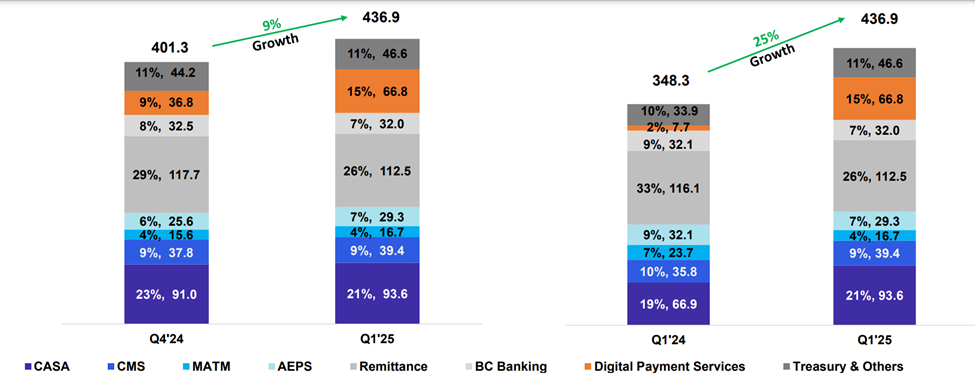

Revenue share as of Q1 25

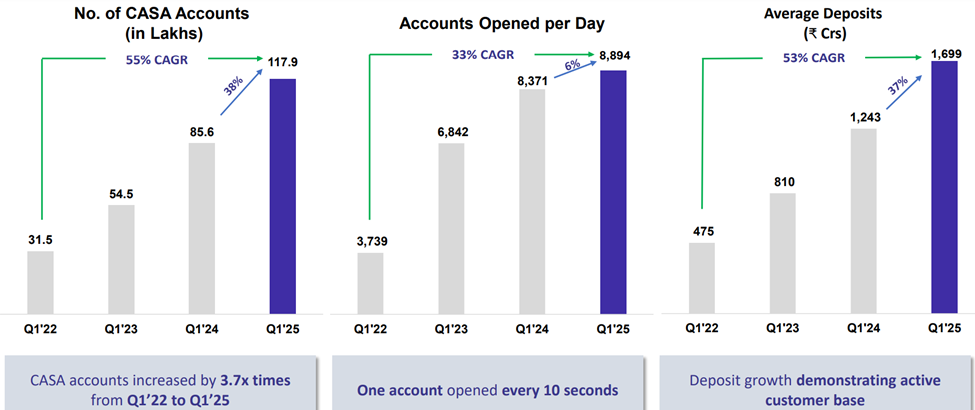

Fino has been able to build a great liability franchise over the years.

Treasury income has grown 5 % QoQ and 37% YoY aided by deposit growth and a favourable interest environment.

It’s good to see a slowdown in degrowth in some of the legacy/hook products. After a long time, MATM grew from 15.6 crores to 16.7 crores and AEPS grew from 25.6 to 29.3 crores on a QoQ basis. Even BC banking had only a marginal de- growth.

Sequential growth in CASA and CMS continues

Of the INR 66.8 crores in digital revenue, around, INR 64 crores is from the B2B kind of business where they have 19 partners, and Fino provides them online UPI platform for facilitating their business, both on the collections as well as the payment.

In addition to that, there are some MEITY incentives and interchange fees.

It is through partnerships wherein Fino platform facilitates financial transactions online for businesses. This model helps to leverage the platform, which was created over the past 2 years on setting up a simplified digital stack with an in-house UPI switch for the business partners.

The biggest advantage for Fino would be its cost of funds when it eventually gets converted to an SFB. As per the previous concall, they informed that their cost of funds was 2.1 % which is great. They have already converted a cost center(liability side) for most SFBs into a profit center.

Digital expenses have remained high and may not go down any soon. Fino is in the process of migrating to Finacle.

Source: Investor presentation and Concall transcript

| Subscribe To Our Free Newsletter |