My key take aways from the management conf call:

-

Quarter numbers are lower because of:

a. account of increased competition,

b. lower raw material prices, and

c. some dumping from Chinese manufacturers in certain segments. <did not elaborate which segment specifically it is impacting. This anyways is a time-consuming process, and no quick turnaround is possible. Roughly above 3 were equally weighted impact wise per management.>

d. Preventative maintenance shut down, led to not executing on some high value orders.

Lower RM cost, led to inventory devaluation, which will be nullified once we fulfill the orders that were supposed to be dispatched in the Qtr gone by. -

Telangana Unit:

a. The Telangana finishing line was expected to be completed by March 2025. But, I don’t think that will happen, in all probability it will be deferred by at least 9 months, because we have recently placed order for some equipment, those orders have been finalized, purchase order has been issued. However, the gestation period for that order is 12 months. So, reasonably speaking, the Telangana unit expansion should get completed by December 2025. -

Hot mill upgrade will only happen once the Telangana finishing line is in place because we will have a loss of production whenever we take the hot mill upgrade. So, in order to compensate that loss, we need the Telangana unit to be active in full capacity. The sense which I am getting from your question is, when will volume growth come in? So, I don’t think there will be any volume growth in FY25. And in FY26, volume growth will only happen once the Telangana finishing line has been completed and is open for commercial production.

-

We don’t export to the Middle East, exports have not revived, exports have been slow for more than a year. Market size in US and Canada is very big, but they have not revived for us.

-

EBITDA per tonne fell from Rs.22,000 a tonne to Rs.9,000 per tonne!!

-

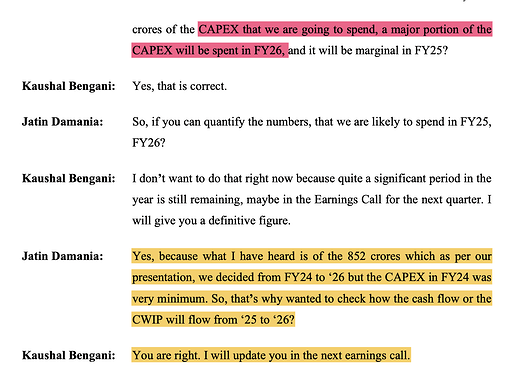

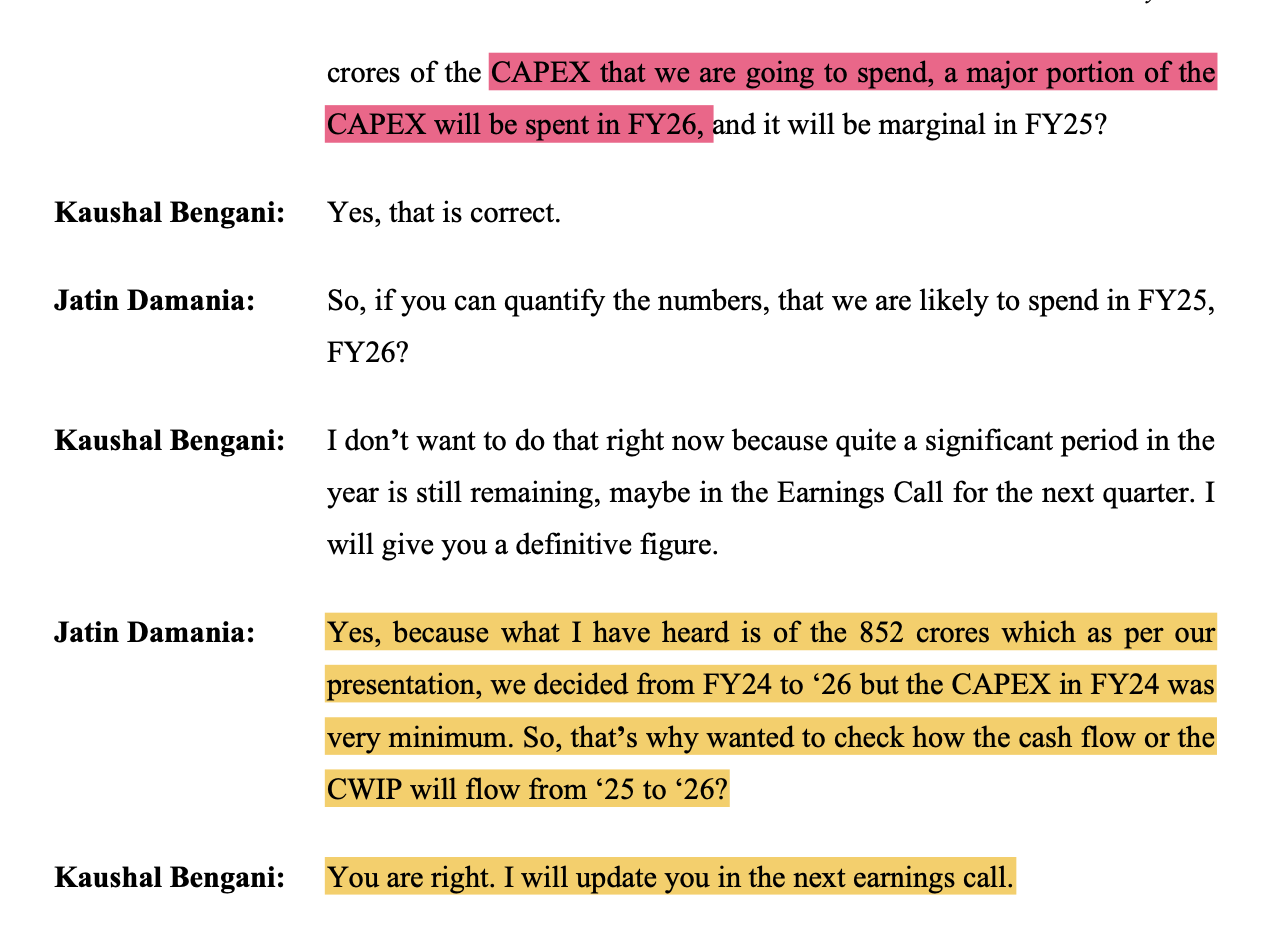

Capex:

The announced ~850 cr would be mostly spent only in FY26.

Although there might be a quick reversal once the high values get shipped and the RM prices adjusted and might show profit and bump in margins, the Capex has been delayed to FY26. So, its wait and watch for me in this counter.

Disc: Not invested.

| Subscribe To Our Free Newsletter |