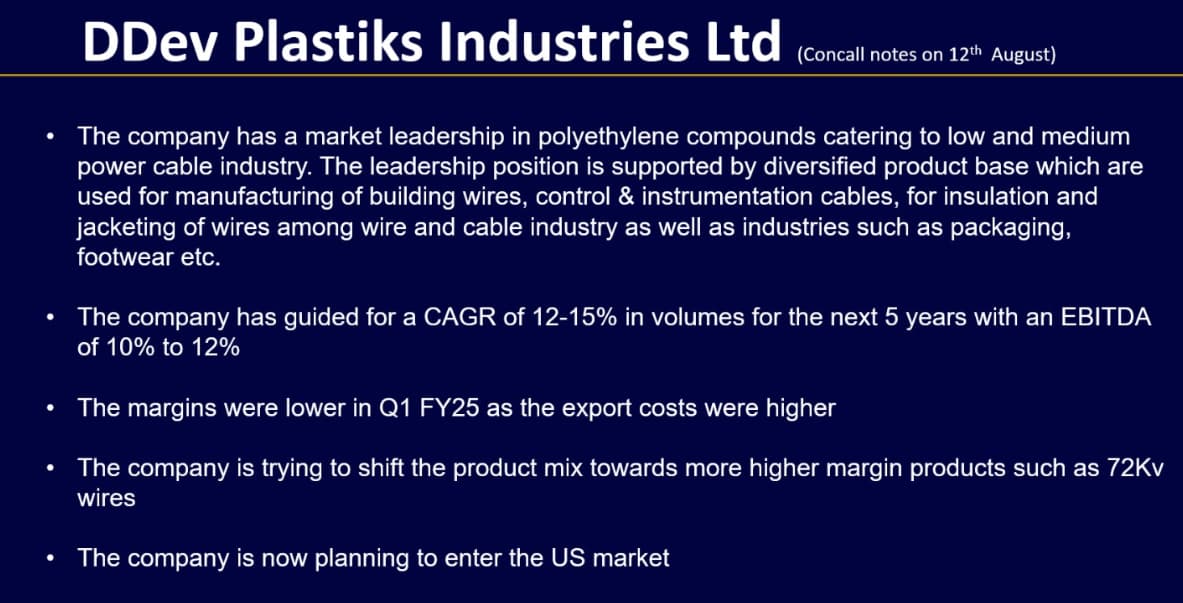

Ddev Plastiks Industries Limited (DPIL) – Q1 FY25 Earnings Call Key Takeaways

Financial Performance (Q1 FY25)

- Revenue: INR 625 crore, a 6% YoY increase.

- EBITDA: INR 65 crore (including other income), 10% margin.

- PAT: INR 42 crore, 11% YoY growth.

Operational Performance

- Volume Growth: Achieved 46,585 MT in sales volume, 18.5% YoY growth.

- Capacity Utilization: Currently at 80%, with an installed capacity of 233,400 MTPA as of June 2024. Targeting 95% utilization by FY26.

- Product Mix Shift: Shifting capacity from lower-margin products to higher-margin offerings.

- Exports: Accounted for 24% of Q1 FY25 revenue.

- Key Clients: Apar, Havells, KEC, KEI, Paramount, and Polycab contribute to ~22% of total revenue.

Future Outlook

- Revenue Target: INR 5,000 crore by FY2030.

- Growth Drivers: Strong demand in wire and cable industry, transition to HFFR cables, and US market expansion.

- Capex Plans: INR 300 crore investment over next three years.

- Volume Growth Guidance: Expects 180,000 to 185,000 MT in volume for FY25.

- EBITDA Margin Guidance: Expects 15-15.5% EBITDA margin for FY25.

Concerns

- Pressure on Margins: Increased shipping costs and decline in raw material prices.

- Competition: Faces competition from international players.

- Backward Integration: Key customers backward integrating by manufacturing their own plastic compounds.

Other Points

- DPIL became net debt-free in Q4 FY24.

- Actively engaging with potential investors but no concrete developments regarding a stake sale disclosed.

- Machine generated highlights, exercise diligence.

| Subscribe To Our Free Newsletter |