Q1 FY25 Concall Highlights

-

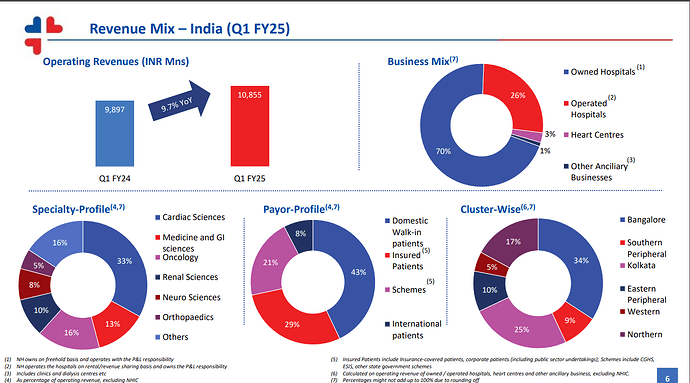

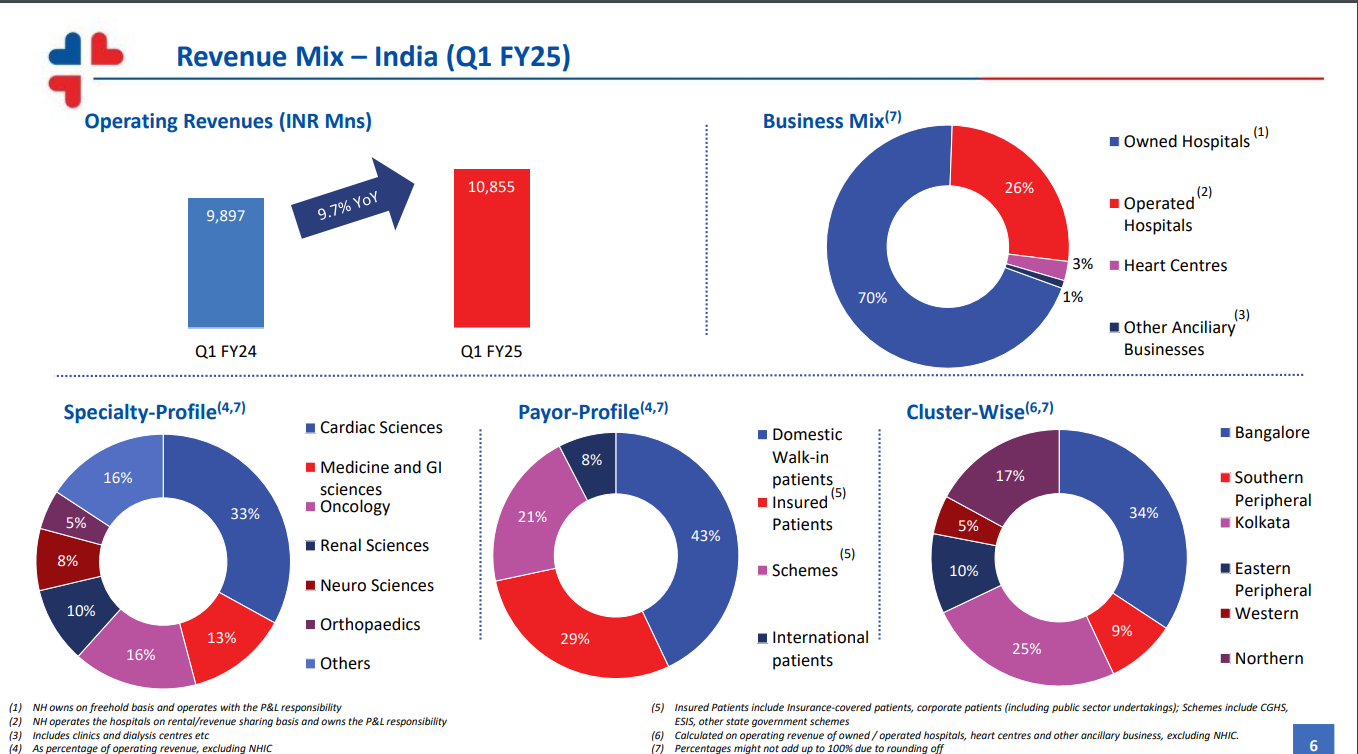

Consolidated operating revenues of INR 13,410 mn in Q1 FY25, an increase of 8.7% YoY and 4.8% QoQ.

-

Consolidated EBITDA of INR 3,274 mn in Q1 FY25 at margin of 24.4%, and consolidated PAT of INR 2,015 mn for Q1 FY25 at a margin of 15.0%.

-

Consolidated Total Borrowings less Cash & Bank Balance and Investments of INR 1,549 mn as on 30th June 2024**, i.e. net debt to equity ratio of 0.05** (Out of which, debt worth US$ 75.0 mn is foreign currency denominated).

-

-

-

-

Revenue from NHIC and NHIL stood at INR 80 mn and EBITDA stood at -INR 120.8 mn for Q1 FY25.

-

Kolkata Greenfield capex- The estimated capex would be INR 1000 cr and in the first phase, 350 beds will be built

-

Bangalore greenfield capex- Estimated capex to be INR 500 cr, bed capacity yet to be finalized

-

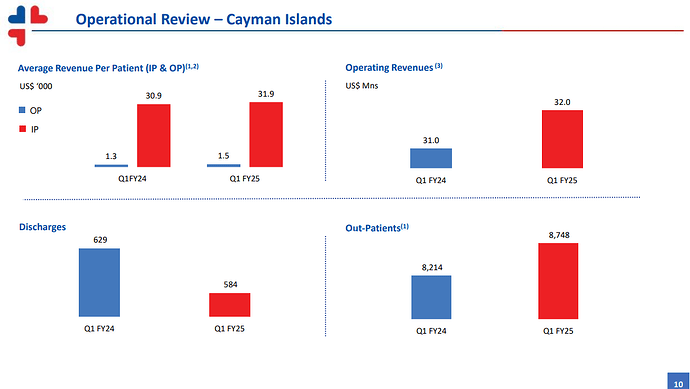

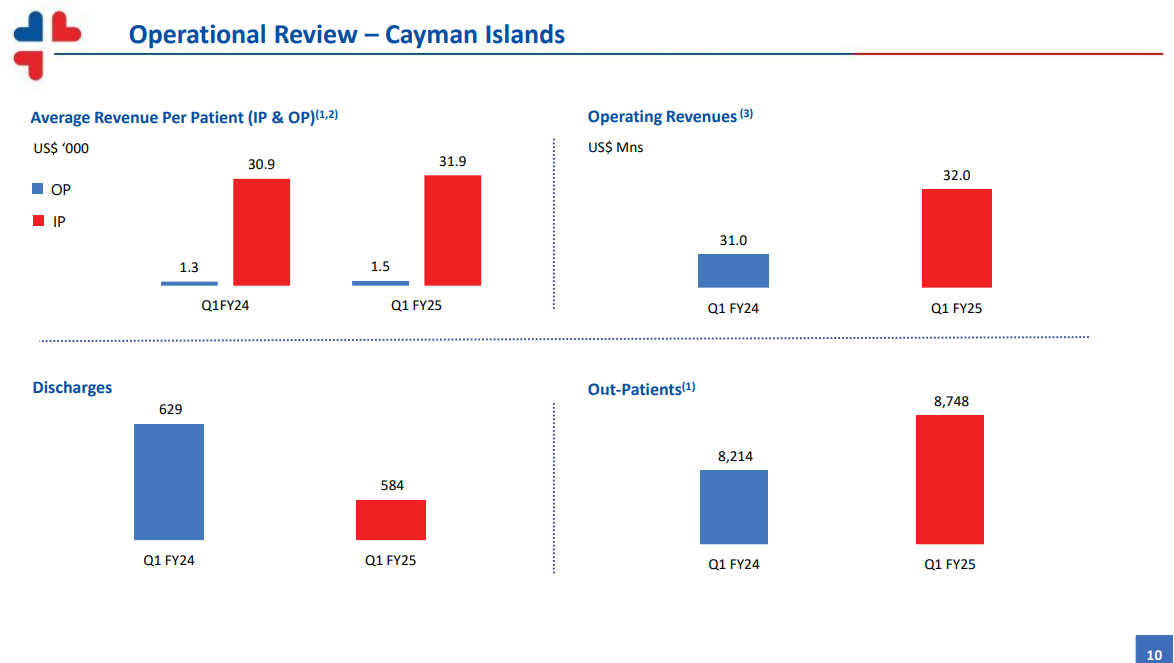

Cayman facility- NH will see margin dilution for some time due to the upcoming Cayman facility capex due to high fixed costs. The new facility will fill the gaps on NH’s existing offerings in Cayman. The existing Cayman facility is also seeing a saturation point, so the management feels it as a good time to go for a new facility

-

The insurance facility is currently limited to Narayana hospitals across India. In future, the management sees that the insurance facility will not be provided all the major hospitals like we see in normal insurances today and will operate in a narrow network.

-

Debtor days- Comparing YoY, we are at similar levels. But comparing QoQ, we have deteriorated by about 8-10 days as in Q4 most of the collections happen. The management expects the debtor days to improve in the next quarter.

-

Company is focusing more on domestic patients and less on international patients. Management is OK if the international patient’s revenue goes down to 0% in next 5 years. As per the mgmt., they never differentiated on the prices for international patients and domestic patients (Superb management quality according to me, I know investors might not like it)

-

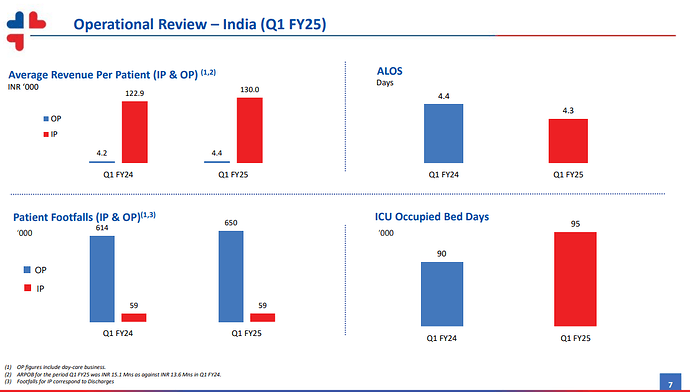

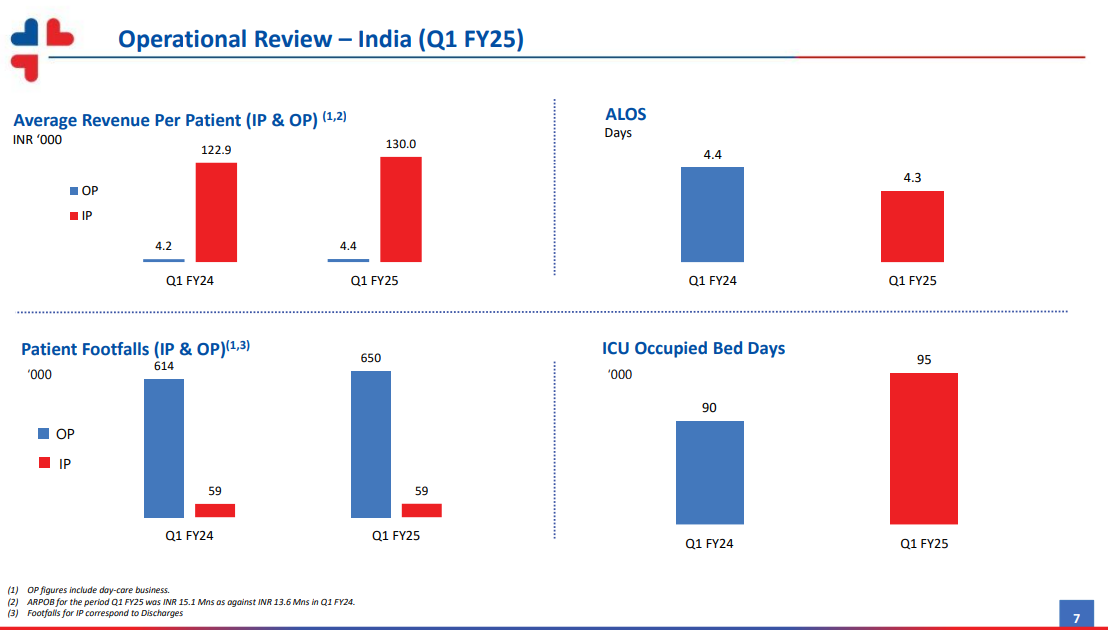

Occupancy levels in Q1 was around 60%

| Subscribe To Our Free Newsletter |