Edel declared Q1 result today.

My 2 cents:

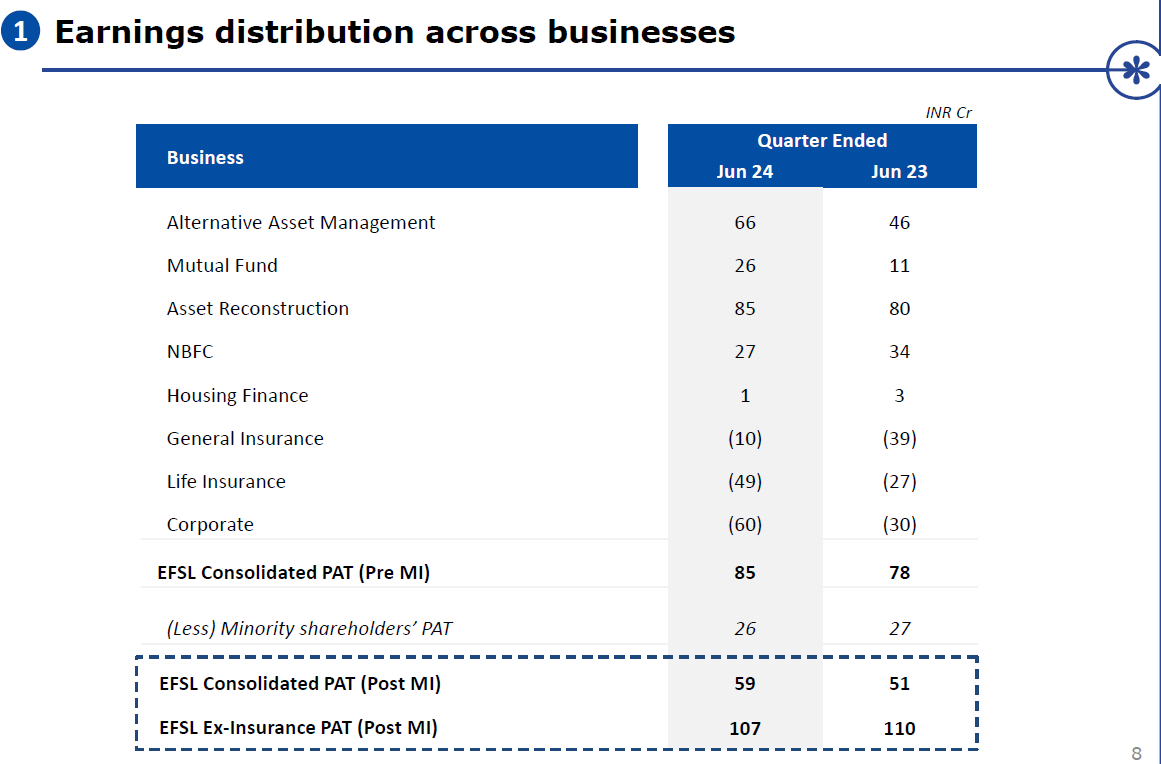

At the current rate, AIF annualised PAT is around 250 cr. However, as the rate is accelerating, it could be 28-300 cr PAT just for AIF.

The mutual fund business is also taking off, with the best PAT ever of 26cr. Their SIP portfolio is growing at a good rate, and they are getting more equity MF. This could be 80/100 PAT for Fy25.

They are setting off AIA spin-off again. I think they should distribute the shareholders the same way they did for Nuvam instead of IPO. In the case of IPO), Edelweiss may get money, but as a shareholder, I want money to be in my hand and not in the hands of management (as they have made a lot of capital misallocation in the past). The Nuvama spin-off was rewarding. I hope AIF/MF follows in line.

AIA profit (AIF +_MF) at annualised rate is 300+ in Fy25. Assuming 20/25 PE, that business is worth around (6,000 to 7,500 cr) at today’s price, which is Edelweiss’s market cap at CMP.

Wholesale reduction of 200cr is on target, less than planned thought. I think this is a sticking point. If wholesale is to be removed from their business, Edelweiss will be quoted at multiple times the current price. But it is not likely to happen. Most of the pending Wholesale must be hard to get rid of , so time is the medicine here. They want to reduce to 1250 cr in June 2026, which is eight quarters away. From 3900 to 1250 (reduction of 2650 cr) in 8 quarters equates to a reduction of 325cr per quarter. They are nowhere near that rate in the last 6 months, so current projects look optimistic at the moment.

General insurance losses are reducing further. Hopefully they keep the momentum. Life insurance is not showing sign if getting better. Hopefully from Fy26 onwards their looses reduce (long if).

Nuvama has declared a dividend of Rs 81 per share, for a total of 289 cr. Edel owns around 14%, which means they will be getting 40cr of dividends in Q2, which will be handy. Additionally, this dividend will be a regular affair going forward.

Note: Long term invested

| Subscribe To Our Free Newsletter |