Date: July 2024

Business Model:

EFC (I) Ltd operates in the flexible office space sector, providing co-working spaces, managed offices, and turnkey project solutions. The company offers end-to-end services including leasing, interior design, and furniture manufacturing through its subsidiaries Whitehills Design Ltd and Ek Design Industries Ltd. EFC is also expanding into REIT and AIF initiatives to control and operate real estate assets more efficiently.

Industry Thesis

The flexible workspace market in India is experiencing rapid growth driven by increasing demand from startups, SMEs, and MNCs. This sector is projected to grow at a CAGR of 15%, offering significant opportunities for companies like EFC that can provide comprehensive, cost-effective, and customizable office solutions.

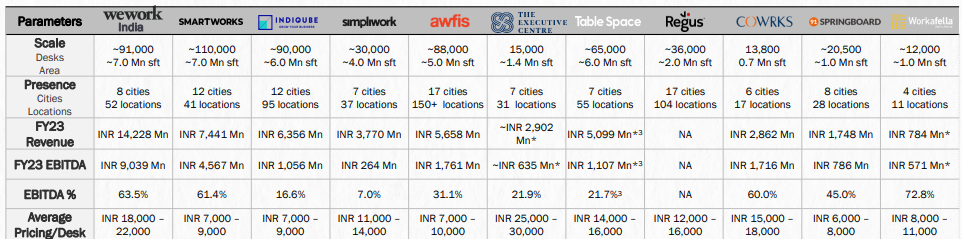

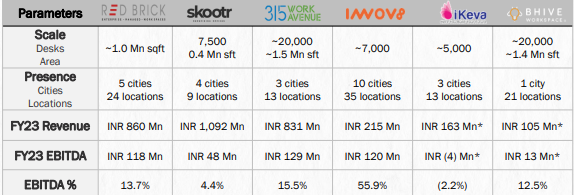

Competition pairing:

Note: EFC revenue is from FY24 (not FY23)

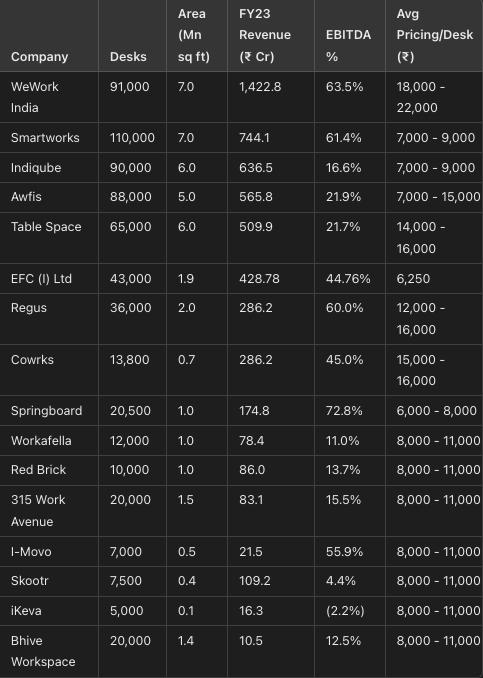

Industry Summary:

- Total Desks: 738,800

- Total Area: 42.4 million sq ft

- Total Revenue: ₹5,459 crore

- Total EBITDA: ₹2,554 crore

EFC’s Absolute Values:

- Desks: 43,000

- Area: 1.9 million sq ft

- Revenue: ₹428. crore

- EBITDA: ₹191 crore

EFC’s Market Share wrt:

- Desks: 5.82%

- Area: 4.48%

- Revenue: 7.85% (8% market share)

- EBITDA: 7.51%

EFC (I) Ltd has a substantial presence in terms of revenue and EBITDA relative to the total, despite having a smaller scale in terms of desks and area. This indicates strong operational efficiency and a competitive position in the market.

Primary Industry Drivers

1. Rising Demand for Flexibility: Increasing need for flexible office solutions post-pandemic.

2. Economic Growth: Expansion of businesses and entry of global companies into India.

3. Cost Efficiency: Flex spaces offer cost savings compared to traditional office leases.

4. Urbanization: Growth in urban centers driving demand for commercial real estate.

Primary Investment Rationale

1. Strong Financial Performance: Significant revenue and profit growth in FY2024.

2. Scalability: Ambitious expansion plans to double seat capacity by 2026.

3. Diversified Revenue Streams: Integration of REIT, AIF, and furniture manufacturing.

4. High Occupancy Rates: Consistently maintaining over 90% occupancy.

5. Cost Efficiency: Economies of scale and in-house capabilities reduce costs.

What I Like About the Business

1. Integrated Operations: End-to-end solutions reduce dependency on third parties.

2. High-Margin Segments: Expansion into furniture manufacturing with high EBITDA margins.

3. Strategic Client Base: Long-term contracts with large enterprise clients.

4. Growth Potential: Positioned well to capture the growing demand in the flex workspace sector.

What I Don’t Like About the Business

1. High Capital Expenditure: Significant upfront investment required for expansion.

2. Market Competition: Intense competition from established players like WeWork and Awfis.

3. Debt Levels: Potential risk from high debt used to fund growth and REIT initiatives.

Trackable Growth Drivers

1. Seat Capacity Expansion: Doubling seats to 92,000 by 2026.

2. Furniture Manufacturing Launch: Expected revenue of ₹300-400 crore annually.

3. REIT and AIF Initiatives: Additional revenue from managing real estate assets.

4. New Leased Spaces: Adding 400,000 sq. ft. in major urban centres.

Risk Factors

1. Market Competition: Price wars and reduced margins.

2. Economic Downturns: Impact on demand and occupancy rates.

3. Operational Risks: Project delays and quality control issues.

4. Regulatory Changes: Compliance costs and restrictions on operations.

5. Technological Disruptions: Adoption of remote work reduces demand for physical spaces.

Valuation Expectations (July 2024)

The company looks favourable from the forward multiple (although would have liked MoS at current levels i.e. P/E less than 30). Currently, the company trades at 45x P/E with an expected EPS growth of min. 30% YoY

| Subscribe To Our Free Newsletter |