Q1FY25 quarter conf call was very interesting for me.

A few key takeaways from the conf call, from my perspective:

-

Infusion of 900 crores by IW Energy Ltd. = parent company. Makes company net cash +ve.

-

(Tender) Tariffs have been healthy and quantitative ranging between:

a. INR 3.4 to INR3.5 per unit for central sector wind solar hybrid project,

b. INR 3.6 to INR3.68 for plain vanilla wind

c. around INR 5 per unit for FDRE -

Lease on a rental basis for Nacelle hub manufacturing in Ahmedabad. Cost = 4 crores per annum. Substantial savings on Capex. No capex and only minimal rental payments.

-

Current year execution target is 800 MW for current year and next year is 1200 MW (might revise upwards too).

-

- No changes for FY25 guidance wise.

-

- FY26 might see margin improvements due to cost optimization, operating leverage, a better product mix & no finance cost.

a. From Q2 onwards, if you see, so we will have interest earnings (on the cash balance which we have in our balance sheet today) also, which will negate the interest expenses. So, we’ll have a negligible interest outgo from Q2 onwards.

b. Tax loss carry forward: So, FY’25 and ’26, we’ll be actually paying no taxes on our profits.

- FY26 might see margin improvements due to cost optimization, operating leverage, a better product mix & no finance cost.

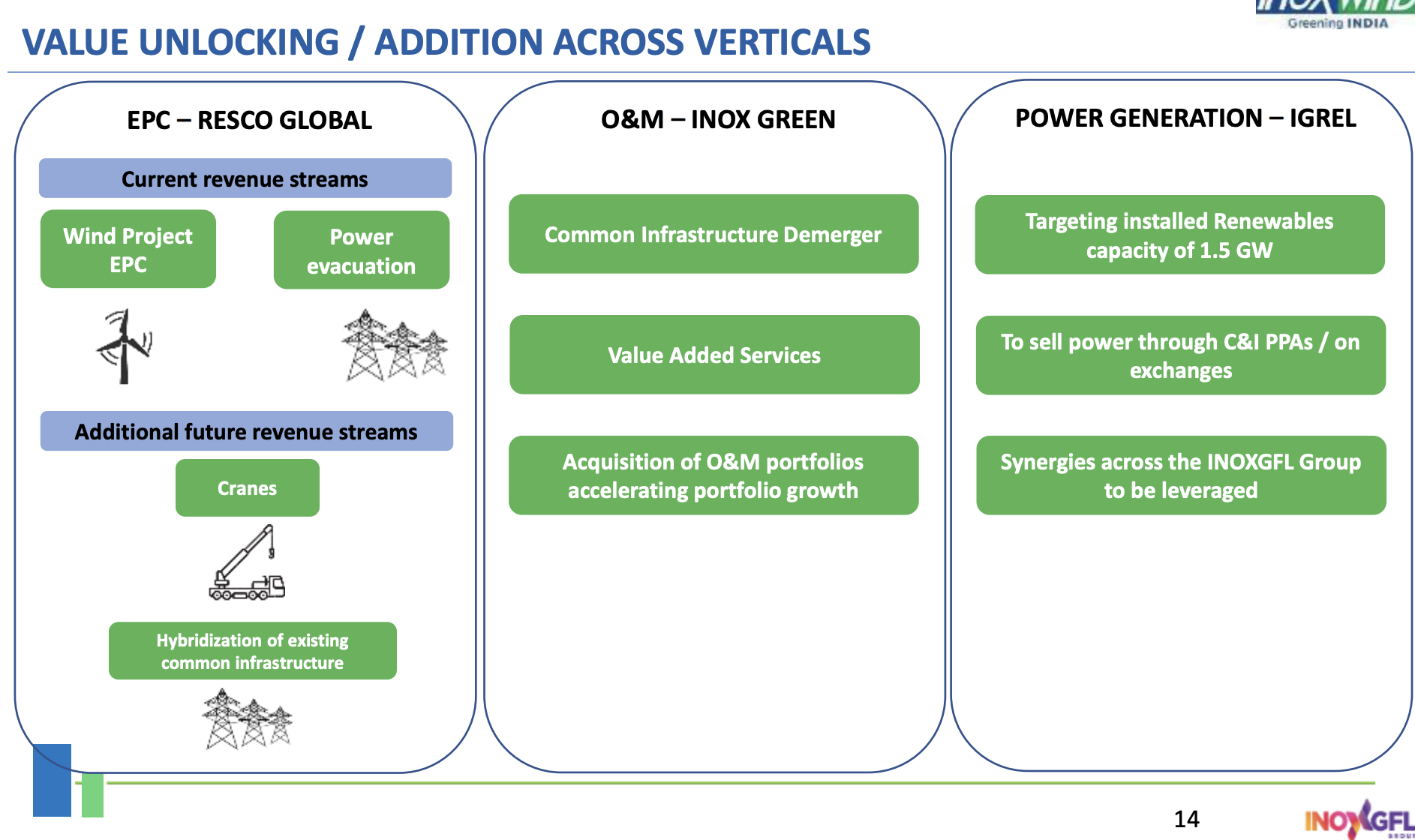

Demerger/ Spinoff:

We are evaluating value unlocking through our EPC arm and also value enhancement through our hybridization of the existing common infrastructure.

Per mgmt, given the multi decadal opportunity ahead:

- at RESCO, it plans to hybridize the common infrastructure like Wind Project EPC, the power evacuation like the substations.

- “backward integrating” – we are getting our own cranes. The returns are phenomenal (30%+)

- (what)we are now doing is given the massive multi-decade opportunity we have ahead of us. We are if I may say so backward integrating into capturing more value within the EPC arm. So we are getting our own cranes. The returns are phenomenal. The payback periods are phenomenal. We are evaluating various other assets to be added within the EPC arm where returns are phenomenal. For example, we buy transformers, our transformers and cable procurement is almost INR400 crores to INR500 crores in a year, given the run rate which we would be on in the coming financial year. We are evaluating whether it makes sense to buy out some of these things to get into it, to manufacture that in-house. Cranes, as I mentioned, is one key area we are anyways moving into internally

- I think we sit on over 5 gigawatts of project site inventory and land bank, which frankly is not given any due importance of value in reality terms, and that’s worth a few couple of INR1000 crores, honestly. So by shunting out the power evacuation from INOX Green, not only do we make the INOX Green balance sheet very light and eliminate the depreciation line, which impacts profitability. But by merging that into the Resco, which is our EPC arm, it leads to automatic listing and creating tremendous incremental value for the larger Inox Wind group. Of course, it’s subject to board approval, but that’s what we are thinking of.

- The company is planning to provide crane services to their existing EPC clients and also rent them to 3rd parties.

| Subscribe To Our Free Newsletter |