Few insights:

-

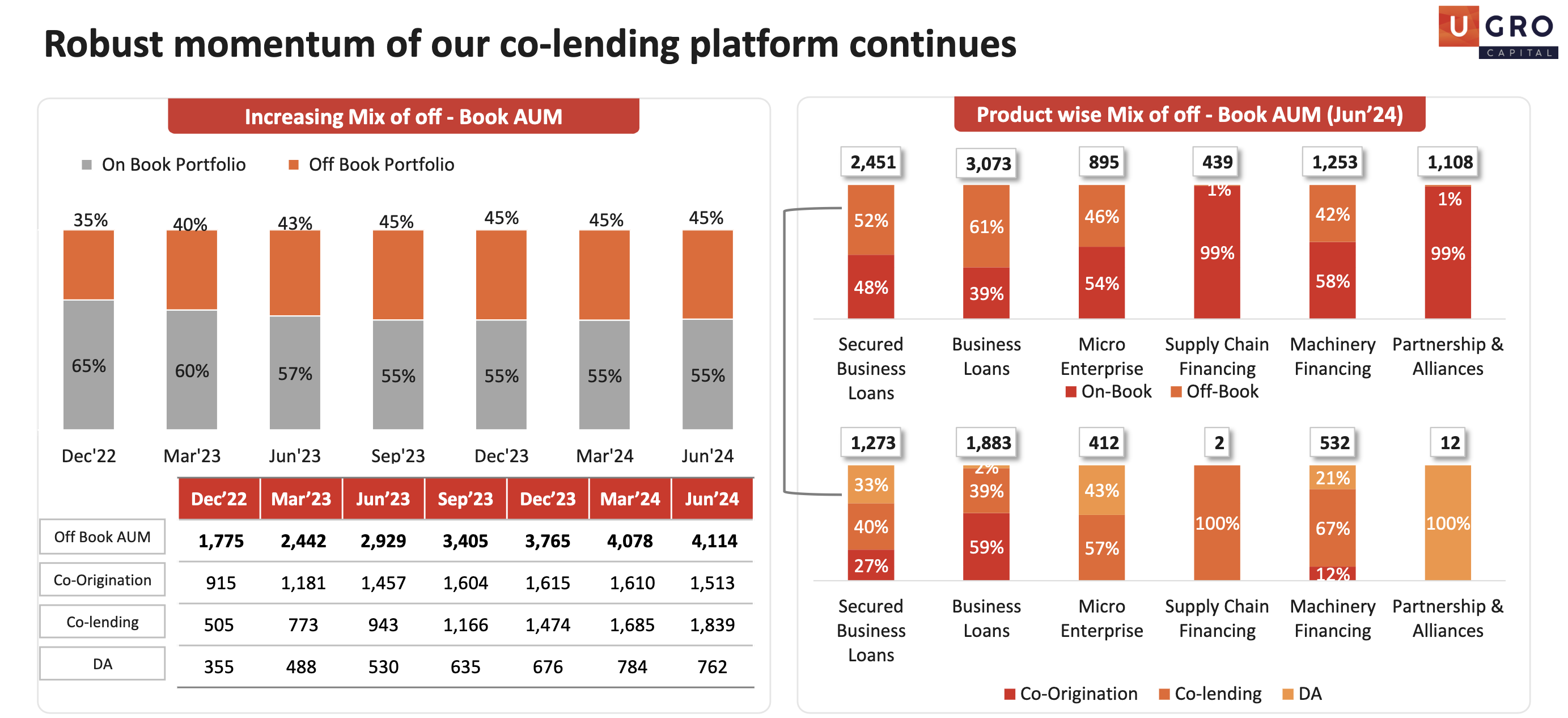

They are continuously increasing their co-lending book, got increased by 9% qoq. This is aligned with the long term objective of the management.

-

They are focusing on Secured and unsecured business loans for co-lending and using their balance sheet to ramp-up Micro enterprise loans. This way they will earn a good fees from banks for co-lending and high spreads from Micro enterprise loans. Good proposition for Ugro.

Question(refer the screenshot below):

-

What is co-origination, is it same as co-lending and why it got decreased?

-

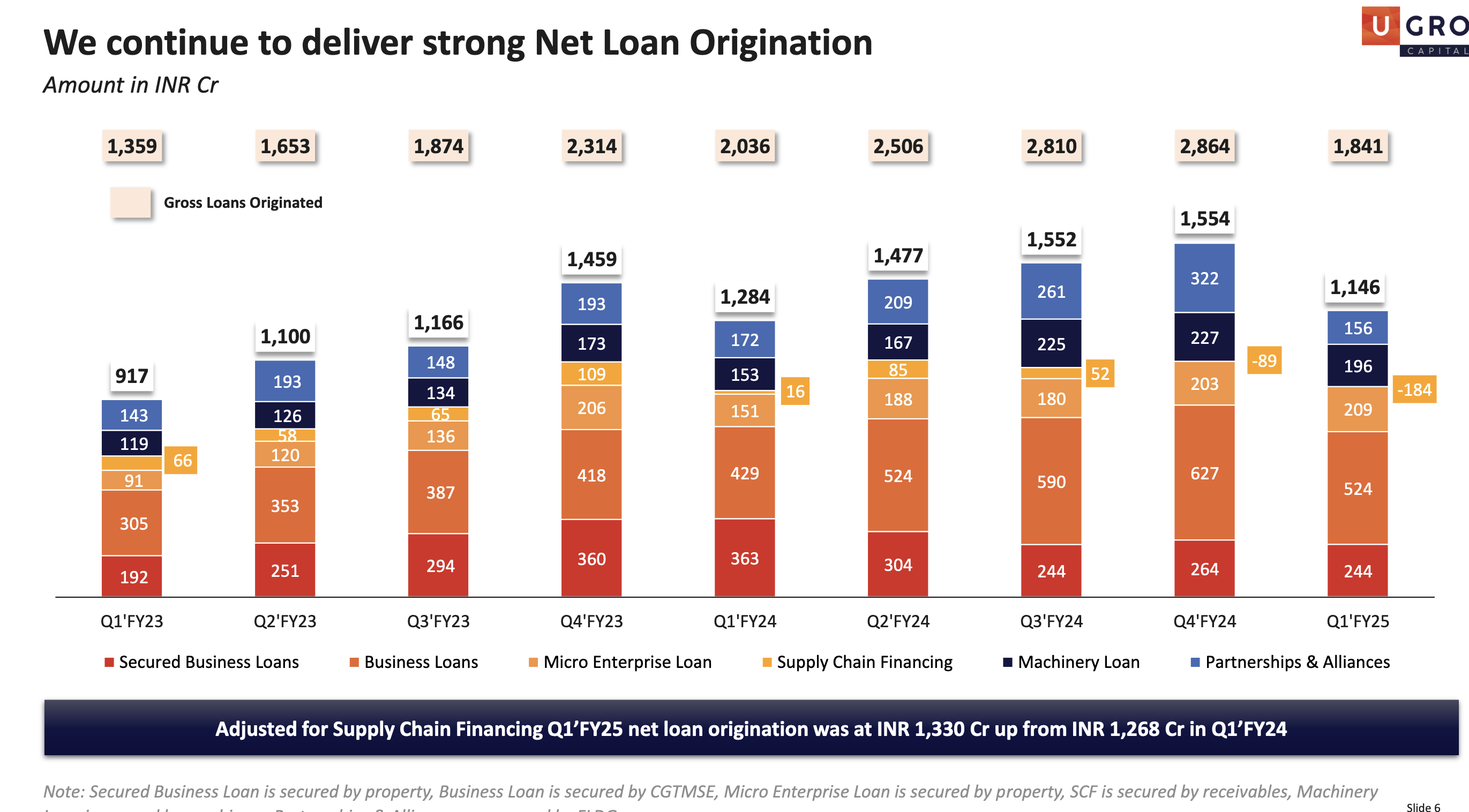

Why over all net loan origination is muted in the quarter for all the buckets(only micro enterprise loan-book increased minimally), need some clarity here?

| Subscribe To Our Free Newsletter |