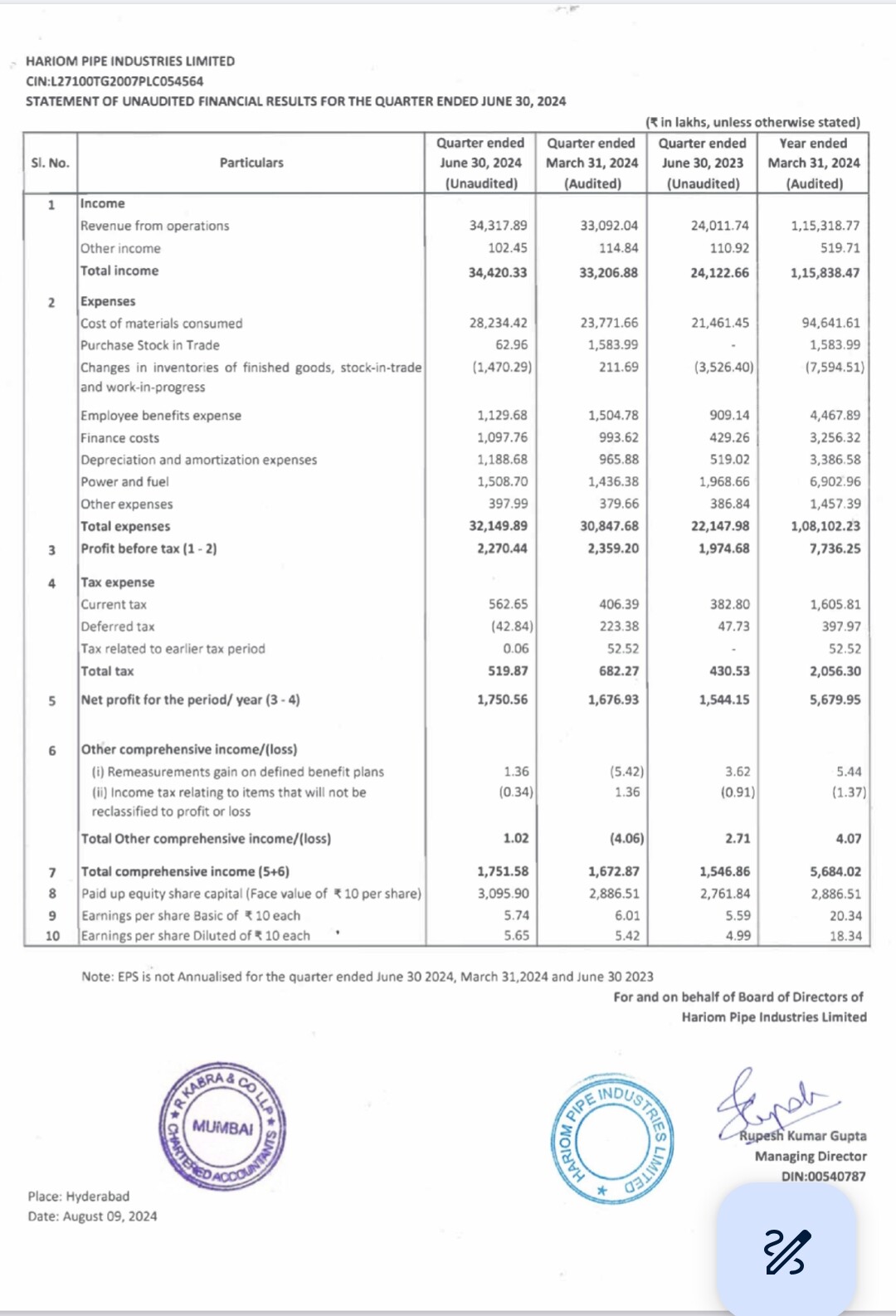

Hariom Pipe Results

Very Good Results beyond my expectations ![]()

Revenue up 43% YoY n Flat QoQ

EBITDA up 59% YoY n 6% QoQ

EBITDA margin at 13% vs 12% YoY n 12.6% QoQ

PAT up 13% YoY n 4% QoQ

Finance cost up

Operating Leverage now comes in Play (QoQ momentum started)

Overall very good set… Q1 is weak for sector and then too it has beaten Q4…

Might be Revenue expectations were high from market but Hariom has clearly beaten on Margin side

Now onwards Q1 < Q2 < Q3 < Q4

Based on guidance FY25 Revenue would be 1650-1750 Cr

Q1: 343 Cr

Left: 1300-1350 Cr

If Revenue would be around 375 Cr than it would be real beat… but still track this number whether they would able to achieve this or not

Debt free target till FY27

No Reco

| Subscribe To Our Free Newsletter |