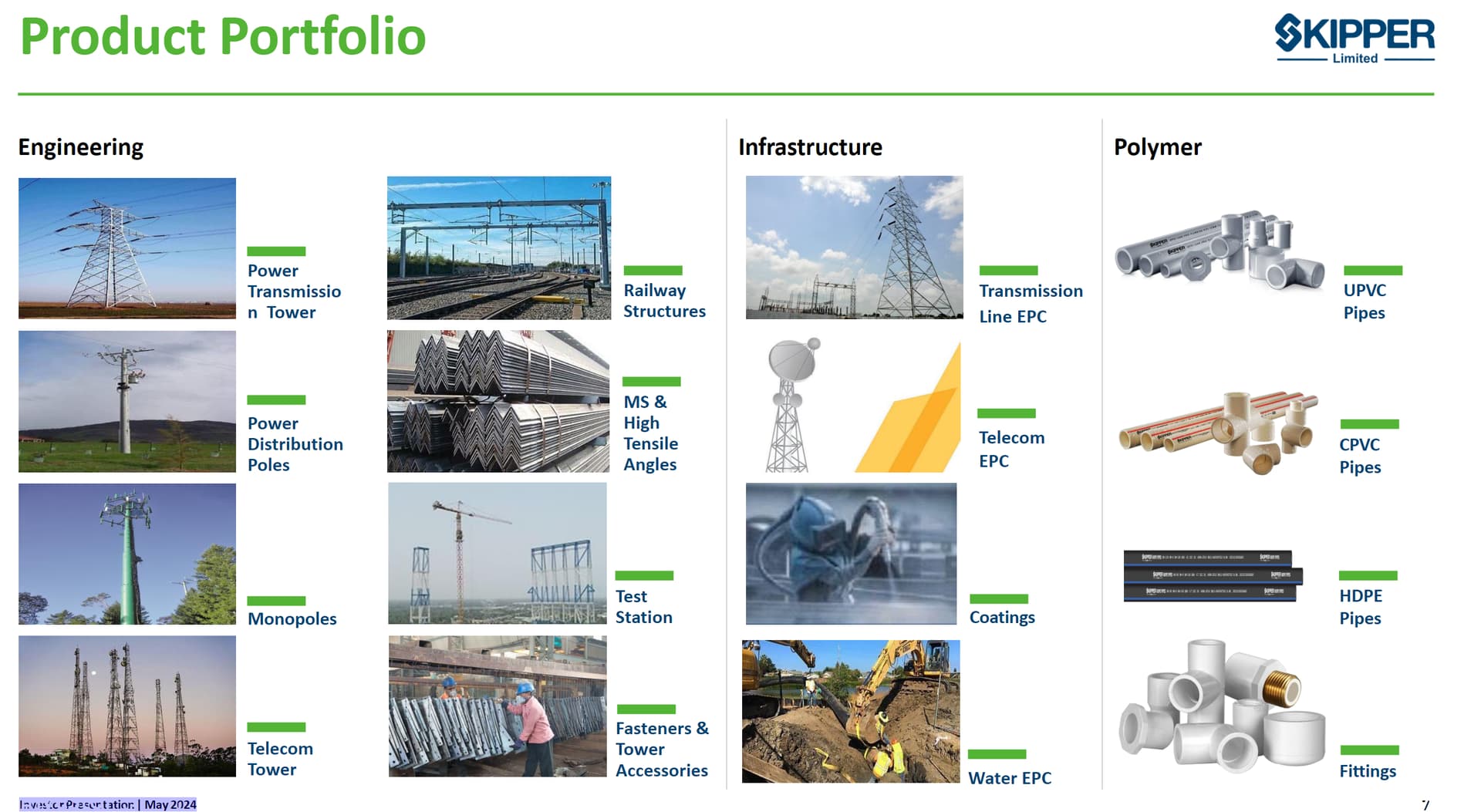

Engineering Products:

What are Transmission Towers?

Transmission towers are used for evacuation of bulk electricity at higher voltages from power

generation plants to remote locations over large distances. They are used in high-voltage

AC and DC lines and come in many shapes and sizes. Skipper manufactures the entire

spectrum of transmission tower from 66KV to 800 KV. It also has the capability of

manufacturing 1200 KV towers.

The need for T&D infrastructure:

Renewable energy has emerged as a cost-effective solution to power various sectors globally, leading to a surge in renewable generation assets. However, the best locations for these assets are often distant from existing power grids, necessitating significant investments in power evacuation infrastructure. To meet long-term sustainability goals, the International Energy Agency estimates a 50% increase in global grid spending in the next decade will be necessary. This includes crucial investments in the approximately 7 million km of transmission lines worldwide to efficiently transport increasing amounts of renewable energy and manage supply and demand volatility.

Building new renewable energy projects will be futile if they cannot be dispatched to the grid due to transmission network limitations.

Polymer Products:

It manufactures polymer pipes and fittings.

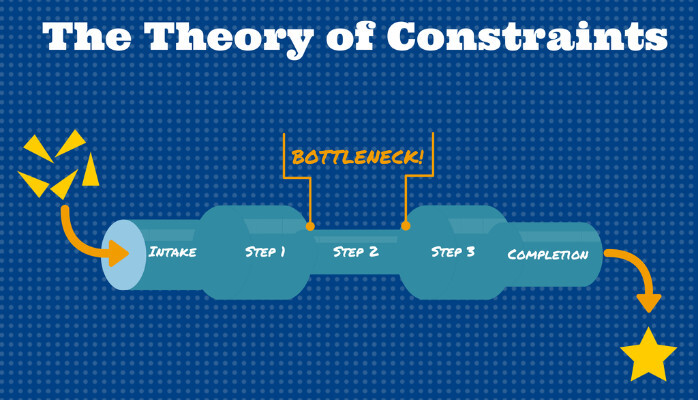

Only polymer pipe company in India to implement the Theory of Constraints (TOC) into its operation.

It is a beneficiary of the Jal Jeevan Mission with a capital outlay of Rs 7 billion announced in the Union Budget. Also a proxy to the rural economy and Real estate upcycle.

Infrastructure segment:

Skipper manufactures various Power Transmission structures, Telecom Towers, and

Railway Electrification Infrastructure. The company has thus forward integrated itself into EPC projects in these sectors and thus has full control over the entire value chain.

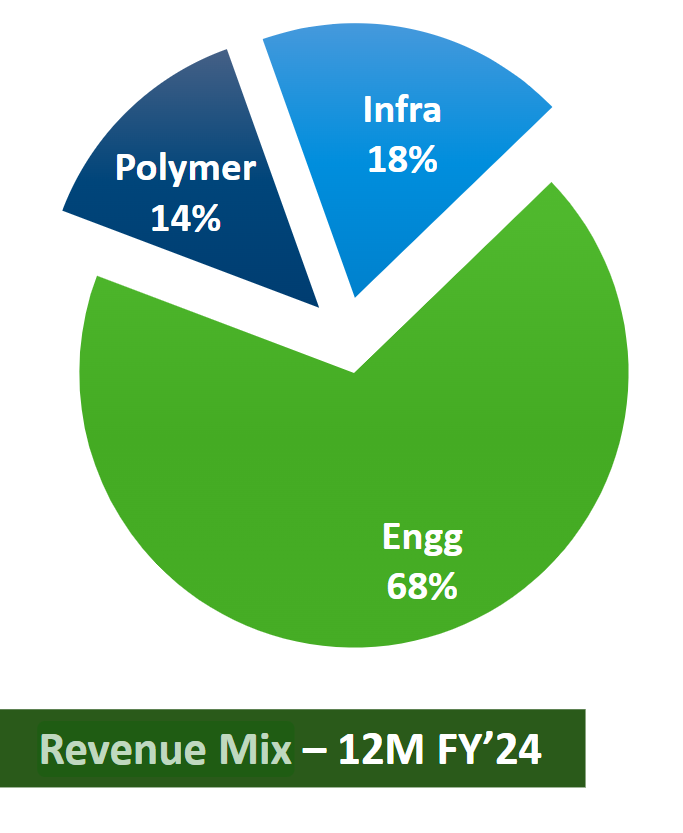

The Engineering and Infrastructure segments serve the same market, with Infrastructure representing a downstream extension of Engineering. Thus it a key beneficiary of Railway Electrification Infrastructure, T&D capex and Telecom tower capex.

Its Polymer Segment is low margin low ROCE business and the company had announced a demerger of its Polymer business in 2018 but subsequently had withdrawn it in 2019, now I was not able to find the exact reason for it but ig it was maybe as it did not have enough scale and function as a standalone business and also the company was facing high leverage due to which the demerger plans might have been cancelled.

TAM for T&D:

TAM in India:

To accommodate the increasing share of renewables in India’s energy mix, the country’s transmission infrastructure requires a significant overhaul. With the government targeting a capacity of 500 GW of renewable energy by 2030, it necessitates building a grid capable of evacuating power from these projects, estimated at a value of Rs 2.5 trillion. This undertaking is equivalent to constructing

the current grid and is crucial to ensuring the successful integration and utilisation of renewable energy sources in India’s power sector.

Now before we get too excited with the massive addressable market lets see what issues it faced during the previous 2015-2019 cycle.

It had a massive addressable market back then too:

Source: Anand Rathi Research

Till 2018 they were increasing their sales also due to operating leverage and higher capacity utilisation they were able to generate good operating cash flows which was invested in capacity expansion from 175000 MTPA in 2015 to 265000 MTPA in 2018 for T&D structures.

Also it tried to diversify itself into PVC pipes which was not a good capital allocation decision as this segment has dragged its overall performance due to low margins and low ROCE.

Despite securing MS Dhoni as a brand ambassador, the company has yet to see a positive impact on brand building or profit margins.

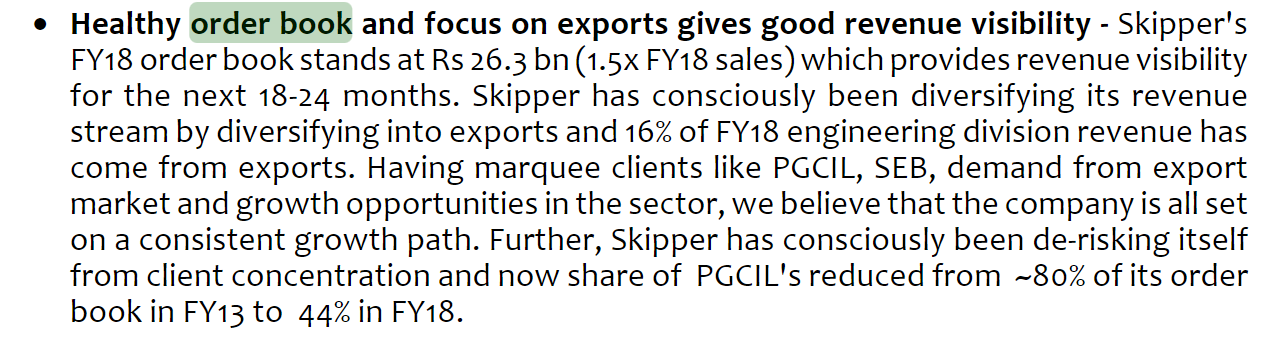

In 2018 the company had good order book which provided revenue visibility for 2 years.

Even after having healthy order book its sales fell the next two years with a decline in operating margins as well.

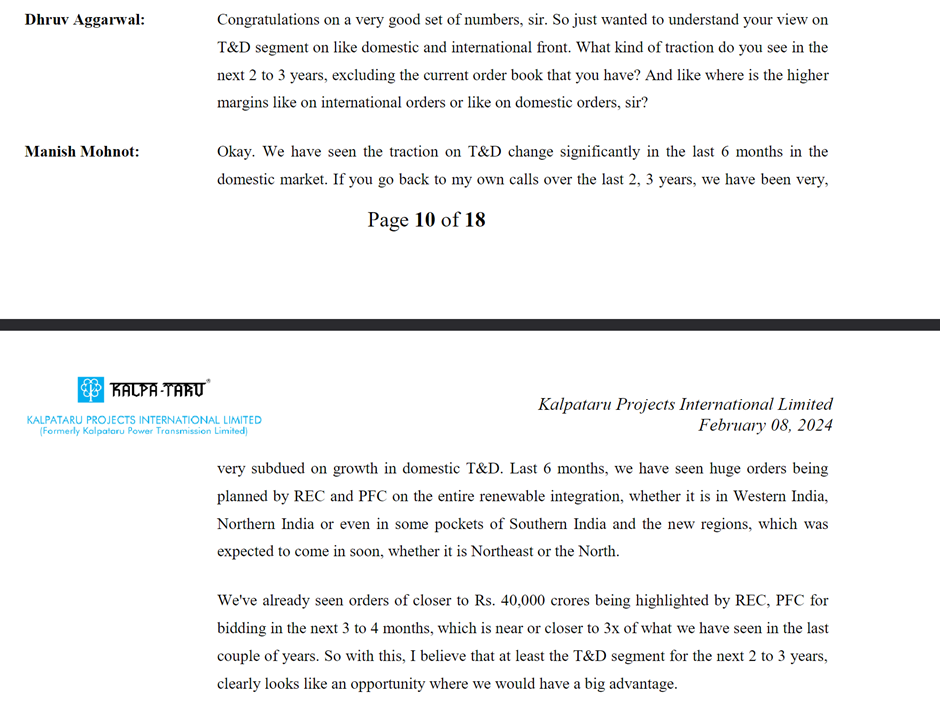

Currently we have a similar narrative with aggressive Infra Capex and need for T&D structures currently Skipper has revenue visibility for next 3 years with 25% CAGR revenue guidance given by the management for the next years.

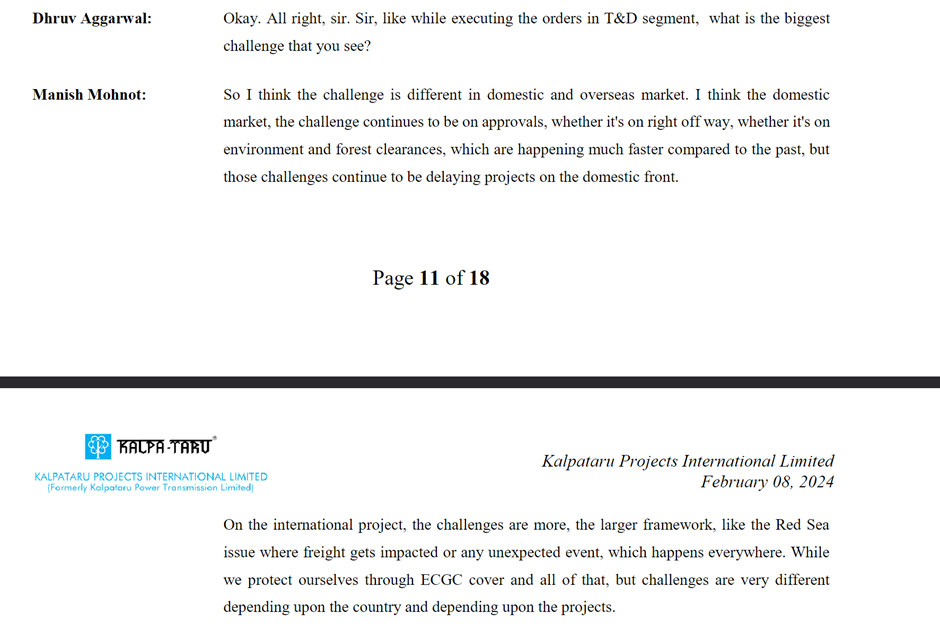

Historically T&D sector has faced major issues in executing its order book:

Source: Jyoti Structure 2015 AR

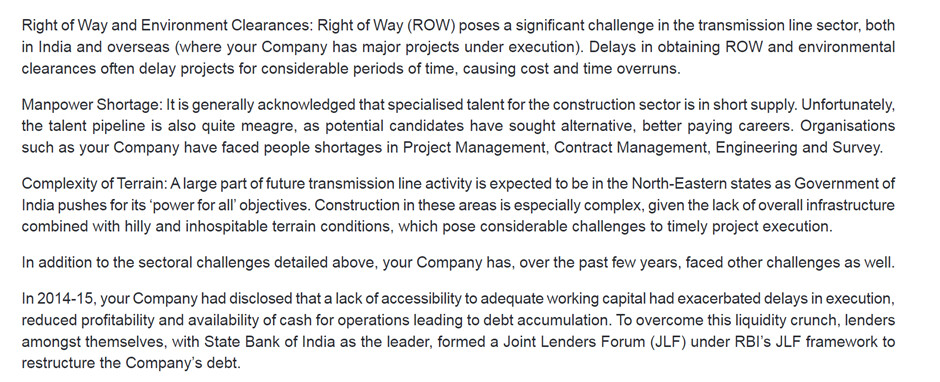

Challenge in getting approvals elongates working capital cycle and leads to delay in order execution-

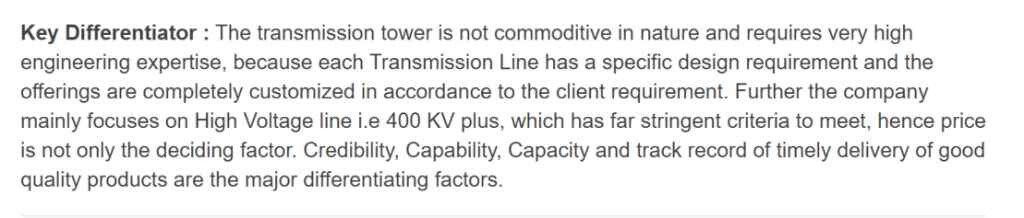

Source: Kalpataru Concall

So judging the company based on future order Book can be quite misleading as a slowdown in the economy leads to lower execution of those projects and thus operating deleverage causes massive drop in earnings. This phenomenon was evident post-2018 when a weakening economy impacted the company’s bottom line.

Margins:

As most of the order book is derived from government L1 bidding, the company faces an extended working capital cycle which further leads to increase in finance costs and reduction in profitability.

Historically Skipper has been able to achieve 15% EBIDTA margins vs its peer KEC achieving max 10.5% margins for their T&D segment.

Thus their bold claims of being the lowest cost producer globally has some merit.

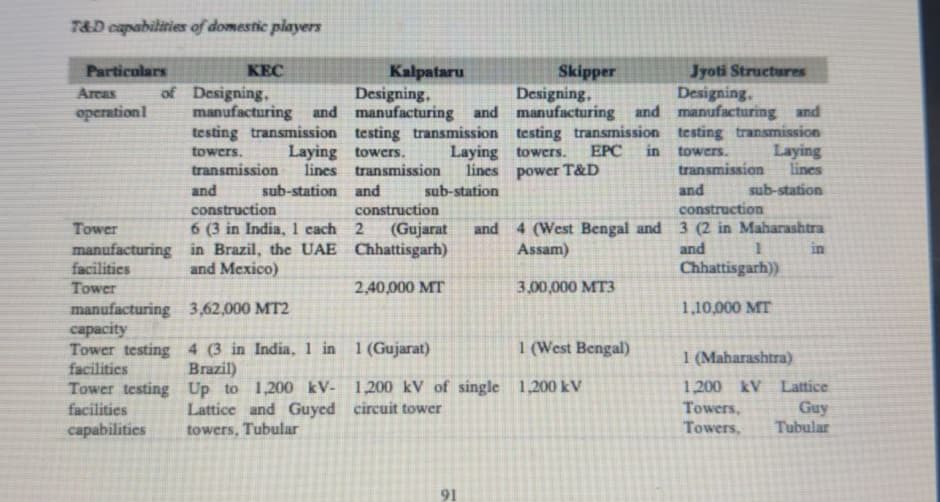

Competitive Analysis:

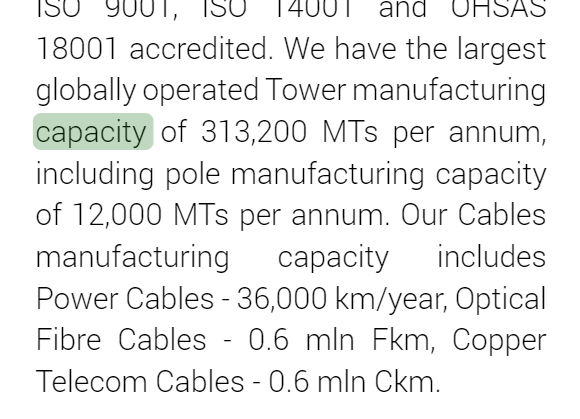

Currently KEC has the largest tower manufacturing capacity of 362000 MT which was 313200 MT in 2015.

Source: KEC 2015 AR

KEC International is a diversified EPC company with a strong presence in transmission tower manufacturing. However, due to lower returns on capital employed (ROCE) in this segment, its manufacturing capacity has expanded by only 15% in the past decade. As a result, KEC has shifted its focus towards EPC execution in the T&D sector, leveraging its strong execution capabilities to pursue complex projects globally.

Jyoti Structures has successfully restructured its debt through NCLT proceedings and is now focused on business turnaround.

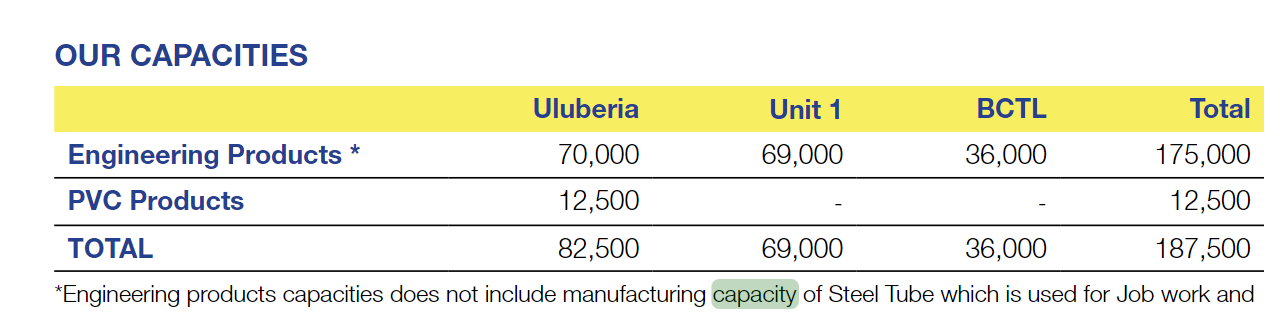

Kalpataru Projects had a manufacturing capacity of 180000MT in 2016, it has increased its capacity by 33% in 8 years.

Source: Kalpataru 2016 AR

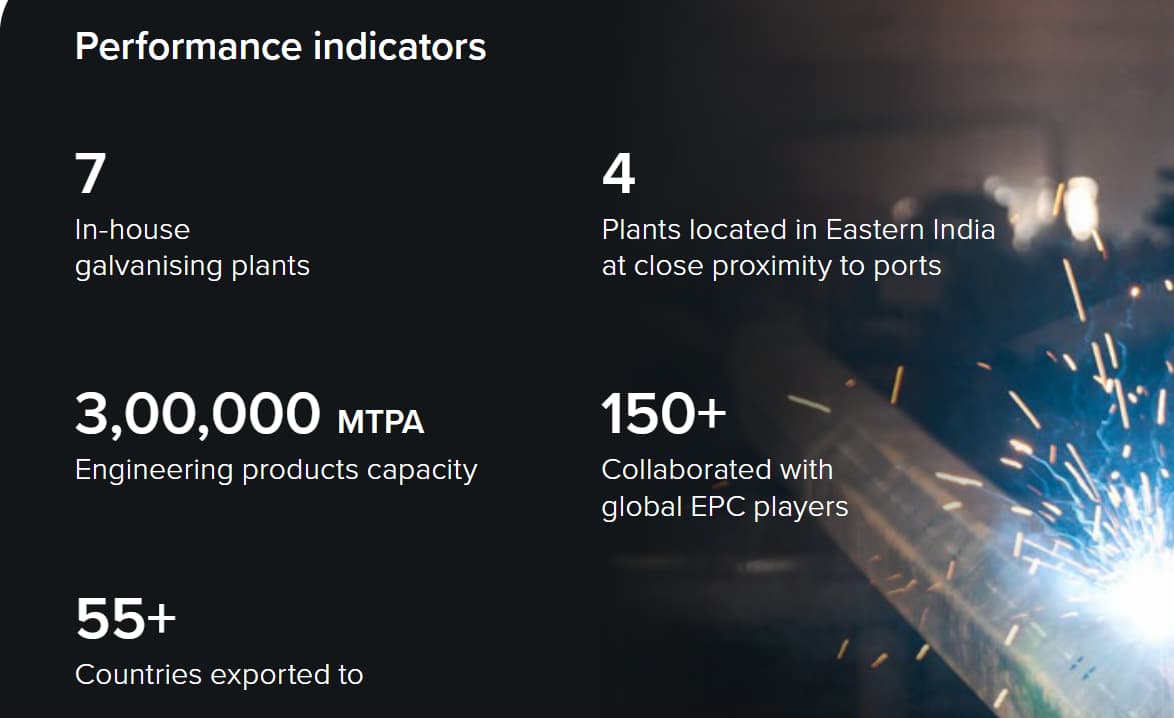

Skipper’s transmission tower manufacturing capacity has increased from 175000 MT to 300000 MT currently, thus a growth of 71% due to a focused business towards T&D which drives majority of its revenues.

Source: Skipper 2015 AR

While KEC and Kalpataru have diversified EPC portfolios, Skipper is a pure-play transmission tower manufacturer. The company’s claims of a geographical advantage and globally lowest cost production are reflected in its superior operating margins, as evidenced by its financial performance.

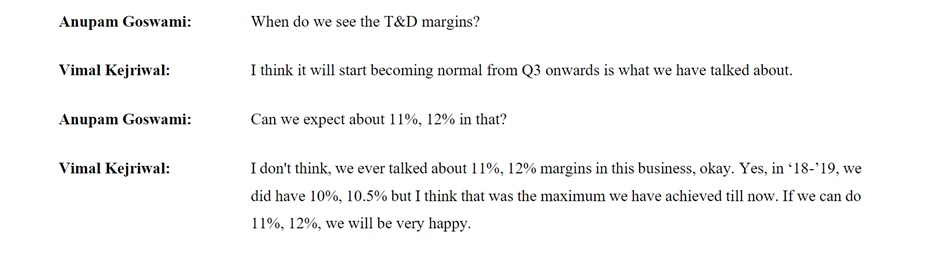

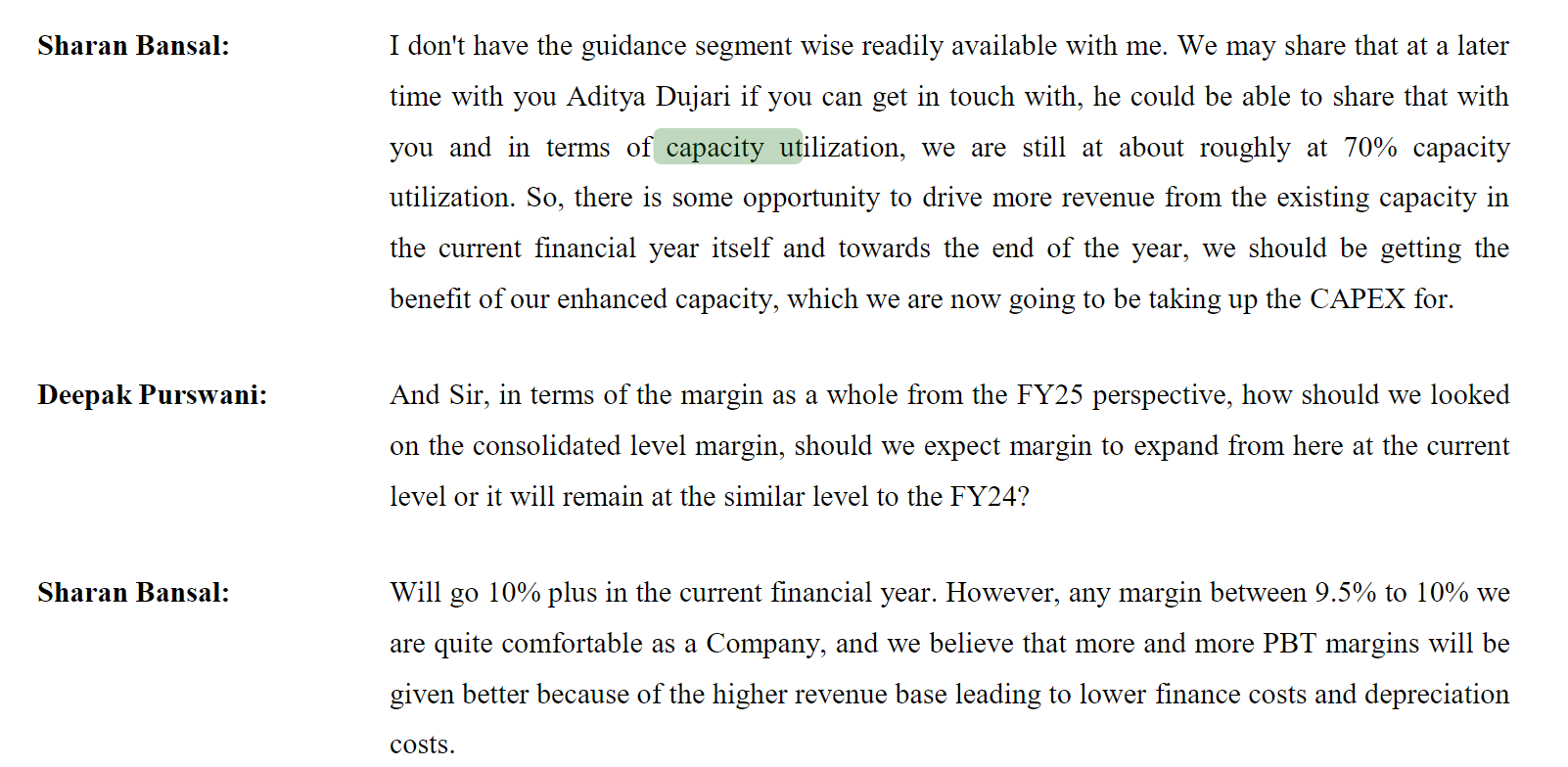

Currently they are operating at 70% capacity and thus can see higher operating margins due to operating leverage, which is evident in the past when it was earning 15% OPM in 2015-2018 operating at 90% capacity utilization. Thus I find management ‘s claim of margins being between 9.5%-10.5% conservative.

Source: Q4 FY24 Concall

High Finance Costs:

It is paying almost 50% of its OPM as finance costs which is very high, as compared to its total borrowings which is just 592 Cr vs finance cost 154 Cr, now many analysts have asked this question on concalls, but ig the reason for such high costs is because of high leverage and also if we see in such a consolidated industry we have seen that lenders in Jyoti structure had to take haircuts too which could be the reason they are raising 200Cr from Rights issue of which 150 Cr is yet to be called.

Maybe post 2018 as we have seen lenders cleaning bad debts from their Infra book be it IDFC First Bank or any other PSU bank. Due to the increasing non-performing assets (NPAs), banks became cautious in lending, making it difficult for infrastructure companies to secure financing. this could be a reason for reluctance to lend to this sector.

Key Strengths:

Source: East India Securities

Source: Skipper AR

Minimal raw material price fluctuation impact:

Source: Skipper Concall

Beneficiary of smart meter rollout:

Currently Skipper supplies transmission towers to EPC players or to Power Grid Corporation to India, which currently owns all the transmission assets and charges fees to local discoms such as MSEDCL for use of their infrastructure.

Smart meter implementation, by enhancing DISCOM financial performance through reduced losses and efficient billing, could potentially shorten Skipper’s cash conversion cycle.

Beneficiary of increase in renewable energy mix:

There has been a substantial increase in renewable energy capacity, often situated in remote locations distant from primary consumption centers. Transmission towers are essential infrastructure for transporting electricity from remote renewable energy sources to population centers.

Transmission towers are essential infrastructure for transporting electricity from remote renewable energy sources to population centers.

Valuations:

The company looks expensive optically at 50 P/E with 25% growth, (PEG=2, Considering no improvement in margins)

At EV/EBIDTA it is at 13x, we are currently seeing a massive capex in increasing our non renewable and renewable energy capacity, plus with the hike in telecom tariffs it is a key beneficiary of Telecom tower capex, also demerger of its Polymer business can be an optionality as well.

Being the lowest cost producer globally I am optimistic on margin expansion as the industry will not increase its capacity which would thus create a bottleneck for the massive capex being undertaken to increase production of electricity.

Risks:

If we look in the past risk has more to do with macro economic conditions of our country as in the past cycle also it had a massive order book but a slowdown in the economy impacted execution due to its dependency on government approvals.

Disclosure: Invested and biased

| Subscribe To Our Free Newsletter |