Comparison with ‘another large institution’ on just one parameter while conveniently ignoring their spectacular performance on all other is not fair either…

.

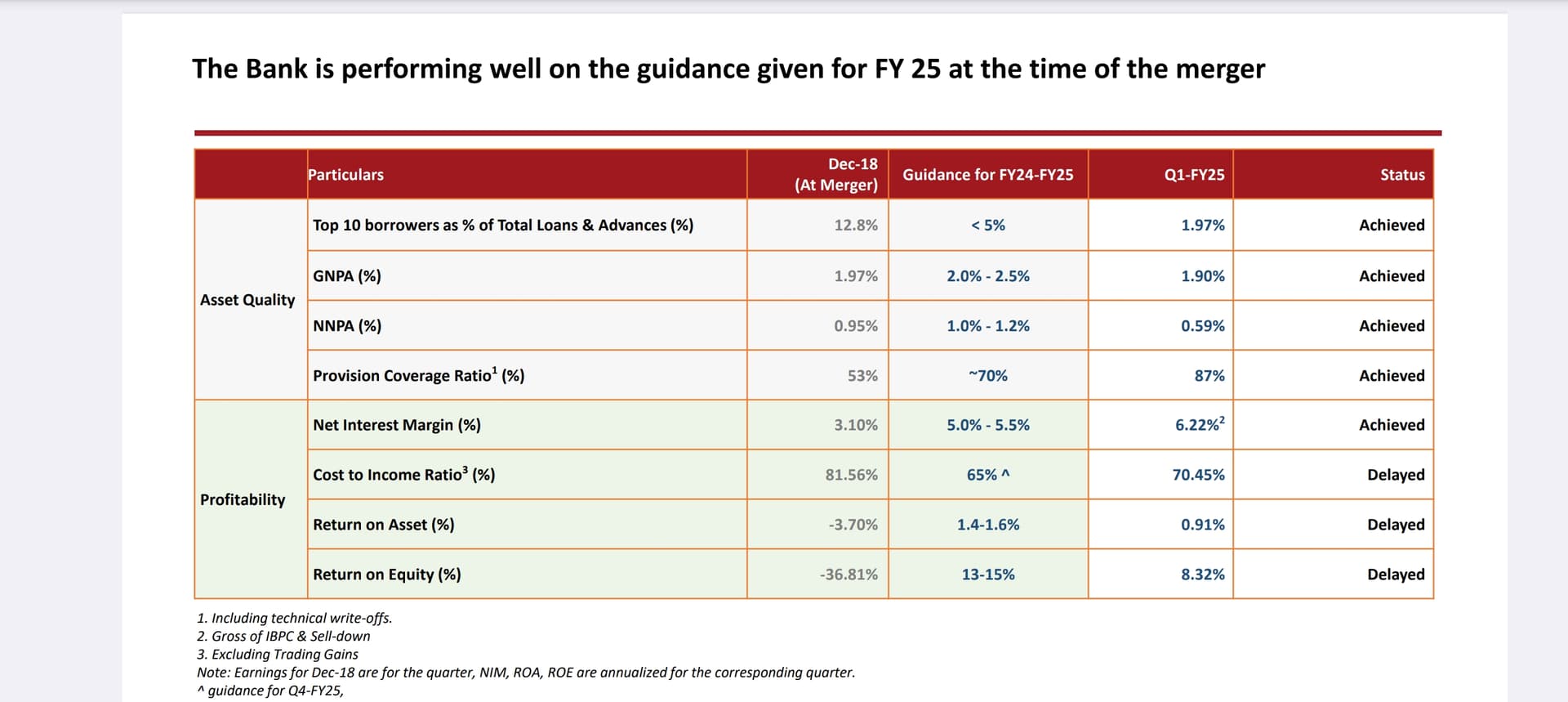

IDFC First’s performance may be great for clients and employees but shareholders have only suffered since merger…

.

They are no way near to their guidance of ROA, ROE and Cost to Income…probably the only 3 things which matter to shareholders.

Now they have started to sell new dreams…we should take it with truckload of salt.

For example, to achieve the now promised 1.4 ROA, profit needs to be around 7200 crores in 2027.

Is it possible when they are going to end 2025 around 3300…![]()

| Subscribe To Our Free Newsletter |