Sharing my view on the Quarterly results in the coming qtr. Hopefully this is useful. It is conservative however, happy to upward revise the same once i see demonstration of execution and margins!

https://x.com/DagaVish/status/1820894207680323611

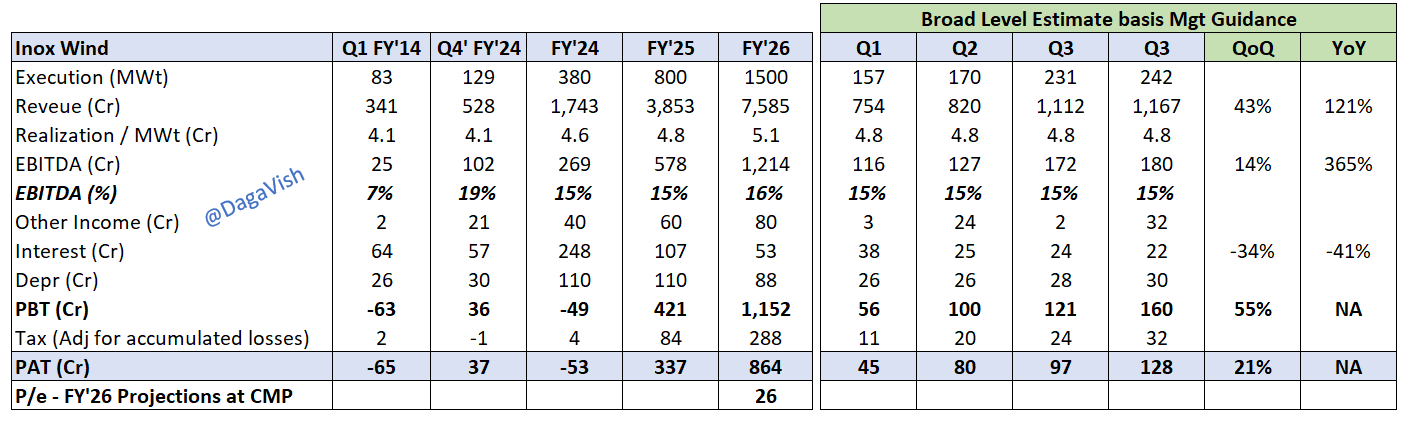

have taken a stab at projecting Q1 FY’25 basis management guidance for the year + historical data points…

Topline – Expecting a ~120% YoY growth & 40-45% QoQ growth upon execution of 157 Mw @ a realization of ~4.8 rs. / Mw

Assuming stable margins of ~15% – EBITDA growth is 4.6x YoY / +365% with a QoQ improvement of ~14%

They have repaid debt to a great extent which can reduce Interest cost YoY by 40% odd

PAT would be at ~45-50 Cr vs. loss of 65 Cr YoY with a QoQ jump of ~20% !

Would be interesting to see Management walk the talk. Technically stock has seen good accumulation in the recent weeks running up to the earnings post being in a range of 130-170 for quite some time.

Disc – Invested. DYOR – Not an Investment advise

| Subscribe To Our Free Newsletter |