What’s your antithesis?

-

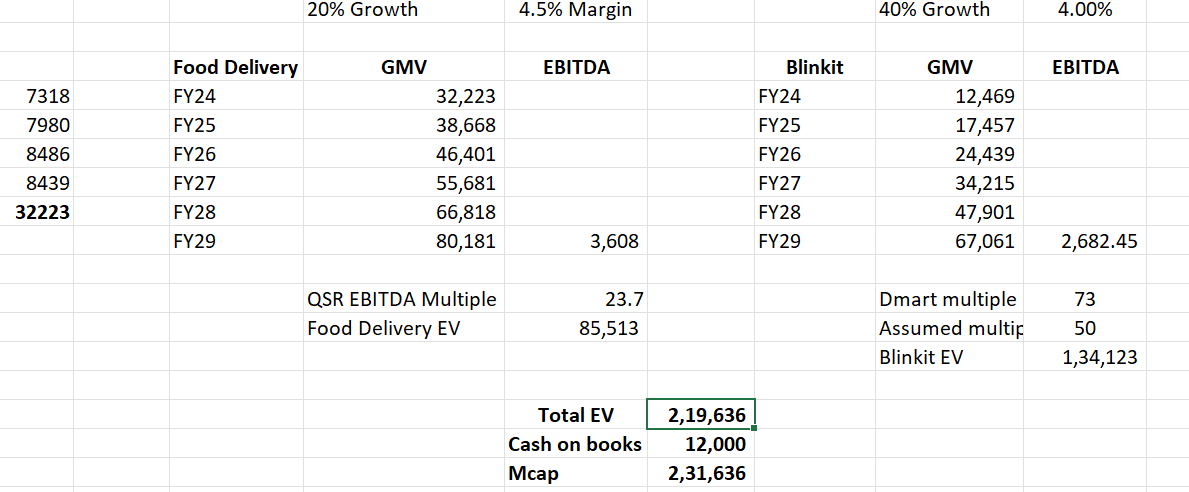

Food delivery won’t grow @ 20% YoY for next 5 years? We are in a subdued macro consumption environment right now. PFCE has been growing at 4-6% for last 4-6 quarters. Zomato is doing 25% growth in that environment. Imagine once RBI starts cutting rates?

-

Blinkit won’t grow @ 40% YoY? Its growing at 80%+ right now and taking away share from other channels (MT and E-Com) in key categories – groceries, consumer staples, and BPC goods. Speak with any category manner for traditional e-com or MT and they’ll tell you.

Levers that Blinkit has to accelerate growth – category expansion & geo expansion. There is enough headroom to grow. And they’re growing while their existing network of dark stores increases throughput (see the trend of GMV per store trending up from 620k in Q1FY24 to 956k in Q1FY25).

On top of it you have the joker – 12k crs cash which they can deploy to acquire EPS accretive businesses. Paytm live event deals that Zomato is in discussions with.

So, I’m curious what’s the core antithesis?

EDIT – Mindyou, Blinkit is likely to 67k crs of EBITDA in FY27 itself as per me. So there’s a lot of upside still left.

| Subscribe To Our Free Newsletter |