I looked at the financial statements filed by the company so far and its IPO RHP, and was not convinced about the quality of reporting. Highlighting some of the issues I found:

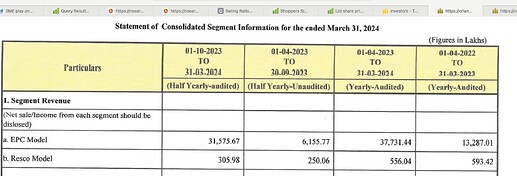

- As per the RHP, the company reported a standalone revenue of Rs. 133 Cr in FY2023, out of which, Rs. 50.6 Cr came from EPC work carried out for subsidiary SPV companies. The consolidated revenue for the same year was reported to be Rs. 136 Cr. This would imply that the subsidiaries earned revenue of 136 – (133 – 50.6) = 53.6 Cr during the year. However, if you aggregate the individual revenue figures of subsidiary companies (mentioned in RHP), you arrive at subsidiary sales of Rs. 5-6 Cr. This is also corroborated by the segmental break up of revenue reported as part of FY2024 financial report.

For me, this raises a lot of questions on the overall reliability of the financials being reported by the company.

- The other part is the RESCO business itself. It has hardly been generating any revenue. I understand that many of the projects are still under construction. But, if one goes by the fixed asset schedule in the consolidated balance sheet over the last two years, it is clear that a significant value of capex has been commissioned and therefore included in PPE and not CWIP.

Assuming most of the fixed assets belong to the RESCO business (which is a reasonable assumption, since there are no fixed assets on the standalone balance sheet), the revenue generated by the segment seems suboptimal. The ROCE of the segment looks poorer.

- Coming to the recent announcement related to the electrolyser business, I could not find any information regarding the contours of the project. I tried to gather some information on the project-partner Splitwaters, but couldn’t really find anything that could establish their ability to set up a manufacturing capacity of 1 GW. Splitwater itself seems to be small scale player.

Further, I really wonder if it is a wise idea to go after a new line of business before the company has established itself in the current one, especially with regards to the RESCO business.

Like many other investors in the current market, I was excited about the prospects of the company, given the many sectoral tailwinds, impressive growth shown by the company and reputed names in its order book/client list. But, having gone through the available data deeply, it seems a lot of questions need to be answered before one can take an informed decision.

Maybe, other forum members can add some insights.

| Subscribe To Our Free Newsletter |