We can estimate that also, dominos (jubilant foodworks) has sales growth of 13% per annum (taken average of last 10 years), you can see that in screener.in, similary cafe coffee day has negative sales growth of -7% for same period, for barbique nation its 11% per year taken average for 5 years.

Lets assume zomato also has excellent management team as that of dominos and give them 13% sales growth then also the valuation of 2.5 lac crore is nowhere to be seen.

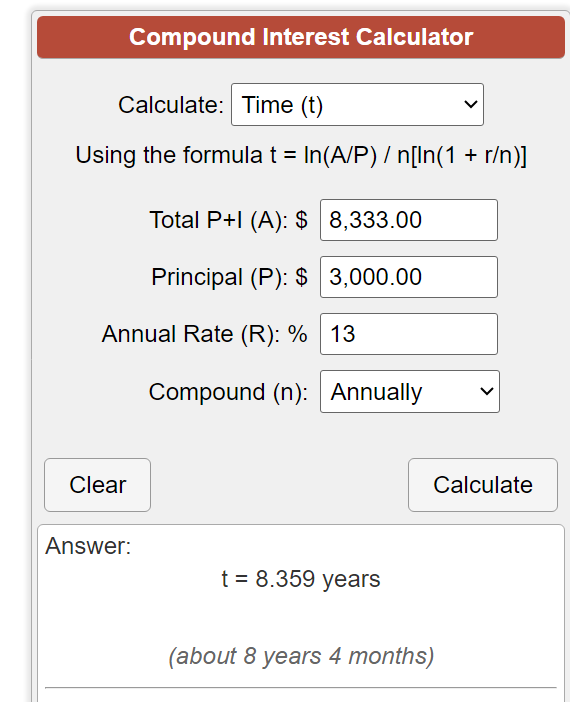

According to my estimates (I have estimated the current valuation of zomato, not the future, assuming if it had tapped the whole market) zomato’s valuation is 90k Crores assuming blinkit doesn’t incur any losses. That too when zomato had tapped the whole market. Zomato doesn’t even have 3000Cr profit today and its valuation is already 2.5lac Cr. For 30 PE ratio it needs profit of 8333.33 Cr profit, that is even more than market potential of 3000 Cr today. It will take 8 years 4 months for market potential to become 8333Cr at 13% sales growth.

And god knows how many years it will take more to tap the whole market potential itself. Overall, I don’t see zomato crossing 2.5lac Cr valuation in next 10 years with PE ratio of 30.

| Subscribe To Our Free Newsletter |