Vaibhav Global Q1 FY25 Concall notes (posting only key takeaways from my POV)

-

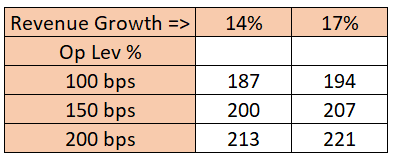

Maintains guidance for 14-17% revenue growth in FY25. The range is due to uncertainties due to US elections, else they’d have been confident guiding for 17%

-

Content and broadcasting cost was 20% of topline in Q1, expects to finish the year at 18% of topline. This is a 1.5% YoY growth for the line item. Investments here being made for ramping up their newly acquired online businesses of Ideal World and Mindful Souls as well as the new territory of Germany. They have also spent some amount in improving TV positioning in USA. This line item as % topline has increased from 12.5% in FY20 to around 18% in FY25E. One hopes that a lot of this is leverage and the ratio was settle below 15% once the new businesses reach steady-state. Looks like they are targeting higher growth (mid teens guidance for medium term) via higher investments in content and broadcasting with some leverage.

-

Overall expect to deliver 150-200bps of operating leverage in FY25. Expects 200bps GM expansion due to better product mix, 100bps expansion from employee costs line item and possibly another 50bps from other line items such as travel expenses and freight. There will be a 150bps negative leverage due to B&C costs as discussed above, so net/net there’s a possibility of 150-200bps EBITDAM expansion YoY

If management indeed is able to deliver 15% revenue growth and 200bps EBITDAM improvement over the year, PAT here can comfortably cross 200Cr. Here’s how I see PAT playing out for various combinations of growth and leverage. I have assumed 20cr Other Income and 25% tax rate.

Depending on which scenario plays out, there could be a 50-75% YoY PAT growth and the stock is likely trading between 24-29x FY25 PAT. If the upper end of the PAT assumptions plays out, I won’t be surprised to see the stock trading at 8000Cr MCap.

Chart wise, 273 seems like a strong support zone. I don’t expect the stock to test that support unless there is panic about a US recession. From what I know, recessionary conditions on ground normally top out well before a recession officially shows up in GDP nos. So the worst in terms of consumer sentiment for the business may actually be behind them and that seems to be what management is also indicating. However, Western economies aren’t in the best of health and adverse risks remain which need to be monitored.

Disc: Invested.

| Subscribe To Our Free Newsletter |