Concall Transcript is now out. Here are my notes.

In terms of business, the concall was very assuring and many of my concerns have been allayed.

Management Guidance

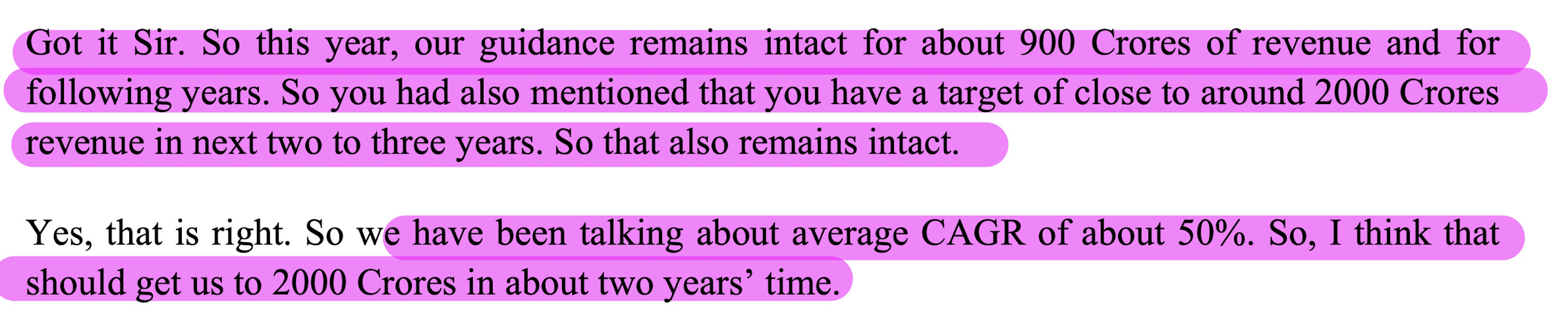

900 cr revenue for FY2025

~35% EBITDA Margin and ~25% PAT margin

Don’t look at Quarters but the whole year as product mix may change and execution could be lumpy

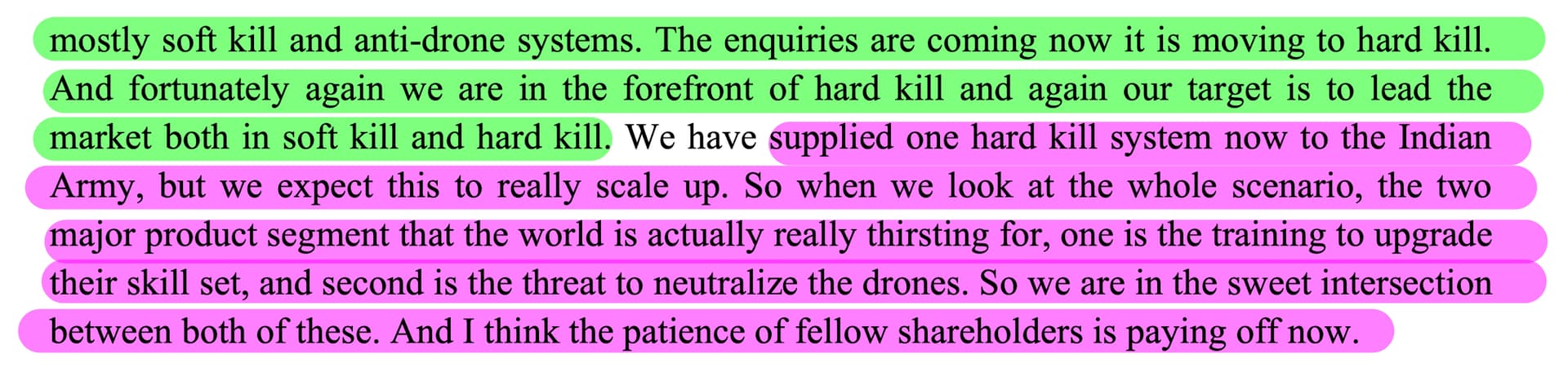

Have healthy enquiries for both their businesses i.e. Simulators and Anti Drone

Have launched new products. Market size for these products is in 1000s of crores however detailed study required to know the market size. There will be more announcements in this area.

New Orders will come predominately in Q4.

Simulators

15000 cr is the opportunity size

High margin segment with ~40% EBITDA

What drives this segment?? – Huge cost savings, reduces downtime etc.

Simulator induction is at nascent stage + new platforms will require simulators

Anti drone

Demand to be revised upwards from 10,000 cr

EBITDA margin in this segment ~30%

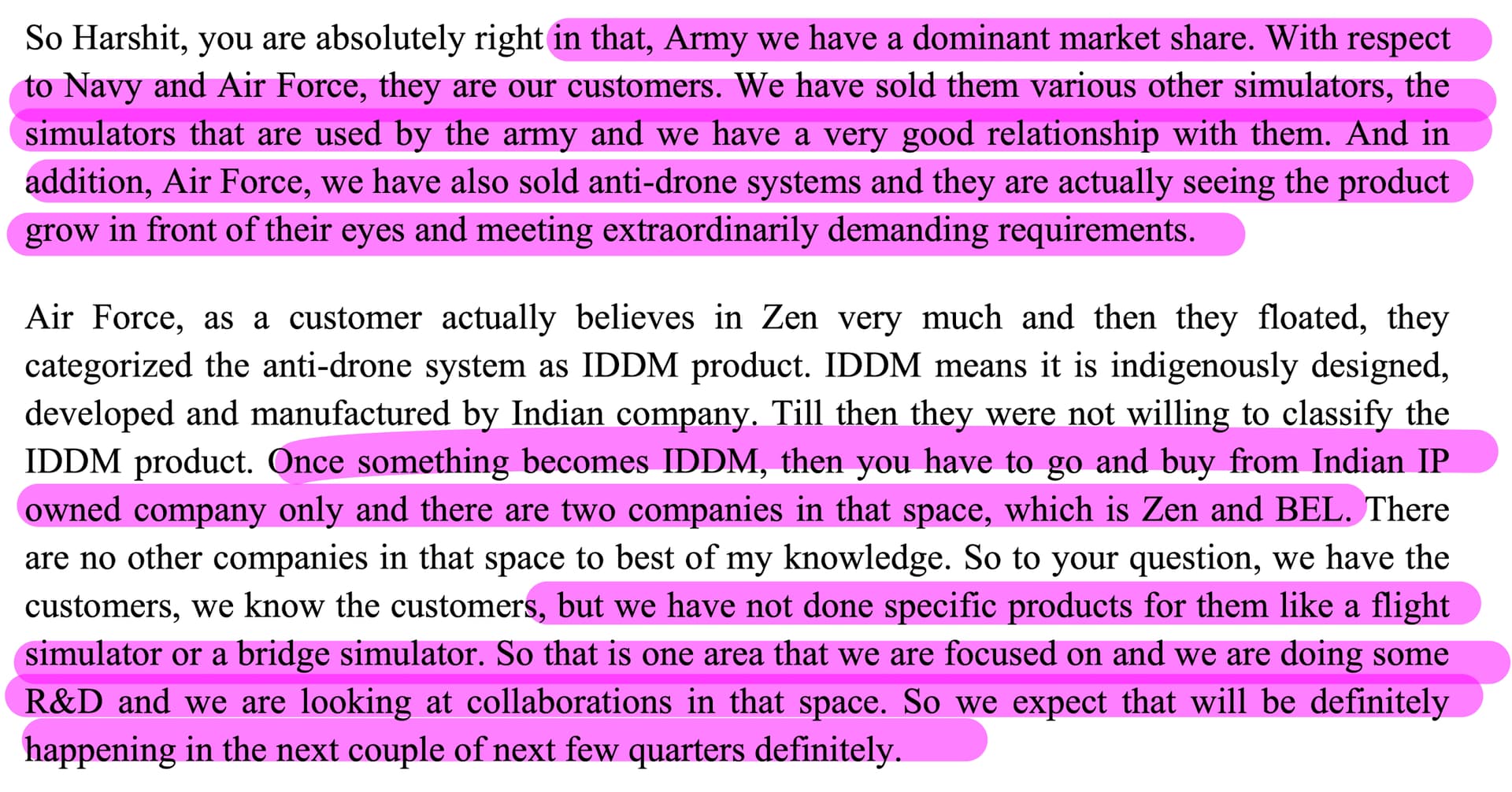

ADS are in IDDM list. Only other player is BEL

QIP

Enabling resolution – not raised funds yet

Looking for inorganic opportunity

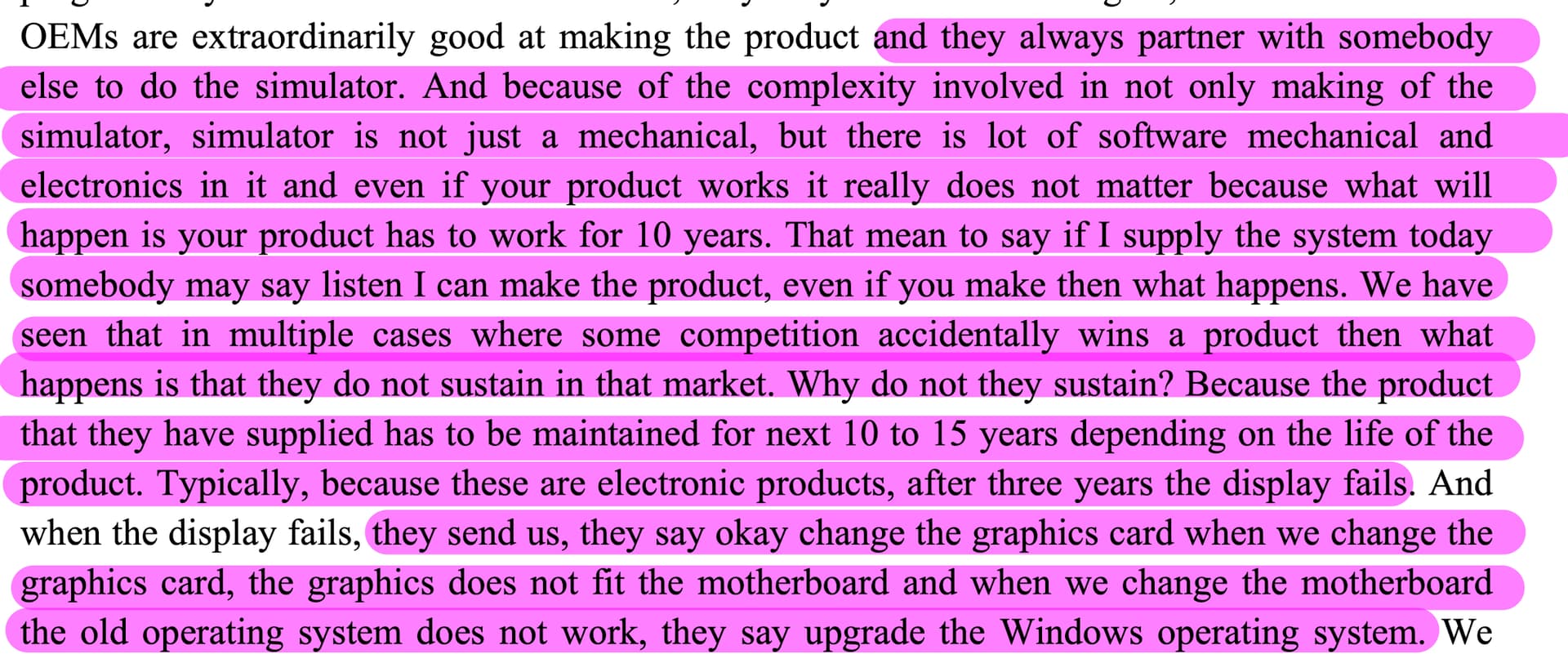

Why AMC matter and why simulators are not done by OEMs themselves

50% CAGR is this sustainable?

My take:

In the overall scheme of things the company is still a 15000 cr market cap company. They are growing rapidly and things like growth in simulators and ADS makes sense.

Simulators you need to train – it is an effective way to train and given the nature of modern-day warfare are crucial components.

Key Monitorable from Concall: Order wins by Q4, execution in between and new products

Disl – Invested and biased

| Subscribe To Our Free Newsletter |